Key Takeaways

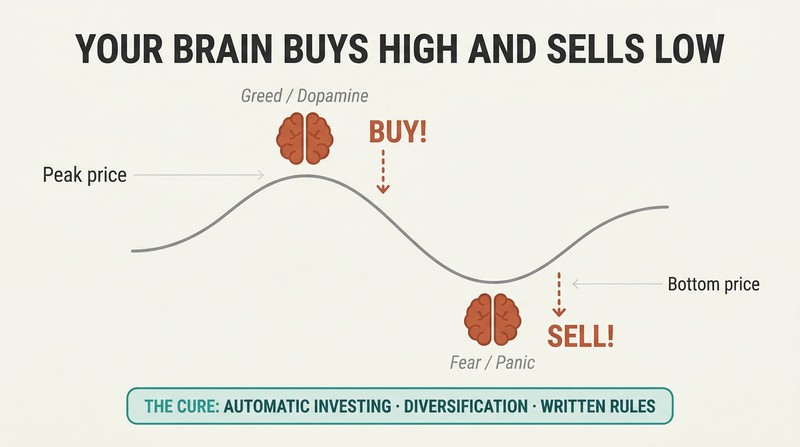

Your brain is hardwired to sabotage your portfolio

Genius doesn't immunize against folly. Sir Isaac Newton bought shares in the South Sea Company, sold for a 100% profit, then got swept back in by the mania, repurchased at a much higher price, and lost £20,000 — over $3 million today. Two Nobel Prize – winning economists at the hedge fund Long-Term Capital Management lost $2 billion in weeks. Graham redefines "intelligent" investing as character — patience, discipline, emotional self-control — not IQ.

Your impulses attack at the worst moments. The pain of a $1,000 loss hits twice as hard psychologically as the pleasure of a $1,000 gain. When stocks rise, dopamine floods your brain; when they crash, your fear center fires and you panic-sell at the bottom. Graham's cure: build systems — automatic investing, diversification, a written investment contract — that override your impulses before they strike.

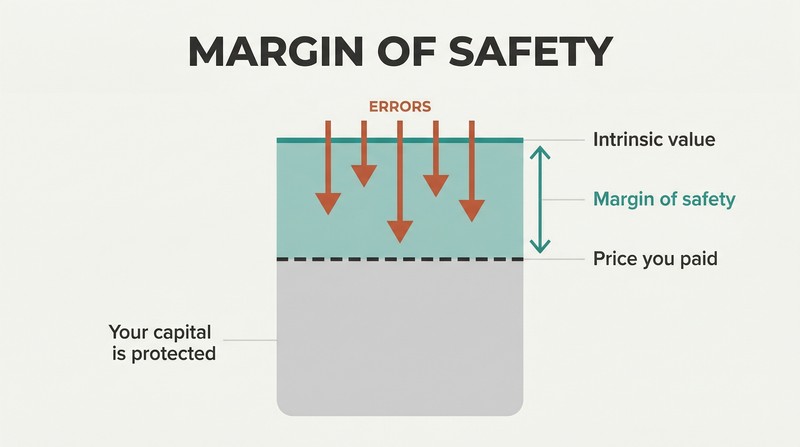

Never pay so much that you can't afford to be wrong

Graham's single most important concept. Margin of safety is the gap between what you pay for an investment and what it's actually worth — a built-in cushion against error, bad luck, or unforeseen downturns. For bonds, it means earnings cover interest charges at least five times over. For stocks, it means buying at a price well below intrinsic value, so even a partly wrong analysis still protects your principal.

Diversification makes the math decisive. A margin of safety on any single stock doesn't guarantee profit — it guarantees better odds. Across twenty or more bargain-priced stocks, the aggregate profits from winners should comfortably exceed losses from duds. Once you lose 95% of your money, you need a 1,900% gain just to break even — which is why avoiding catastrophic loss matters more than chasing spectacular gain.

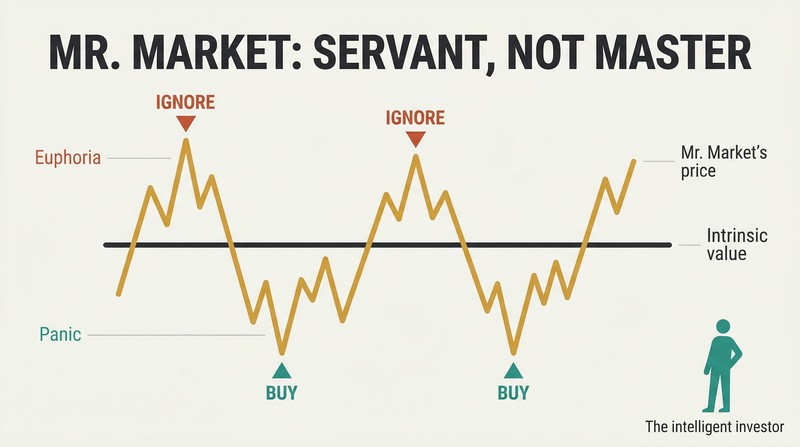

Treat Mr. Market as your servant, never your master

Graham's most famous metaphor. Imagine you co-own a private business with a partner named Mr. Market. Every day he offers to buy your stake or sell you more of his — at a price that swings wildly with his mood. When euphoric, he quotes absurdly high prices; when depressed, he practically gives shares away. You'd never let this manic-depressive set the value of your business — yet that's exactly what happens when stock-price tickers dictate your decisions.

Mr. Market in action. Internet firm Inktomi hit $231 per share in March 2000, valued at $25 billion despite never earning a dime of profit. Thirty months later it traded at 25 cents. Yahoo then bought the entire company for $1.65 per share. When Mr. Market panics, the intelligent investor goes shopping.

Quarantine your gambling money from your investments

Graham draws a bright line. An investment requires three elements: thorough analysis, safety of principal, and adequate — not extraordinary — return. Anything missing those criteria is speculation. The distinction matters because speculators mistake luck for skill, then bet bigger until they're ruined. Finance professors Barber and Odean found that the most active traders underperformed the market by 6.4 percentage points annually after costs.

Build a firewall. Graham advises designating no more than 10% of your total assets as a "mad money" account for speculative plays. Never add more money when it's winning — that's precisely when to take money out. Never mingle speculative and investment operations in the same account or in your thinking. This firewall separates your financial future from your gambling instinct.

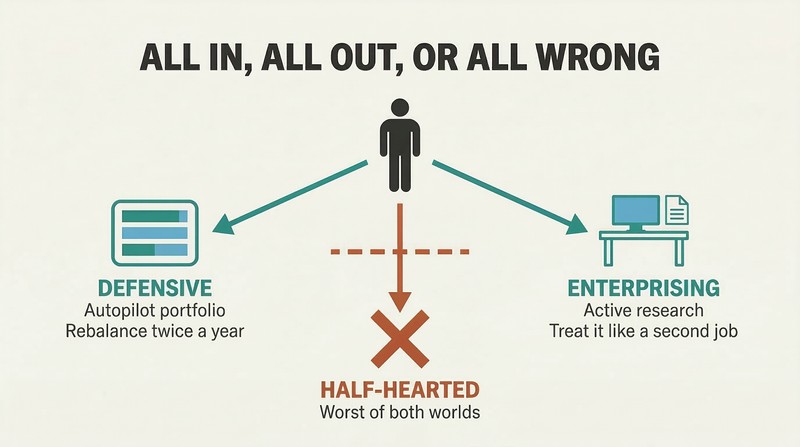

Either invest on full autopilot or treat it like a second job

Two paths, zero shortcuts. Graham divides investors into "defensive" (passive) and "enterprising" (active). The defensive investor wants safety and minimal effort — building an autopilot portfolio of index funds and bonds, rebalanced twice a year. The enterprising investor devotes serious time to researching undervalued stocks, distressed bonds, and special situations, aiming to earn above-average returns through analytical skill.

The middle path is a trap. A half-hearted attempt at stock picking — spending weekends casually browsing financial websites — gives you the worst of both approaches: too much effort for passive investing, too little rigor for active success. If you can't commit to professional-grade analysis, embrace simplicity. The choice hinges entirely on your time and temperament, never on how much risk you can stomach.

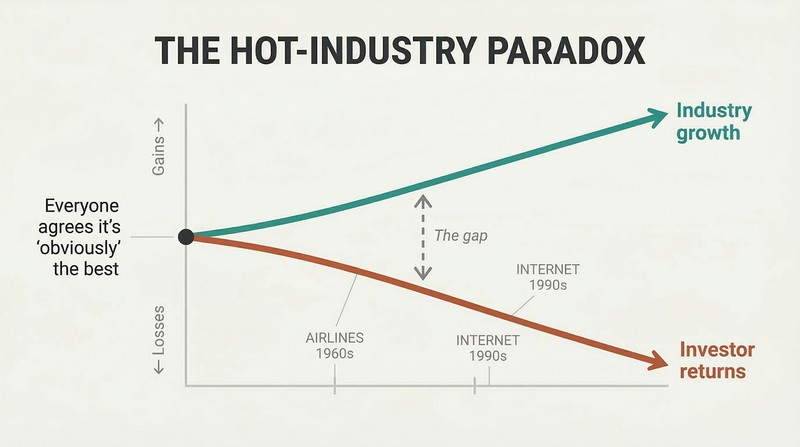

Booming industries reliably produce disappointed investors

The airline paradox is eternal. Air traffic grew spectacularly through the mid-twentieth century — yet airlines lost $200 million for their shareholders in 1970 alone. The same pattern destroyed Internet investors: the technology changed the world, but most tech stocks obliterated their owners' wealth. Even the highly paid experts at mutual funds were completely wrong about the fairly short-term future of these promising industries.

The trap has two jaws. First, when everyone agrees an industry is "obviously" the best, stock prices already reflect that optimism — leaving zero margin of safety. Second, even professionals can't reliably pick winners within a hot sector. Most mutual funds holding computer stocks during the 1960s lost money on every pick except IBM. Predicting an industry's growth and profiting from it are entirely different skills.

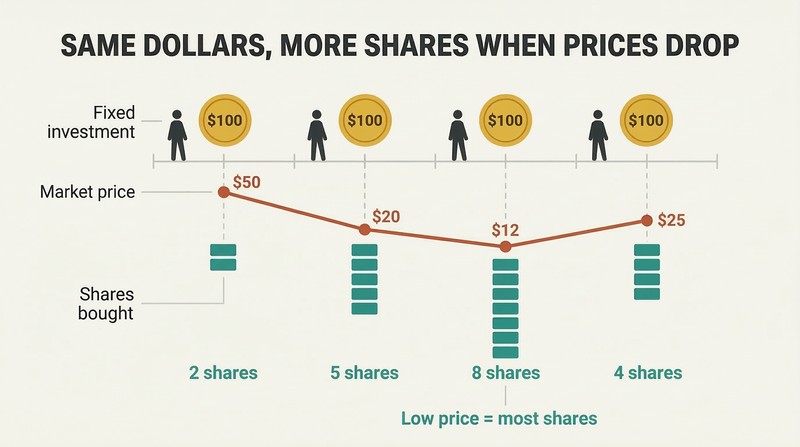

Dollar-cost averaging into index funds, then stop watching

The most powerful strategy requires no talent. Dollar-cost averaging means investing the same fixed amount at regular intervals regardless of market conditions — automatically buying more shares when prices fall and fewer when they rise. If you'd invested $100 monthly in the S&P 500 starting September 1929 — the worst possible timing — you'd have had $15,571 by August 1939. A $12,000 lump sum invested at the peak would have shrunk to just $7,223.

Index funds make it effortless. Both Graham and Buffett endorse total-market index funds as the single best choice for most investors. Own three — U.S. stocks, international stocks, and bonds — set contributions to autopilot, and rebalance every six months. When someone asks you about market conditions, the most powerful answer is: "I don't know and I don't care."

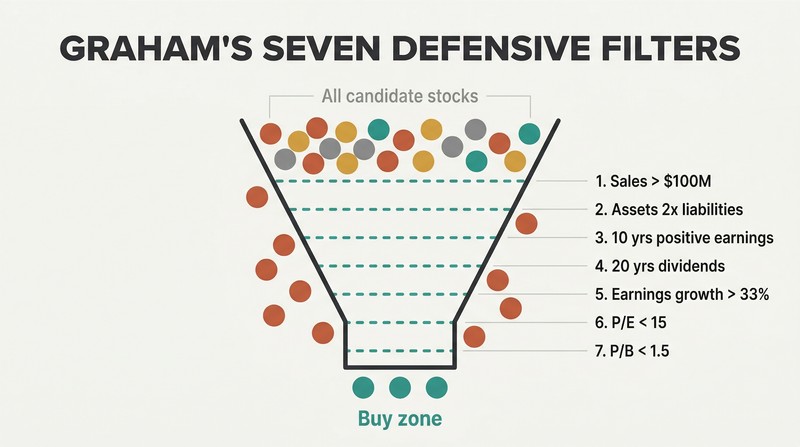

Apply Graham's seven strict filters before buying any stock

A defensive stock screen in seven steps:

1. Adequate size: at least $100 million in annual sales

2. Strong finances: current assets at least 2x current liabilities

3. Earnings stability: positive earnings every year for 10 years

4. Dividend record: uninterrupted payments for 20+ years

5. Earnings growth: at least one-third increase over 10 years

6. Moderate P/E: price no more than 15x three-year average earnings

7. Moderate price-to-book: no more than 1.5x book value

These filters reject glamour by design. Most popular growth stocks fail criteria 6 and 7 — which is the point. Graham wants proven businesses at reasonable prices, not thrilling narratives at thrilling valuations. The combined test (P/E × price-to-book must be under 22.5) enforces a mathematical ceiling on speculation.

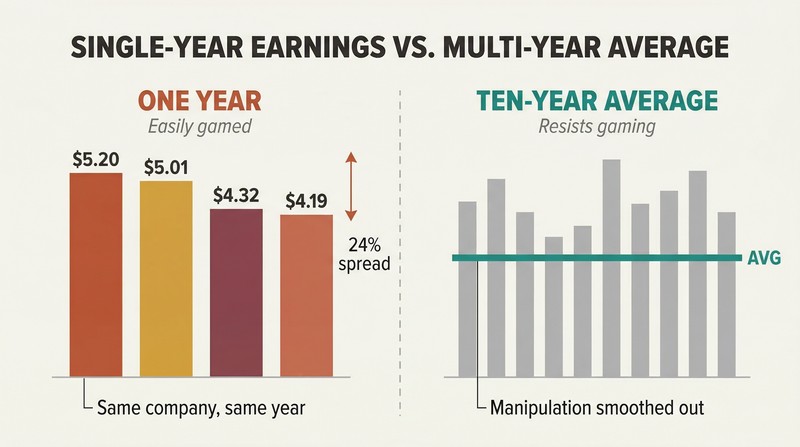

Per-share earnings are easily gamed — always use multi-year averages

One company, four different earnings. In 1970, Aluminum Company of America (ALCOA) reported per-share earnings of $5.20, $5.01, $4.32, or $4.19 — depending on which adjustments you counted. The highest figure was 24% above the lowest. Companies routinely inflate results through "special charges," changes in depreciation methods, pension-fund income assumptions, and pro forma reporting that strips away inconvenient expenses.

Graham's antidote: average over seven to ten years. Short-term earnings are easily manipulated; long-term averages resist gaming. Include all those "nonrecurring" charges — they recur with depressing regularity. Read financial footnotes backward, starting from the last page: anything a company wants to hide is buried at the back. If "extraordinary" costs crop up every year, they are ordinary.

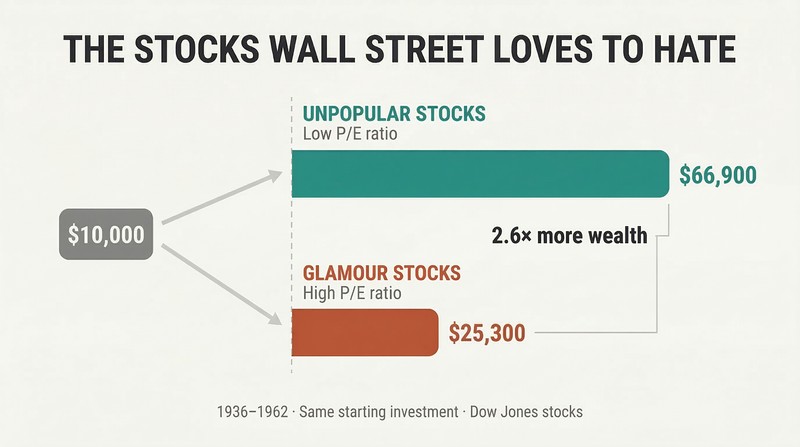

Buy the large, solid stocks Wall Street loves to hate

Unpopular large companies crush glamour stocks. In 25 of 34 annual tests from 1937 to 1969, the lowest-P/E stocks in the Dow Jones Industrial Average outperformed the highest-P/E stocks. An initial $10,000 in low-multiplier stocks in 1936 grew to $66,900 by 1962; the same amount in high-multiplier darlings reached only $25,300 — less than half.

The pattern repeats in every era. In Zweig's updated comparison, Sysco — the institutional food distributor trading at 26 times earnings — trounced Cisco Systems, the Internet juggernaut trading at 219 times earnings. When temporary bad news hammers a strong company's stock, Wall Street often marks it down far below its business value. That gap between price and value is precisely where the enterprising investor's best opportunities hide.

Analysis

The Intelligent Investor is frequently labeled the greatest investment book ever written, an endorsement carried by Warren Buffett himself. But calling it merely an 'investment book' undersells its contribution. At its core, this is a work of applied behavioral psychology disguised as a finance manual. Graham's most enduring insight — that temperament matters more than technique — anticipated the entire field of behavioral economics by decades. Kahneman and Tversky's research on loss aversion and overconfidence would not arrive until the 1970s, yet Graham had already diagnosed the same pathologies and prescribed remedies through his Mr. Market allegory and his insistence on mechanical rules that override emotional impulses.

What makes the book endure is its structural completeness. Graham doesn't merely tell you what to buy — he builds a full decision architecture. The defensive / enterprising distinction forces self-awareness before any stock is purchased. The margin-of-safety concept applies universally across asset classes. The seven stock-selection criteria provide a repeatable screening process. And the written investment contract transforms abstract philosophy into a behavioral commitment device. Few finance books offer this top-to-bottom integration of philosophy, psychology, and process.

The book's limitations deserve acknowledgment. Graham's emphasis on tangible book value has been challenged by the rise of intangible-asset-heavy businesses — software platforms, brand portfolios, network effects — that dominate modern markets. His bond analysis reflects mid-century interest-rate environments now obsolete, and his skepticism toward all growth-stock investing is arguably too sweeping in an era when compounding advantages for dominant technology firms have proved remarkably durable. Zweig's commentary partially bridges these gaps but cannot fully modernize a framework rooted in the industrial economy.

Yet the paradox of investing is that the more markets evolve, the more human psychology stays the same. Every bubble since 1949 has validated Graham's central warning: the investor's chief enemy is not the market but himself. That principle carries no expiration date — and neither, fundamentally, does this book.

Review Summary

The Intelligent Investor is widely regarded as a classic guide to value investing. Readers praise its timeless principles and insights, though some find it dense and outdated. The book emphasizes long-term investing, understanding company fundamentals, and maintaining a margin of safety. Many consider it essential reading for investors, with Warren Buffett's endorsement adding to its reputation. While some struggle with its complexity, others appreciate its depth and historical perspective. The updated commentary by Jason Zweig helps contextualize Graham's teachings for modern readers.

People Also Read

Glossary

Margin of Safety

Cushion between price and valueThe gap between the price paid for a security and its estimated intrinsic value, serving as a buffer against analytical error, bad luck, or market downturns. Graham considers this the central concept of all sound investing. It can be demonstrated through financial data—such as earnings coverage exceeding interest charges by a wide margin, or a stock price well below net asset value—rather than relying on predictions about the future.

Mr. Market

Metaphor for market irrationalityGraham's allegory of a manic-depressive business partner who shows up daily offering to buy your shares or sell you his at wildly fluctuating prices driven by his emotional state. The intelligent investor uses Mr. Market's mood swings as opportunities to buy low and sell high, but never allows Mr. Market to dictate the intrinsic value of holdings. Introduced in Chapter 8, it remains perhaps the most widely cited metaphor in investment literature.

Defensive (passive) investor

Safety-first, low-effort investorOne of Graham's two investor archetypes. The defensive investor's primary goals are avoiding serious mistakes and minimizing the time and effort devoted to portfolio decisions. The recommended approach involves maintaining a diversified portfolio split between high-grade bonds and leading common stocks (or index funds), rebalanced periodically, with strict quantitative criteria for any individual stock purchases.

Enterprising (aggressive) investor

Research-intensive, active investorGraham's second investor archetype. The enterprising investor is willing to devote significant time, energy, and analytical skill to selecting securities that are both sound and more attractive than the average. This may include undervalued large companies, net-current-asset bargain issues, special situations like merger arbitrage, and distressed bonds—always purchased with a demonstrable margin of safety.

Net-current-asset (bargain) issues

Stocks priced below working capitalCompanies whose stock can be purchased for less than their current assets minus all liabilities, effectively valuing the company's fixed assets, plants, and goodwill at zero. Graham's preferred bargain category, which historically produced strong returns when bought as a diversified group. Graham-Newman Corp. required purchasing these at two-thirds or less of net-current-asset value per share.

Earnings power

Sustainable average earning capacityGraham's term for the amount a company could reasonably be expected to earn per year if business conditions during a representative past period were to continue. Calculated using average earnings over seven to ten years rather than a single recent period, earnings power smooths out cyclical fluctuations and one-time distortions, providing a more reliable basis for stock valuation than any single year's reported results.

Dollar-cost averaging

Fixed regular investing regardless of priceA formula investing technique in which the investor commits the same fixed dollar amount to a security or fund at regular intervals—monthly, quarterly, or otherwise—regardless of the current market price. This automatically purchases more shares when prices are low and fewer when prices are high, producing a favorable average cost over time and removing the impossible task of timing the market.

FAQ

What's The Intelligent Investor about?

- Investment Philosophy: The Intelligent Investor by Benjamin Graham focuses on value investing, advocating for a disciplined approach to investing in stocks and bonds. It emphasizes the importance of analyzing a company's fundamentals over market speculation.

- Investor Types: Graham categorizes investors into defensive (passive) and enterprising (active) types, each with tailored strategies for stock selection and portfolio management.

- Market Behavior Insights: The book provides insights into market fluctuations and investor psychology, encouraging rational decision-making and a long-term perspective.

Why should I read The Intelligent Investor?

- Timeless Principles: The book offers investment principles that have proven effective over decades, making it a foundational text for investors. Warren Buffett endorses it as "the best book about investing ever written."

- Risk Management: It teaches risk management through concepts like the "margin of safety," crucial for both novice and experienced investors.

- Behavioral Insights: Graham delves into the psychological aspects of investing, helping readers understand their biases and improve decision-making.

What are the key takeaways of The Intelligent Investor?

- Investment vs. Speculation: Graham defines investment as an operation promising safety of principal and adequate return, contrasting it with speculation, which lacks these assurances.

- Margin of Safety: This central concept advises buying securities below their intrinsic value to minimize risk.

- Market Fluctuations: Investors should view market fluctuations as opportunities, using them to buy low and sell high, rather than reacting emotionally.

What is the "margin of safety" concept in The Intelligent Investor?

- Definition: The "margin of safety" is the difference between a stock's intrinsic value and its market price, providing a buffer against errors and market downturns.

- Risk Minimization: By buying at prices well below intrinsic value, investors protect against unforeseen downturns and judgment errors.

- Practical Application: Investors should assess intrinsic value before purchasing and aim to buy when the market price is significantly lower.

How does Benjamin Graham differentiate between defensive and enterprising investors in The Intelligent Investor?

- Defensive Investors: These investors prioritize safety and minimal effort, typically investing in a balanced portfolio of high-grade bonds and leading common stocks.

- Enterprising Investors: They are willing to devote time and effort to select securities that are sound and more attractive than average, seeking higher returns.

- Investment Strategies: Defensive investors focus on stability, while enterprising investors actively seek undervalued stocks and special situations.

How does The Intelligent Investor address market fluctuations?

- Market Psychology: Graham discusses how market fluctuations are often driven by emotions rather than fundamentals, encouraging rational responses.

- Opportunities in Volatility: Market downturns can present buying opportunities for intelligent investors, who should maintain a long-term perspective.

- Mr. Market Analogy: The "Mr. Market" metaphor illustrates the stock market's irrational behavior, advising investors to use fluctuations as decision-making tools.

What are the best quotes from The Intelligent Investor and what do they mean?

- "The market is a pendulum...": This quote illustrates the cyclical nature of market sentiment, reminding investors to remain grounded.

- "Investing isn't about beating others...": Emphasizes self-discipline and emotional control, suggesting personal behavior is key to success.

- "Those who do not remember the past...": Stresses the importance of historical knowledge in investing, encouraging learning from past cycles.

How can I apply the principles of The Intelligent Investor to my own investing?

- Conduct Thorough Analysis: Perform a thorough analysis of a company’s fundamentals, including earnings and financial health, before investing.

- Establish a Margin of Safety: Aim to purchase stocks at a price significantly below their intrinsic value to create a margin of safety.

- Maintain Discipline: Stick to your investment strategy and avoid emotional reactions to market fluctuations, focusing on long-term goals.

What are the risks associated with investing in common stocks according to The Intelligent Investor?

- Market Volatility: Common stocks are subject to significant price fluctuations, which can lead to temporary losses.

- Overvaluation Risks: High price-to-earnings ratios can expose investors to overvaluation risks, leading to potential losses if the market corrects.

- Psychological Factors: Emotions can be an investor's worst enemy, leading to panic selling or irrational exuberance.

How does Graham suggest handling market downturns in The Intelligent Investor?

- Stay Calm and Rational: Avoid panic selling during downturns and view declines as opportunities to buy quality stocks at lower prices.

- Rebalance Your Portfolio: Consider rebalancing to maintain desired asset allocation, selling stocks that have risen and buying those that have fallen.

- Focus on Fundamentals: Keep focus on the underlying fundamentals of investments rather than market price, trusting that strong fundamentals will lead to recovery.

What role do dividends play in The Intelligent Investor?

- Sign of Financial Health: Dividends indicate a company's financial stability and profitability, often seen as a reliable investment sign.

- Total Return: Dividends contribute significantly to an investor's total return over time, emphasizing their importance in investment strategy.

- Investment Strategy: A strong dividend history can indicate a company's commitment to returning value to shareholders, making it an important evaluation factor.

How does The Intelligent Investor suggest evaluating stocks?

- Fundamental Analysis: Emphasizes examining a company's financial statements, earnings, and business model to assess true value.

- Price-to-Earnings Ratio: Advises using the P/E ratio as a key valuation metric, with a lower ratio indicating potential undervaluation.

- Long-Term Performance: Focus on long-term performance and stability, with consistent earnings growth and solid dividend history as positive indicators.

About the Author

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.