Key Takeaways

Run your options portfolio as a one-man insurance company

“Insurance companies sell 'paper,' a promise to pay in the future in exchange for cash now.”

The core thesis: sell options like insurance. TOMIC — The One Man Insurance Company — is the framework co-author Dennis Chen uses to run his hedge fund, Smart Income Partners. Just as an insurance company collects premiums for bearing risk, an options seller collects premiums from buyers who want protection on their stocks or indexes. The asset insured is the stock; the policy period is the option's expiration; selling out-of-the-money is like offering a deductible.

TOMIC has three primary functions:

1. Trade Selection — the underwriting that determines which risks to take and at what price

2. Risk Management — position sizing, hedging, and trade adjustments

3. Trade Execution — efficiently placing orders on the option exchanges

These are supported by a trading plan, proper infrastructure, and continuous learning processes.

Trade selection is your underwriting — get it wrong and nothing saves you

“AIG sold $450 billion of credit insurance without a clear understanding of how the risks behaved.”

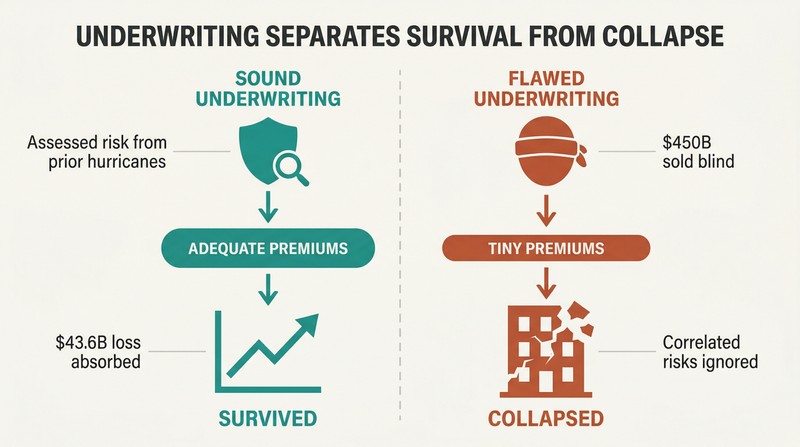

Underwriting separates survival from collapse. Hurricane Katrina caused $43.6 billion in insured losses from 1.75 million claims, yet the insurance industry survived and posted record profits in 2004 – 2006. Their underwriting was sound — they understood hurricane risk from prior events and collected adequate premiums.

AIG was the opposite disaster. The company sold $450 billion in credit default swaps on mortgage-backed securities without understanding how the underlying risks were correlated. Unlike house fires, which don't spread between neighborhoods, mortgage defaults are contagious during recessions. AIG's underwriting was fatally flawed: wrong risk assessment, insufficient premiums, no portfolio-level risk management. Trade selection in your TOMIC must answer five questions covering market, direction, time frame, volatility, and pricing before any premium is sold.

Cap every trade at 2% risk; halt after a 6% monthly loss

“Taking losses from identified risks is acceptable, but getting blindsided from unexpected risks is not.”

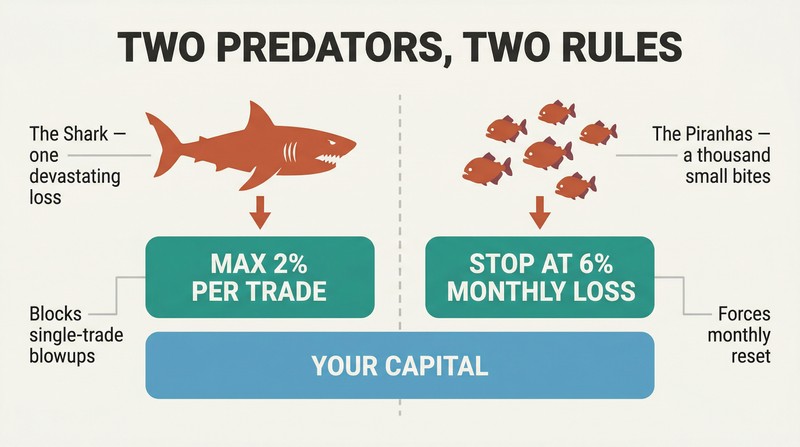

Two predators kill trading accounts. The authors, borrowing from Dr. Alexander Elder, call them sharks and piranhas. The shark is one devastating loss — imagine 35% of your equity wiped out in a single trade. The piranha is a stream of small losses that slowly devour your capital, like piranhas killing a cow with a thousand small bites in the Amazon.

Two rules neutralize both threats:

1. Never risk more than 2% of total capital on any single trade — this prevents shark attacks

2. If the portfolio loses 6% in any single month, stop trading for the rest of that month — this prevents piranha death

With 15 – 20 positions and an 80% win rate, roughly 3 – 4 trades may go against you simultaneously. The 6% circuit breaker forces you to stop, reassess, and return fresh.

Allocate 5-10% to cheap 'units' so a crash pays you instead

“By properly implementing units, you are willing to bet that you will never have to sell your house because the market dropped 25%.”

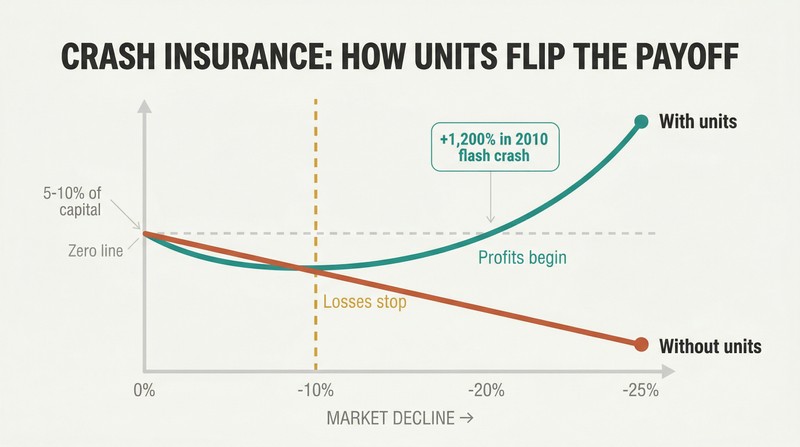

Units are your catastrophic reinsurance. A unit is an inexpensive far out-of-the-money option — typically under $2 in SPX or $0.20 in SPY — with near-zero delta and negligible gamma or vega. In normal markets, they barely move. In a crash, they explode due to a snowball effect: panic buying raises their vega, which raises their delta, which accelerates their price appreciation.

The flash crash proved their power. During the May 2010 flash crash, the fund held OEX May 505 puts purchased at $1.20 each as portfolio insurance. When the market collapsed, those puts closed at $14.50 — a return exceeding 1,200%. The authors recommend spending 5 – 10% of allocated trading capital on units. If the market drops 10%, your portfolio stops losing; at 20%, you're making money.

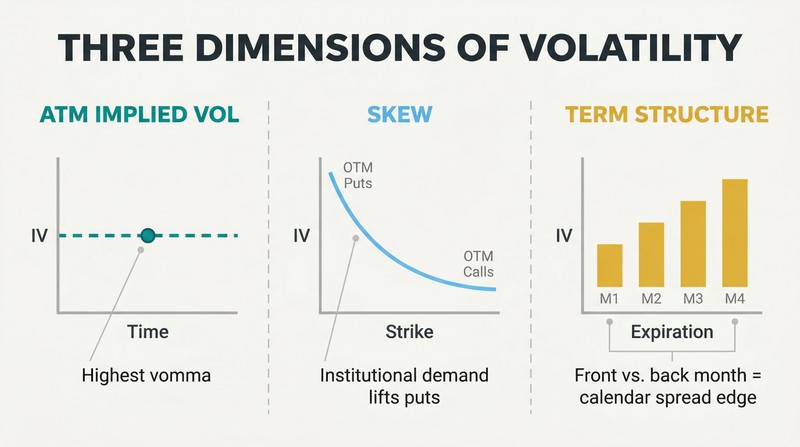

Track volatility in three dimensions: ATM, skew, and term structure

“Any educator, coach, book, software, or service that ignores volatility, or does not emphasize volatility as the primary and fundamental key to success, is likely not worth much.”

Volatility isn't a single number. First, ATM implied volatility — front-month at-the-money options drive the entire surface, possessing what traders call vomma, or the greatest sensitivity to IV changes. Second, skew — how OTM puts trade at higher implied volatility than ATM options (called investment skew ), driven by institutional demand for downside protection from 401(k)s and pension funds buying puts and selling calls. Third, term structure — how different expiration months are priced relative to each other.

Each dimension creates edge. A flat put skew signals a good time to sell iron butterflies. An overbought front month versus back month creates calendar spread opportunities. Implied volatility is determined by supply and demand, not market makers — understanding when each dimension is mispriced is how TOMIC sells expensive policies and buys cheap ones.

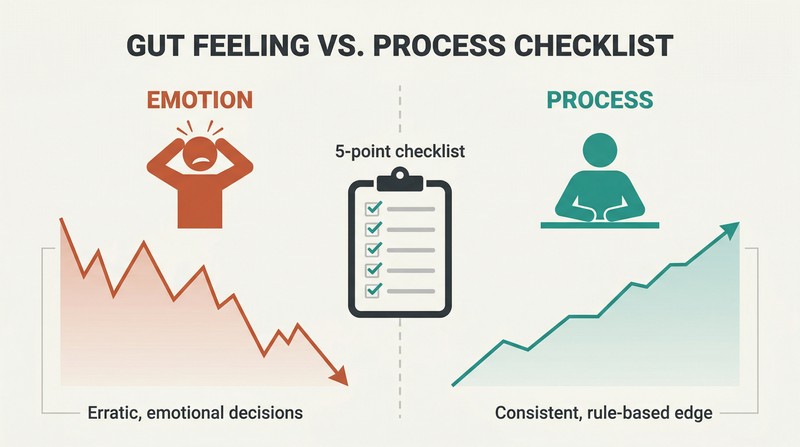

Build a trading checklist — a hospital checklist saved 1,500 lives

“We have seen more dollars lost on gut feeling than just about any other type of loss.”

Checklists enforce discipline when emotions revolt. The authors cite Dr. Peter Pronovost's research at Johns Hopkins: a simple five-item checklist — wash hands, use barrier precautions, clean skin with chlorhexidine, avoid certain insertion sites, remove unnecessary catheters — reduced catheter infections by 66% in Michigan ICUs, saving over 1,500 lives and nearly $200 million. The program cost just $500,000.

TOMIC applies identical logic. Before every trade, demand answers: What's implied volatility relative to historical? What's the skew? Maximum loss? Target profit? Does this conform to position sizing? The blackjack analogy cements the point: hitting on 18 when the dealer shows 6 is bad process, even if you draw a 3 and win. Casinos impose rules on dealers because process — not luck — produces consistent edge. You're the house, not the gambler.

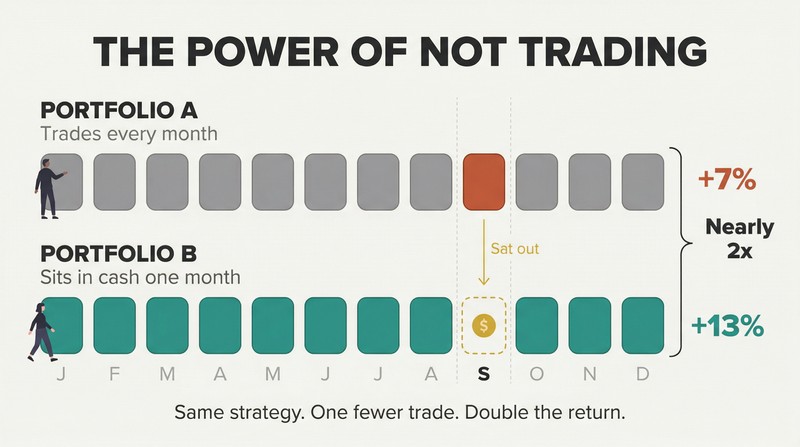

Cash is often the most profitable position you can hold

“It may not be sexy, but in the end I'd rather be rich than sexy.”

Not trading can outperform trading. The authors present two identical iron condor portfolios over twelve months. Portfolio A trades every month and returns 7%. Portfolio B sits in cash during one bad month — September — and returns 13%, nearly double. The only difference: knowing when to fold.

Resist the compulsion to act. If implied volatility is too low to justify selling premium, if skew and term structure don't present clear edge, or if market conditions are uncertain, the right move is no trade at all. The need to constantly hold positions is a psychological compulsion, not a strategic advantage. The authors recommend expanding your knowledge base during downtime — learning new products and strategies — so you can recognize more diverse opportunities rather than forcing mediocre trades into hostile environments.

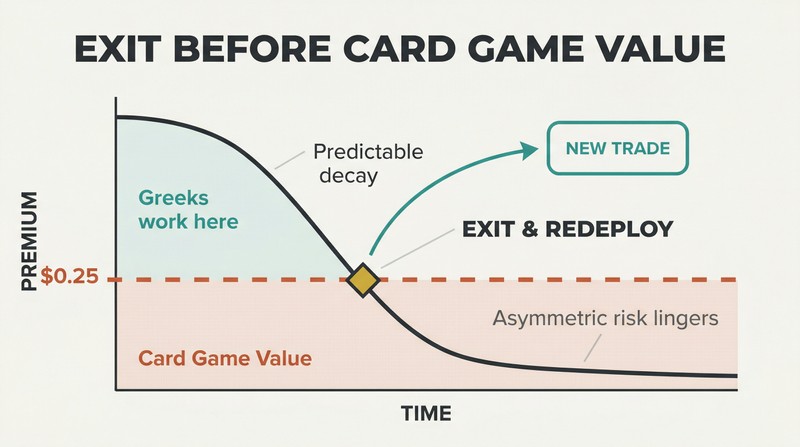

Exit credit spreads once they hold only Card Game Value

“Credit spreads are a great way to make money, but it takes only one bad draw to wipe you out.”

Card Game Value explains why cheap options linger. Imagine two men play a one-time card game: 99 of 100 cards are worthless, one pays $1,000. Mathematically, the draw is worth $10. But since it's played only once, the seller demands far more — there's no series of repetitions to recoup a catastrophic loss.

Options below $0.25 behave identically. Probabilities say they should be worthless, but asymmetric one-time risk keeps them alive longer than any pricing model predicts. The final $0.25 of premium decays agonizingly slowly. For credit spread traders, the actionable lesson: close your spread when the short option enters Card Game Value territory. Free up that margin capital and redeploy it into new trades where standard option pricing and Greeks still work predictably.

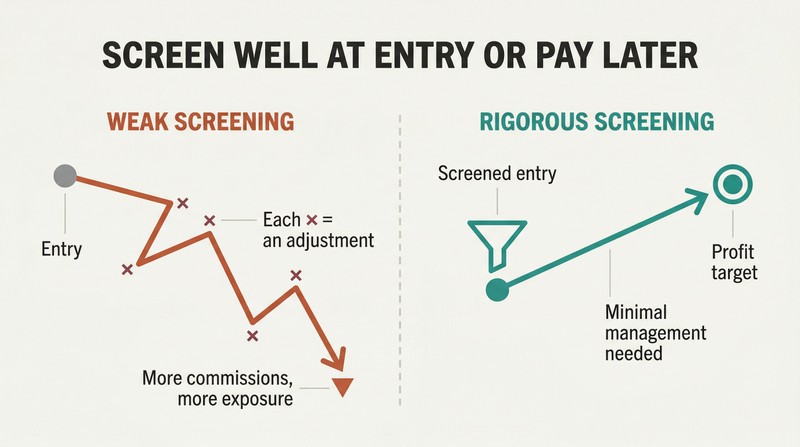

Proper trade screening matters far more than brilliant adjustments

“Well-constructed trades are easy to manage.”

The authors repeat one pattern across every strategy. The iron condor sold when IV was declining and skew was reasonable never triggered risk limits. The iron butterfly entered during flat put skew with steep call skew hit its 10% target in days. The calendar spread sold when term structure was 10% out of line made 5% overnight. In each case, rigorous screening at entry did the heavy lifting.

Over-adjusting is a disease. Each adjustment adds commissions, extends time in the trade, and increases exposure to multi-standard-deviation events — the large moves that actually destroy positions. The authors offer a diagnostic: push your position forward three days. If you'd profit or break even in two of three scenarios (flat, up one standard deviation, or down one standard deviation), do absolutely nothing.

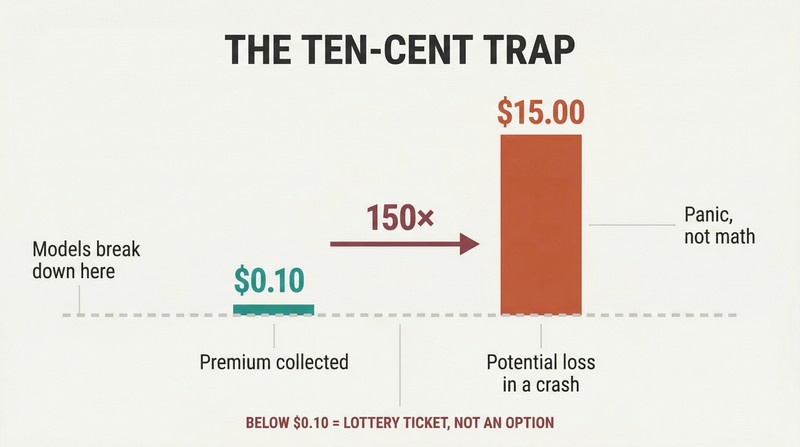

Never short options worth ten cents or less

“A .10 option that moves to 15.00 returns 1,500%, and there is no way to price that degree of movement in an option.”

At a certain price, options stop trading on volatility and become lottery tickets. Around $0.10 in SPX, pricing models break down entirely. The option has near-zero delta and negligible gamma — until a crash. Then panic buying creates a cascading repricing that no mathematical model was designed to capture. The authors call this "human risk."

Three rules protect against catastrophe:

1. Never short options worth $0.10 or less

2. If your short option decays below $0.10, buy it back even with a commission cost

3. A premium-selling fund should always be net long these unit options

Beyond two standard deviations, options respond to panic, not mathematics. Being net long units transforms this unhedgeable tail risk into a profit opportunity — as the flash crash OEX puts demonstrated with their 1,200% return.

Analysis

The TOMIC framework's deepest contribution isn't its option strategies — vertical spreads, iron condors, and butterflies are well-documented elsewhere. Its real innovation is psychological architecture. By recasting the options trader as an insurance underwriter rather than a speculator, Chen and Sebastian solve the identity crisis that destroys most retail traders. When you think of yourself as running an insurance company, every premium collected feels like revenue, every loss feels like a routine claims payout, and catastrophic hedging feels like standard business practice rather than an anxious afterthought.

The insurance analogy is genuinely productive but has structural limits. Insurance companies benefit from the law of large numbers across thousands of uncorrelated policies. A single trader running 15 – 20 positions faces concentration risk that no actuarial table can smooth away — particularly during correlation spikes like 2008, when 'diversified' equity positions moved in lockstep. The authors partially address this with unit-based tail hedging, a concept that anticipates the post-crisis mainstreaming of tail-risk strategies that firms like Universa Investments would later popularize.

The 2%/6% money management rules, adapted from Alexander Elder's trading psychology framework, may be the book's most universally transferable contribution. They mechanically prevent the two failure modes that eliminate traders: the catastrophic single loss and the slow bleed of accumulated small losses. What makes these rules powerful isn't their novelty but their specificity — concrete thresholds remove the judgment that emotion corrupts.

Written in 2012, the book predates zero-day-to-expiration options, algorithmic market-making dominance, and the retail options boom catalyzed by commission-free brokers. Some execution advice — routing to the CBOE, building floor-broker relationships — feels dated. However, the core framework remains structurally sound because it addresses permanent features of options markets: mean-reverting volatility, skew driven by institutional hedging demand, and the ever-present tension between premium collection and tail risk. The book's most counterintuitive insight may be its simplest: professional options traders spend far more time deciding not to trade than they spend trading.

Review Summary

The Option Trader's Hedge Fund receives mixed reviews, with an average rating of 3.85/5. Readers appreciate its valuable insights for intermediate to advanced traders, particularly its comparison of options trading to insurance. However, many find the book inconsistent, swinging from basic to complex concepts. Some praise its practical strategies and business model approach, while others criticize its lack of examples and disorganized structure. The book is generally considered useful but challenging for beginners, with several reviewers suggesting it requires multiple readings to fully grasp the concepts.

People Also Read

Glossary

TOMIC

The One Man Insurance CompanyThe central business framework of the book: running an individual options trading portfolio as if it were an insurance company. TOMIC has three primary functions — Trade Selection (underwriting), Risk Management, and Trade Execution — mirroring a traditional insurer's value chain. Created by co-author Dennis Chen to manage his hedge fund, Smart Income Partners, Ltd.

Units

Cheap OTM catastrophic insurance optionsInexpensive far out-of-the-money options (around $0.10–$0.20 in SPY or $1–$2 in SPX) with near-zero delta and negligible gamma or vega under normal conditions. During extreme market moves, units gain value explosively due to a cascading effect: panic buying raises vega, which raises delta, which accelerates price. The authors recommend spending 5–10% of allocated trading capital on units as portfolio catastrophe insurance.

Card Game Value

Non-model residual option valueThe value that cheap options retain beyond what pricing models predict, caused by asymmetric one-time risk. Named after an analogy: in a one-time card game where 1 of 100 cards pays $1,000, the theoretical value is $10, but rational sellers demand far more because a single bad outcome can never be recouped. Options below about $0.25 hold this residual value stubbornly, and credit spread traders should exit positions once their short option enters Card Game Value territory.

Third Third Third Rule

Iron condor adjustment trigger sequenceA risk management rule for iron condors dividing maximum loss into three equal segments. First adjustment occurs at one-third of maximum loss, second adjustment at two-thirds, and full exit upon hitting the final third. Absolute maximum loss (set at the value of total credit received) serves as a hard ceiling that should never be exceeded. If a 1.5 standard deviation move would breach absolute maximum loss, the trade should be adjusted or exited immediately.

Vomma

Vega sensitivity to IV changesA second-order Greek measuring how sensitive an option's vega is to changes in implied volatility. Front-month at-the-money options have the highest vomma, making them the most responsive to volatility shifts across the entire option chain. Monitoring ATM front-month options via their vomma indicates how implied volatility on any option in the product will likely move.

Kite spread

Condor upside repair adjustmentAn adjustment technique for short call credit spreads under upside pressure. The trader buys one long call below the existing short spread's strikes, then sells 2–3 additional call spreads at higher strikes to finance most of the long call's cost. The resulting risk profile resembles a kite shape. It reduces gamma exposure inexpensively and is the primary upside adjustment for iron condors, though it adds margin and has a 'sour spot' where it can lose money.

Investment skew

OTM puts costlier than ATMThe typical volatility skew pattern in equity and equity index options where out-of-the-money puts have higher implied volatility than at-the-money options, and out-of-the-money calls have lower implied volatility. Caused primarily by institutional hedging behavior: 401(k)s, pension funds, and mutual funds buy puts and sell calls to protect long stock positions, creating persistent demand that bids up put volatility and depresses call volatility.

Five phases of volatility skew

Skew cycle from calm to crisisMark Sebastian's framework describing how volatility skew evolves through market cycles: Phase 1 (Calm) — low IV, normal skew; Phase 2 (Calm Before the Storm) — low IV but steepening skew as protection buying begins; Phase 3 (The Typhoon) — extreme fear, VIX above 30%, but skew actually flattens as ATM IV surges; Phase 4 (The Calming Storm) — IV falling but skew very steep as traders sell ATM but buy OTM puts; Phase 5 — IV normalizes but skew remains slightly elevated for up to six months.

FAQ

What's "The Option Trader's Hedge Fund" about?

- Business Framework for Trading: The book provides a comprehensive framework for trading equity and index options, likening the process to running a hedge fund.

- Insurance Company Model: It introduces the concept of The One Man Insurance Company (TOMIC), where trading options is compared to the operations of an insurance company.

- Risk Management Focus: Emphasizes the importance of risk management, trade selection, and execution as key components of successful trading.

- Practical Insights: Offers real-world perspectives and strategies from the authors' experiences in managing a hedge fund and trading on the floor.

Why should I read "The Option Trader's Hedge Fund"?

- Unique Perspective: The book offers a unique approach by comparing option trading to running an insurance company, providing a fresh perspective on risk management.

- Comprehensive Guide: It covers everything from trade selection to execution, making it a valuable resource for both novice and experienced traders.

- Real-World Examples: The authors share their personal experiences and lessons learned, providing practical insights that can be applied to real trading scenarios.

- Focus on Consistency: The book emphasizes the importance of developing a consistent trading plan and sticking to it, which is crucial for long-term success.

What are the key takeaways of "The Option Trader's Hedge Fund"?

- Framework for Success: Establishing a structured framework for trading options is essential for consistent profitability.

- Risk Management: Effective risk management is crucial, including position sizing, diversification, and protecting against catastrophic events.

- Trade Selection: Selecting the right trades involves understanding market conditions, volatility, and pricing.

- Continuous Learning: The importance of maintaining a trading journal and continuously learning from both successes and failures is emphasized.

How does "The Option Trader's Hedge Fund" compare option trading to an insurance company?

- Risk Transfer: Just like insurance companies, option traders take on risk from others in exchange for a premium.

- Underwriting Process: Trade selection is akin to the underwriting process in insurance, where risks are assessed and priced.

- Reinsurance Concept: Traders can protect against catastrophic losses by buying options, similar to how insurance companies use reinsurance.

- Profit Drivers: Both businesses rely on effective risk management and pricing strategies to ensure profitability.

What is the TOMIC (The One Man Insurance Company) concept in "The Option Trader's Hedge Fund"?

- Business Model: TOMIC is a business framework that treats option trading like running a small insurance company.

- Risk Management: It involves selecting and managing risks, similar to underwriting and claims processing in insurance.

- Trade Execution: The execution of trades is likened to selling insurance policies, focusing on efficiency and effectiveness.

- Support Functions: TOMIC requires a solid infrastructure, including a trading plan, analytical tools, and continuous learning processes.

What are the most used strategies in "The Option Trader's Hedge Fund"?

- Vertical Spreads: These are used for directional plays and can be bullish or bearish, offering positive theta.

- Iron Condors: Suitable for stable or declining volatility, these involve selling out-of-the-money call and put spreads.

- ATM Iron Butterflies: These are used when expecting minimal movement in the underlying asset, benefiting from time decay.

- Calendar Spreads: These involve selling short-term options and buying longer-term ones, capitalizing on term structure differences.

- Ratio Spreads: These are used to take advantage of skew and volatility, often involving buying more options than sold.

How does "The Option Trader's Hedge Fund" emphasize risk management?

- Position Sizing: The book stresses the importance of not risking more than a set percentage of capital on any single trade.

- Diversification: Maintaining a diversified portfolio to avoid overexposure to any one sector is crucial.

- Adjustments: Making timely adjustments to trades can minimize losses and protect capital.

- Insurance Against Catastrophes: Buying out-of-the-money options can protect against unexpected market events.

What is the importance of a trading plan according to "The Option Trader's Hedge Fund"?

- Framework for Decisions: A trading plan provides a structured approach to making trading decisions, reducing emotional influences.

- Consistency: Sticking to a plan helps ensure consistent application of strategies and risk management practices.

- Performance Evaluation: A plan allows for the evaluation of trading performance and identification of areas for improvement.

- Adaptability: While a plan provides structure, it should also allow for flexibility to adapt to changing market conditions.

How does "The Option Trader's Hedge Fund" suggest traders handle volatility?

- Understanding Volatility: Traders should have a strong grasp of how volatility affects option pricing and trading strategies.

- Volatility Skew: Recognizing and exploiting volatility skew can provide trading opportunities.

- Term Structure: Understanding the relationship between different contract months can enhance strategy selection.

- Volatility Management: Monitoring and managing volatility exposure is crucial for maintaining a balanced portfolio.

What are the best quotes from "The Option Trader's Hedge Fund" and what do they mean?

- "Risk is our business." This quote emphasizes the core of trading and insurance, which is about managing and profiting from risk.

- "Failing to plan is planning to fail." Highlights the necessity of having a structured trading plan to guide decisions and actions.

- "The best loss is the first loss." Stresses the importance of taking small losses early to prevent larger, more damaging ones.

- "You are the casino, not the gambler." Encourages traders to focus on maintaining an edge and managing risk, rather than relying on luck.

How does "The Option Trader's Hedge Fund" address the psychological aspects of trading?

- Mindset: The book discusses the importance of having a disciplined and focused mindset for successful trading.

- Emotional Control: Emphasizes the need to control emotions and stick to the trading plan, especially during market volatility.

- Continuous Improvement: Encourages traders to learn from both successes and failures, using them as opportunities for growth.

- Confidence and Humility: Balancing confidence in one's strategies with humility to accept and learn from mistakes is crucial.

What is the role of continuous learning in "The Option Trader's Hedge Fund"?

- Trading Journal: Keeping a detailed trading journal helps track performance and identify areas for improvement.

- Feedback Loops: Regularly reviewing trades and outcomes provides valuable feedback for refining strategies.

- Education Resources: The book suggests utilizing books, seminars, and coaching to enhance trading knowledge and skills.

- Adaptability: Continuous learning ensures traders can adapt to changing market conditions and maintain a competitive edge.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.