Key Takeaways

Winning in stocks is a decision, not a gift you're born with

Minervini opens by demolishing the myth that great traders are naturally gifted. He started poor, undereducated, and lost money for six years before turning a few thousand dollars into millions. He cites the famous Berlin violin study: by age twenty, elite players had logged over 10,000 hours of practice versus 4,000 for the mediocre, and crucially, no 'naturals' floated to the top with fewer hours. Peter Lynch quipped there was no ticker tape above his cradle.

Minervini frames every trader as housing two selves: the builder (disciplined, process-driven, treats mistakes as lessons) and the wrecking ball (ego-driven, fixated on results, blames others). Drawing on a Native American parable, he argues the wolf that wins is the one you feed. Choosing to win and committing fully is lesson zero.

The 'winning is a choice' framing borders on motivational cliche, but the deeper claim about deliberate practice is empirically robust. Anders Ericsson's research (the actual source of the violin study) emphasizes that not all practice counts, only focused, feedback-driven repetition improves performance, which aligns with Minervini's insistence on tracking results. A useful caution: survivorship bias lurks here. For every Minervini who persisted six years and broke through, others persisted equally and failed. The builder versus wrecking ball dichotomy echoes Carol Dweck's growth versus fixed mindset, repackaged for traders. The honest takeaway is that talent is neither sufficient nor the bottleneck; structured persistence is the lever within your control.

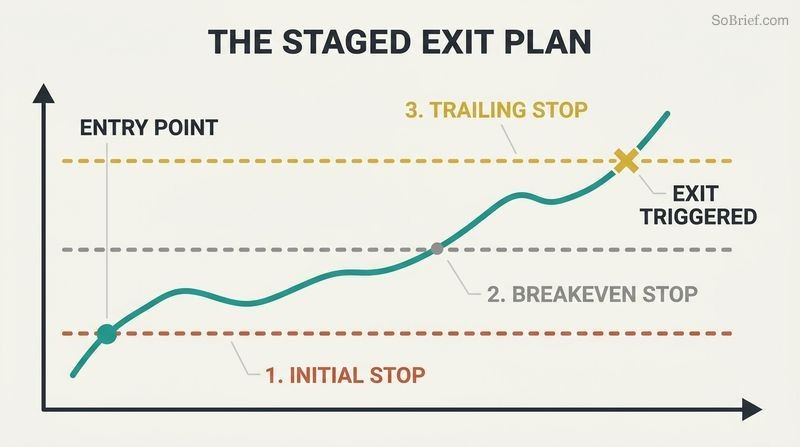

Never enter a trade without first deciding where you'll exit

Minervini's first rule: always go in with a plan. Most people commit $100,000 to a stock on a tip with less research than they'd give an $800 TV. A plan defines the what, why, when, and how: your entry trigger, your risk response, your profit-taking method, and your position sizing.

Central to this is contingency planning, a 'what if' playbook updated as new scenarios arise. After 9/11, Merrill Lynch moved its data center to a separate power grid; Minervini keeps a second brokerage account to short against longs if his primary firm goes down. His priorities shift in sequence: first limit the loss with an initial stop, then protect breakeven once the stock advances, then protect accumulated profit with a trailing or back stop. Hope, as Ed Seykota warned, is not a strategy.

The power of pre-commitment is well documented in behavioral economics. Deciding your exit before entering is a form of what Ulysses did binding himself to the mast: you make the rational choice while calm, before fear and greed hijack judgment. This counters the 'hot-cold empathy gap' identified by George Loewenstein, where people in a calm state underestimate how differently they'll behave under emotional arousal. Minervini's contingency playbook resembles aviation checklists, which Atul Gawande showed dramatically reduce errors in high-stakes, time-pressured environments. The train-schedule analogy (knowing when to worry the train is late) is a clever heuristic for distinguishing normal volatility from genuine breakdown.

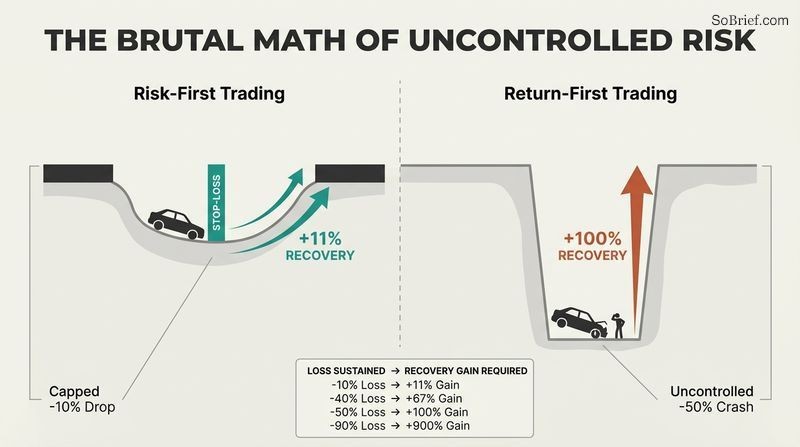

Trade risk-first because losses compound geometrically against you

Every morning Minervini reminds himself he can do serious damage to his account. His core discipline is approaching every trade risk-first, focused on what he can lose rather than what he might gain. Trading without a stop-loss, he says, is like driving without brakes: you'll crash eventually.

The math is brutal because losses work geometrically. A 10% loss requires an 11% gain to recover. A 40% loss needs 67%. A 50% loss demands 100%. A 90% loss requires a 900% gain. This is why he caps losses at 10% maximum, averaging far less. He warns against the 'involuntary investor,' Jesse Livermore's term for someone who becomes a long-term holder only because their trade went wrong. He also avoids volatile 'bucking bronco' stocks whose wild swings make tight stops impossible, recalling a childhood horse named Black Orchid that bucked him off repeatedly.

The asymmetry of percentage losses is mathematically undeniable and underappreciated by retail investors who anchor on the nominal dollar amount rather than the recovery hurdle. This is the same logic behind why drawdown control dominates compound returns over time, a point Nassim Taleb makes about 'ruin' being an absorbing barrier: once you're wiped out, expected value calculations no longer apply because you can't play again. Minervini's emotional stop-loss insight is sharp: everyone has a pain threshold, but for most it sits far past where math dictates, doing both financial and psychological damage. The Black Orchid story memorably encodes a real edge: avoiding high-volatility names where stops get whipsawed.

Set your stop using your real batting average, not wishful thinking

Risk is not arbitrary; losses must be a function of expected gain. To size a stop, you need three numbers: your average gain, your average loss, and your batting average (percentage of winning trades). At a 50% win rate, keeping losses at half your gains yields a 2:1 reward/risk ratio.

Minervini's counterintuitive secret: he'd rather profit at a 25% batting average than 75%, because small losses build 'failure' into the system and let him be wrong often while still winning. He rejects the popular advice to widen stops for volatile stocks. His proof: at a 40% batting average, taking 4% gains and 2% losses nets a profit, while taking 42% gains and 21% losses (same 2:1 ratio) actually loses money, because large losses compound destructively. He uses Result-Based Assumptions (actual past results) over Theoretical Base Assumptions (hopeful projections).

This is the book's most quantitatively rigorous insight and its most contrarian. The finding that identical reward/risk ratios produce wildly different outcomes depending on absolute magnitude flows directly from the multiplicative nature of compounding, the same reason volatility drag erodes leveraged ETFs. Minervini is essentially deriving a discretionary cousin of the Kelly criterion, which he references via 'Optimal F.' The expectancy formula he calls his 'holy grail' is standard in systematic trading, but his emphasis on using real, logged results rather than fantasized targets is where most retail traders fail. The behavioral trap is that traders set stops based on what they hope the stock does, not what their track record proves they actually capture.

What gets measured gets managed: log every trade like an actuary

Minervini learned the power of measurement from slot car racing, where he logged lap times in a notebook after every adjustment to tires, motors, and bodies. He brings the same obsession to trading. At his workshops, almost no one can name their average gain, average loss, and win rate. Flying without those numbers, he says, is like flying without an instrument panel.

He tracks everything on a spreadsheet: average win, average loss, win/loss ratio, batting average, largest wins and losses, and how long he holds winners versus losers (his 'Stubborn Trader' indicators). If you hold losers longer than winners, you're doing the exact opposite of what works. He compares this to how insurance companies set premiums using actuarial life-expectancy tables. Your distribution of trades forms a bell curve; the goal is to skew it right, with a hard wall at minus 10%.

The actuarial framing is genuinely illuminating: insurers don't predict individual deaths, they manage distributions, and traders should think the same way about individual trades. This reframes trading from prediction to probability management, which is psychologically liberating because it removes the need to be right on any single bet. The resistance most people feel toward reviewing losing trades is a documented phenomenon called the 'ostrich effect,' where investors avoid monitoring portfolios during downturns. Minervini's prescription, deliberately confronting painful data, parallels exposure therapy in clinical psychology. One nuance: with small sample sizes, early statistics are noisy, so a beginner's first twenty trades may mislead more than guide.

Averaging down on losers is the fastest road to ruin

Minervini's chapter title says it: compound money, not mistakes. His deadliest rookie error was averaging down, buying more of a falling stock to lower his cost basis, throwing good money after bad. He cites Paul Tudor Jones's trading-desk sign: 'Losers average losers.'

He warns of the '50/80 rule': once a major market leader tops, there's a high chance it falls 50%, and a coin-flip chance it ultimately drops 80% or more, with average declines exceeding 70%. Lumber Liquidators and Cisco both fell roughly 90% from their peaks. He also debunks the 'cheap trap': a stock that's down isn't a bargain like a discounted Armani jacket, because stocks discount the future and falling prices often signal problems institutions already see. When a great earnings report sends a stock down hard, that's 'differential disclosure': the big players know something you don't. Trust your eyes, not your ears.

The 'just this one time' analysis is the book's sharpest psychological observation: occasional reinforcement of rule-breaking is more corrosive than consistent punishment, a principle straight from B.F. Skinner's work on variable-ratio reinforcement schedules, the same mechanism that makes slot machines and gambling so addictive. Getting rewarded for averaging down once virtually guarantees you'll do it again until catastrophe. The 'cheap trap' critique cuts against deep-value investing, and here Minervini is partly trading-style-specific: value investors like Graham built fortunes buying declining prices. The reconciliation is time horizon and the difference between price confirmation and pure contrarianism. For momentum traders using tight stops, fighting the trend is suicidal.

Only buy stocks in confirmed Stage 2 uptrends; trade with the wind

Minervini buys only stocks in long-term uptrends, what he calls catching a wave with the tide in your favor. Stocks cycle through four stages: Stage 1 (neglect/consolidation), Stage 2 (advancing/accumulation), Stage 3 (topping/distribution), and Stage 4 (declining/capitulation). Over 95% of the biggest winners since the late 1800s made their gains in Stage 2. In any other stage you're either losing money or losing time.

His Trend Template lists eight non-negotiable criteria, anchored by the price trading above its rising 200-day and 150-day moving averages, with the 50-day above both. Paul Tudor Jones's one rule: get out of anything below its 200-day. Minervini illustrates with Valeant, which fell 92% after closing below its 200-day line while Bill Ackman doubled down. Avoiding 'serial gappers' (downtrending stocks that gap lower) and demanding new highs (Monster Beverage rose 8,000% making new highs all the way) round out the discipline.

Trend-following has strong academic backing: the momentum factor documented by Jegadeesh and Titman, and later Cliff Asness at AQR, shows that past winners tend to keep winning over intermediate horizons, one of the most robust anomalies in finance. Minervini's Stage Analysis is essentially Stan Weinstein's framework from the 1980s, repackaged with disciplined criteria. The insistence on new highs directly contradicts the 'buy low' instinct most retail investors hold, and the Monster Beverage example is the steelman: a stock can only become a multibagger by making a continuous series of new highs. The Ackman/Valeant case is a vivid reminder that intelligence and conviction are no defense against ignoring the tape.

Buy when volatility contracts to a coiled spring near the pivot

Once a stock is in Stage 2, Minervini looks for his signature setup: the Volatility Contraction Pattern (VCP). As a stock consolidates, it forms a sequence of two to six progressively smaller pullbacks, each roughly half the prior one, accompanied by drying-up volume. Bitauto corrected 28%, then 16%, then just 6% before rocketing 465%.

He likens it to wringing a wet towel: each twist releases less water until the towel is light and moves easily. The contractions represent weak holders being replaced by strong ones, absorbing overhead supply until the 'line of least resistance' forms. When volume nearly vanishes at the tightest point, even small demand sends the price flying. The exact entry is the pivot point, a call-to-action price where the stock breaks out on expanding volume. Minervini encodes each base as a 'footprint' (time, price depth, number of contractions) like a person's height and weight measurements.

The VCP is the book's signature contribution and a refinement of William O'Neil's cup-with-handle pattern. The underlying logic is sound microstructure: declining volume during a base signals that sellers are exhausted and float has tightened, so the supply/demand imbalance can resolve violently upward. Skeptics note that chart-pattern trading sits uneasily with the efficient-market hypothesis, and rigorous backtests of visual patterns are notoriously hard because pattern recognition is subjective. Minervini partly addresses this by quantifying the footprint. The honest framing: the VCP is a probabilistic filter that, combined with strict stops, can produce positive expectancy even when many individual setups fail. It's a risk-management edge as much as a prediction tool.

Concentrate in four to six best names; diversification dilutes your edge

Minervini flatly rejects broad diversification for traders seeking superperformance, calling over-diversification 'di-worsification.' If you have a real edge, spreading capital thin just produces an average return, in which case you'd be better off buying an index fund. To beat the market you must concentrate in the best four to twelve names, ideally putting most capital in your top four or five.

The discipline that makes concentration safe is position sizing tied to risk. Never risk more than 1.25% to 2.5% of total equity on any trade, never take a position larger than 50%, and cap stops at 10%. With a 25% position and a 10% stop, you risk only 2.5% of equity. He points to Ken Heebner managing billions in under 20 names. The 'two-for-one rule' lets you reallocate: trim two weak performers by half to fund one promising new full position. Tend your portfolio like a garden, pulling weeds and watering flowers.

This directly opposes Modern Portfolio Theory and Harry Markowitz's diversification-as-free-lunch, but the contradiction is partly definitional. Minervini is making a Kelly-criterion argument: if you have a genuine edge, concentration maximizes geometric growth, whereas diversification is optimal precisely when you lack edge or can't identify it. The catch, of course, is the enormous 'if you have an edge,' which most investors overestimate (the Dunning-Kruger problem). His position-sizing math is the genuine safeguard: by capping equity-at-risk per trade, concentration in count does not mean concentration in risk. Buffett famously echoed this: diversification is protection against ignorance and makes little sense for those who know what they're doing.

Sell into strength while buyers are eager, not into the crash

Minervini found that after mastering buying, his hardest lesson was selling a winner. Two emotions, fear and regret, paralyze traders: sell too soon and you miss gains; sell too late and you give them back. The professional move is selling into strength, while the stock is rising and buyers are plentiful, rather than waiting for weakness.

He reads the stock's life cycle through base counting (bases 5 or 6 are failure-prone, late-stage tops) and P/E expansion (if the multiple doubles from when the move began, beware). The climax top is the key sell signal: a stock accelerates 25% to 50% or more in one to three weeks, with 70%+ up days, exhaustion gaps, and the largest single up-day of the entire run. Qualcomm soared 260% in two months, then fell 88%. To neutralize regret, the 'sell-half rule' lets you bank profit on half and ride the rest, a psychological win either way.

Selling is genuinely the under-taught half of trading, and Minervini's emotional framing maps onto prospect theory: Kahneman and Tversky showed losses loom about twice as large as equivalent gains, which explains both the urge to dump winners early (locking in certain gain) and to hold losers (avoiding certain loss). The sell-half rule is an elegant behavioral hack that hedges against both regret directions, similar to dollar-cost-averaging out of a position. The climax-top signals are pattern-based and somewhat subjective, but the underlying institutional logic, that big funds must distribute shares into retail euphoria on the way up because they can't exit all at once, is structurally true and explains why tops form amid the most exciting price action.

Master your fear by rehearsing losses, not just visualizing wins

In a closing dialogue with performance coach Jairek Robbins, Minervini tackles the psychology. The antidote to fear is detachment from outcome plus daily preparation. Robbins distinguishes mental rehearsal from positive visualization: visualizing only wins is dangerous, because when a loss hits, your nervous system panics. Instead, like Muhammad Ali rehearsing taking punches, you rehearse following your plan when trades go against you, seeing yourself accept a small loss calmly.

Practical tools include 'box breathing' (inhale, hold, exhale, hold, four seconds each) to oxygenate the brain and quiet anxiety, plus physical activation. Robbins applies habit science (cue, routine, reward) and urges traders to literally celebrate taking a small loss, retraining the pain/pleasure cycle so cutting losses feels like victory. A Duke study found 40% of daily behavior is habit, not conscious choice. Confidence scales from getting it right with small positions first.

The mental-rehearsal-over-visualization distinction is backed by research: Lien Pham and Shelley Taylor found that students who visualized the process of studying outperformed those who visualized the outcome of a good grade, who actually did worse. Outcome fantasy can sap motivation and leave you brittle. The 'celebrate a small loss' prescription is operant conditioning applied to oneself, attempting to reverse the natural aversive response, though whether you can genuinely fool your limbic system into enjoying losses is debatable. Box breathing is validated stress physiology, activating the parasympathetic nervous system. The deeper point, that trading uniquely punishes mistakes financially and thus compounds fear, is astute and explains why trading psychology is harder than other skill domains.

Compound modest gains; you don't need a moonshot to triple your money

Minervini's 'Plan B,' which transformed his results from mediocre to stellar, is recognizing that you don't need to find one giant winner. Through 'velocity trades,' gains of 20% to 50% over weeks, and the power of compounding, small consistent wins outperform rare big ones. He shows the math: twelve 10% gains compound to a 214% return, beating two 40% gains (96%). It's far easier to find a dozen 10% winners than one stock that triples.

This ties together his eight keys to superperformance: precise timing, concentration, embracing turnover (cheap commissions make it viable today), maintaining risk/reward, selling into strength, trading small before big, trading directionally with the trend, and protecting breakeven. He dramatizes opportunity cost: holding a stock through a long correction ties up capital you could deploy elsewhere. Higher turnover of a real edge, turned over more often, beats waiting for the rare home run.

The compounding arithmetic is incontestable and underappreciated, the same logic Einstein allegedly called the eighth wonder of the world. Framing trading as repeatedly exercising a small statistical edge, like a casino's house advantage turned over thousands of times, is the correct mental model and connects to the law of large numbers: the more times you deploy positive expectancy, the more reliably results converge to the expected value. The honest caveat is taxes and transaction friction, which Minervini acknowledges have shrunk but which still matter for taxable accounts where short-term gains are taxed as ordinary income. The opportunity-cost emphasis is genuinely valuable: most retail investors fixate on realized losses while ignoring the invisible cost of dead money.

Analysis

Think and Trade Like a Champion is the second volume of Mark Minervini's trading philosophy, and unlike most market books it is overwhelmingly about risk and psychology rather than stock selection. Roughly two-thirds of the content concerns how to lose correctly, manage position size, track results, and master emotion. This is its great strength and its marketing weakness: readers come for the secret of picking winners and get a disciplined risk-management catechism instead.

The book sits at the confluence of three traditions. Technically, Minervini extends William O'Neil's CAN SLIM and Stan Weinstein's stage analysis, refining the cup-with-handle into his quantified Volatility Contraction Pattern. Statistically, he is doing applied Kelly-criterion position sizing and expectancy management, dressed in baseball and poker metaphors. Psychologically, he channels Tony Robbins-style peak-performance coaching, culminating in the literal coaching dialogue that closes the book.

The most intellectually durable material is the math of asymmetric losses and expectancy. His demonstration that identical reward/risk ratios yield opposite outcomes depending on absolute loss magnitude is a genuine insight most traders never internalize, flowing from the multiplicative nature of compounding. The weakest material, epistemically, is the chart-pattern recognition, which resists rigorous backtesting because it depends on subjective judgment, and the survivorship-tinged 'winning is a choice' rhetoric.

The central tension the book never fully resolves: nearly all its edge depends on 'if you have an edge,' yet it offers no objective test for whether your edge is real versus luck, beyond tracking results. A trader with negative expectancy who concentrates and turns over rapidly will be destroyed faster, not enriched. Minervini's safeguards (small initial positions, strict stops, scaling on success) partly address this. For a disciplined reader who treats it as a risk-first operating system rather than a stock-picking shortcut, the book delivers a coherent, internally consistent, and unusually honest framework. Its enduring lesson is that survival, not prediction, is the master skill.

Review Summary

Readers consistently praise Minervini's clear writing style and actionable advice. Many consider it a must-read for traders, offering practical tips on mindset, routine, and risk management. Some note overlap with his first book but still find unique value. The book is lauded for its focus on the psychological aspects of trading and its scientific approach to performance improvement.

People Also Read

FAQ

What's "Think & Trade Like a Champion" about?

- Comprehensive Trading Guide: "Think & Trade Like a Champion" by Mark Minervini is a comprehensive guide to mastering stock trading with a focus on developing a champion mindset.

- Key Learning Areas: The book covers essential trading skills such as reading charts like a professional, precise buying techniques, optimal position management, and risk reduction.

- Proven Strategies: It introduces time-tested rules and strategies that have helped Minervini become one of America's most successful stock traders.

- Emotional Control: The book also emphasizes the importance of controlling emotions and making a successful trading plan.

Why should I read "Think & Trade Like a Champion"?

- Expert Insights: Gain insights from Mark Minervini, a renowned stock trader with a proven track record of success.

- Practical Techniques: Learn practical techniques for maximizing profits and minimizing risks in stock trading.

- Mindset Development: Understand the psychological aspects of trading and how to develop a winning mindset.

- Comprehensive Coverage: The book covers a wide range of topics, making it suitable for both beginners and experienced traders.

What are the key takeaways of "Think & Trade Like a Champion"?

- Risk Management: Prioritize risk management to protect your capital and ensure long-term success.

- Strategic Planning: Develop a clear and actionable trading plan to guide your decisions.

- Emotional Discipline: Control emotions to avoid costly mistakes and maintain focus on your trading strategy.

- Continuous Learning: Embrace a mindset of continuous improvement and learning from both successes and failures.

What is the SEPA method in "Think & Trade Like a Champion"?

- SEPA Definition: SEPA stands for Specific Entry Point Analysis, a method developed by Minervini to identify optimal entry points for stock trades.

- Focus on Leadership: It involves identifying stocks with leadership potential based on historical data and specific characteristics.

- Risk and Reward Balance: The method emphasizes balancing risk and reward by setting precise entry and exit points.

- Proven Success: SEPA has been instrumental in Minervini's success, helping him achieve significant returns over the years.

How does Mark Minervini suggest managing risk in trading?

- Risk First Approach: Minervini advocates for a "risk first" approach, focusing on potential losses before considering potential gains.

- Stop-Loss Orders: Use stop-loss orders to limit losses and protect your capital from significant downturns.

- Position Sizing: Carefully determine position sizes to ensure that no single trade can significantly impact your portfolio.

- Emotional Control: Maintain emotional discipline to avoid impulsive decisions that could increase risk.

What are the best quotes from "Think & Trade Like a Champion" and what do they mean?

- "Success is a choice": This quote emphasizes that success in trading is not about luck but about making informed and disciplined choices.

- "Losers average losers": Highlighting the danger of averaging down on losing trades, this quote advises against compounding mistakes.

- "The market is the engine": Reminds traders to respect market trends and not fight against them, as the market ultimately dictates price movements.

- "Effort without knowledge is wasted": Stresses the importance of continuous learning and applying knowledge effectively in trading.

How does Minervini recommend handling emotions in trading?

- Emotional Awareness: Be aware of your emotions and how they can impact trading decisions.

- Pre-Trade Preparation: Prepare mentally before trading to reduce emotional reactions during market fluctuations.

- Stick to the Plan: Rely on a well-thought-out trading plan to guide decisions rather than emotions.

- Learn from Mistakes: Use emotional setbacks as learning opportunities to improve future trading performance.

What is the significance of the "VCP" pattern in Minervini's strategy?

- VCP Definition: VCP stands for Volatility Contraction Pattern, a key concept in Minervini's trading strategy.

- Pattern Characteristics: It involves identifying stocks with decreasing volatility and volume, indicating potential for a breakout.

- Entry Points: The VCP pattern helps traders identify precise entry points for buying stocks.

- Proven Effectiveness: This pattern has been a reliable indicator of stock performance in Minervini's trading experience.

How does Minervini suggest traders should approach stock selection?

- Trend Analysis: Focus on stocks in a confirmed uptrend, avoiding those in a downtrend.

- Leadership Profile: Look for stocks with strong leadership characteristics and potential for significant growth.

- Technical Patterns: Use technical analysis to identify favorable patterns like the VCP for entry points.

- Fundamental Strength: Consider the fundamental strength of a company to support technical signals.

What role does discipline play in Minervini's trading philosophy?

- Core Principle: Discipline is a core principle in Minervini's trading philosophy, essential for consistent success.

- Rule Adherence: Strict adherence to trading rules and plans is crucial to avoid emotional and impulsive decisions.

- Continuous Improvement: Discipline involves continuously refining strategies and learning from both successes and failures.

- Long-Term Success: Maintaining discipline helps traders achieve long-term success and avoid significant setbacks.

How does Minervini address the concept of "timing" in trading?

- Importance of Timing: Timing is crucial in trading, and Minervini emphasizes the need for precise entry and exit points.

- Market Conditions: Understand and adapt to current market conditions to optimize timing decisions.

- Speed of Execution: Be prepared to act quickly when the right timing opportunities arise.

- Avoiding Overtrading: Balance timing with patience to avoid overtrading and unnecessary risks.

What are Minervini's views on diversification in a trading portfolio?

- Concentration Over Diversification: Minervini prefers a concentrated portfolio of high-potential stocks over broad diversification.

- Focused Attention: Concentration allows for focused attention on a few select stocks, increasing the potential for significant returns.

- Risk Management: While concentrated, ensure proper risk management to avoid catastrophic losses.

- Strategic Allocation: Allocate resources strategically to maximize returns from the best-performing stocks.

About the Author

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.