Key Takeaways

Your snap judgments about rich people expose your money ceiling

Rob Moore called a Ferrari driver a "drug dealer." At 24, broke and bitter, he watched his dream car — a Ferrari F430 Spider in rosso red — cruise past. Rather than admire it, he projected envy and bitterness onto a stranger he'd never met. Those seven words captured everything wrong with his money mindset: the beliefs, the self-sabotage, the quiet conviction that wealth equals corruption.

Years later, Moore became a millionaire and bought that exact car. Nothing changed about the world — only his beliefs. If you see wealthy people as evil, you'll unconsciously block your own wealth to avoid becoming what you despise. Every negative money belief you hold — money is the root of evil, the system is rigged, rich people exploit others — is a story you've inherited, not a fact you've verified.

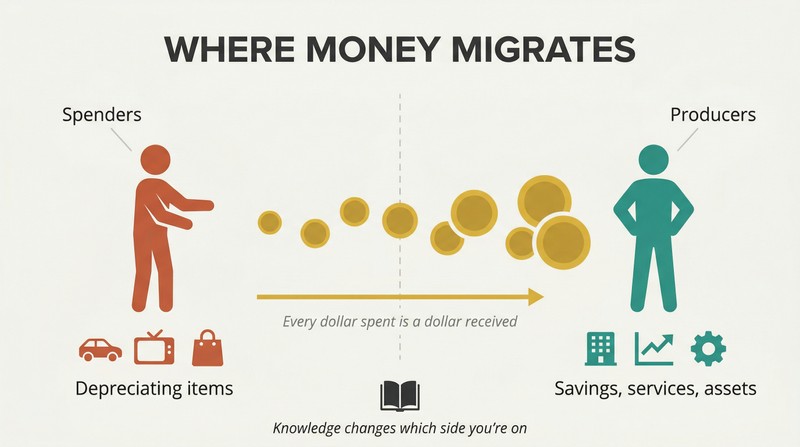

Money migrates from spenders to producers — that's economics, not injustice

In any economy, total spending equals total receipts. The top 3% of Americans hold 54.4% of all US wealth. This isn't theft — it's flow. Money moves from those who prioritize spending on depreciating items to those who prioritize receiving through service, saving, and investing. Consumers fund producers. That's why redistribution alone fails: 70% of sudden windfall recipients lose everything within a few years, and 44% of lottery winners spend it all within five.

The knowledge gap matters more than the wealth gap. If you give more money to someone without financial literacy, they consume it the same way they consumed the last lot. Education — not redistribution — changes the direction of flow. Learn the rules of money, and more flows your way.

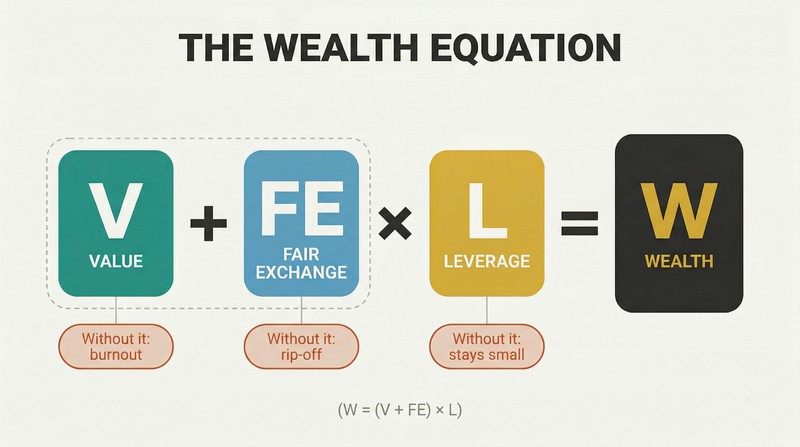

Build wealth using Value + Fair Exchange × Leverage

Moore's formula for wealth is W = (V + FE) × L. Value is the service you provide as perceived by others. Fair Exchange means pricing that leaves both buyer and seller satisfied — not so low you resent it, not so high they feel cheated. Leverage is the scale and speed at which you deliver. All three are required, and in that order.

Each piece without the others fails differently. Value without Fair Exchange creates burnout and resentment — you give endlessly but never earn. Fair Exchange without Value means customers feel ripped off and your reputation collapses. Value plus Fair Exchange without Leverage means you run a nice small business that never scales. The Post-it Note nails all three: universal problem solved (V), pennies each (FE), 6 billion sold annually (L).

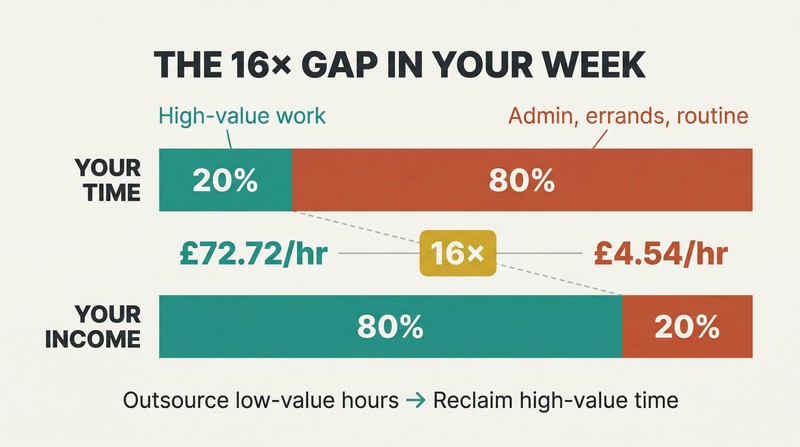

Calculate your hourly worth, then outsource everything below it

Your Income Generating Value reveals a brutal truth. Divide your total weekly income by total hours worked. Earning £1,000 in 55 hours means your IGV is £18.18/hour. Any task costing less than that to outsource — admin, errands, routine operations — should be handed off immediately. Every hour freed flows into higher-value work.

Apply 80/20 and the gap becomes staggering. If 80% of your income comes from 20% of your time, that productive slice earns £72.72/hour — while the remaining 80% earns just £4.54/hour. That's a 16× difference in the same person's week. Double your high-value hours, outsource 60% of the low-value ones, and you earn £270 more per week in 33 fewer hours. Over a decade: £14,000 more income, 1,716 fewer hours worked.

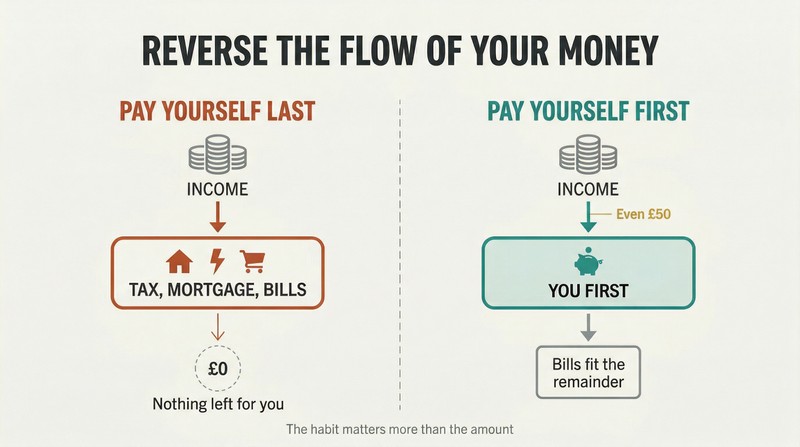

Pay yourself first — even £50 — then force bills into the remainder

Most people pay themselves last. After tax, mortgage, subscriptions, and groceries, nothing survives. Moore calls this Pay Yourself Last — a guaranteed formula for staying broke. The fix is PYF: set up a standing order on payday into a SANT account (Save And Never Touch) before any bills hit. Even £50 reverses the direction of flow.

Moore recommends splitting income into seven "buckets":

1. SANT savings: 5%

2. Irregular shock fund: 5%

3. Bucket list goals: 10%

4. Self-education: 10%

5. Investments: 10%

6. Giving: 5%

7. Living expenses: 55%

If 55% is too tight, start with 80% expenses and 3% savings. The habit of redirecting flow matters more than the amount.

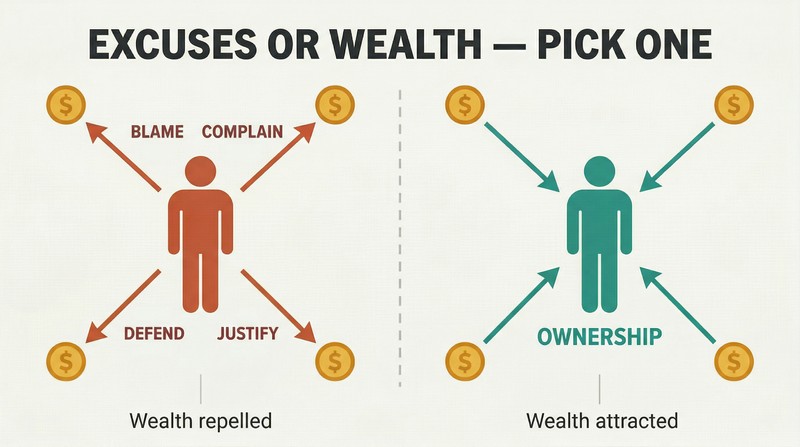

Blame, complaints, defensiveness, and justification repel all wealth

Moore isolates four wealth-killers into one acronym: BCDJ. Blaming the government or economy changes nothing — except other people's opinion of you. Complaining broadcasts that you're someone to avoid. Defending your position drains energy that could go into earning. Justifying your decisions signals self-doubt to everyone watching. All four put you at effect rather than cause.

The antidote is radical personal ownership. Moore suggests a 30-day no-complaining challenge — restart the clock every time you slip. Stop listening to broke people's financial advice. Don't read tabloids. Don't take others' opinions personally. Don't fight battles that aren't core to your vision. The time and emotional energy reclaimed from BCDJ flows directly into income-generating work and clearer decision-making.

Low prices repel your best clients and compound your resentment

Picasso sketched on a napkin and charged a fortune. "It took you a minute!" the admirer protested. "No," Picasso replied, "it took me 40 years." Moore made this exact mistake as a young artist, pricing his work based on canvas costs while ignoring two decades of skill. Low prices attracted bargain hunters and repelled serious collectors — the opposite of what he wanted.

A 10% price increase is nearly invisible to buyers. Just as a 10% portfolio swing triggers no panic, customers absorb modest price changes without strong emotion. Moore recommends raising prices 10 – 20% immediately. If that feels risky, add 4% more perceived value across five areas — speed, service, packaging, personalization, and free extras — and the 20% increase is self-funding through better margins and better clients.

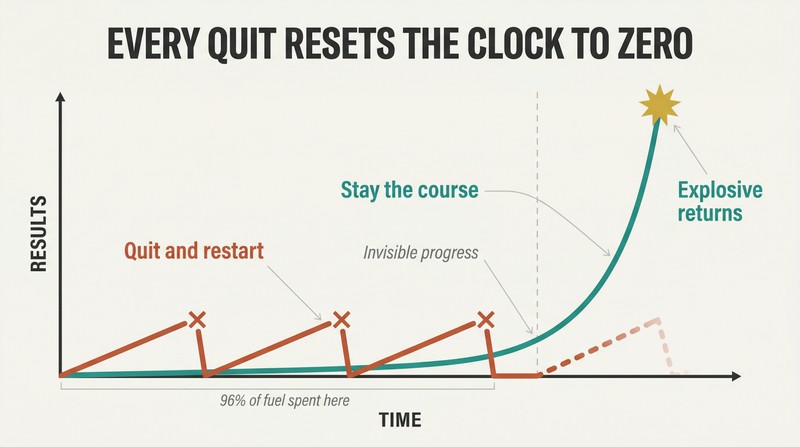

Compounding burns most fuel at liftoff — quitting resets the clock to zero

A space shuttle uses 96.2% of its fuel to get one foot off the ground. The remaining fraction carries it into space and back. Wealth follows the same physics: maximum effort for minimum visible results early on, then explosive returns once momentum builds. A water lily doubles daily and covers half its pond on day 29 — then the entire pond on day 30.

Warren Buffett made 99% of his wealth after age 50. Moore himself earned more in one year after his first million than in the four years it took to reach it. Every time you abandon a venture for the next shiny opportunity, you reset compounding to zero and burn all the fuel again. The cost of change is the cost of erasing your invisible, intangible progress — reputation, network, expertise — that was about to compound.

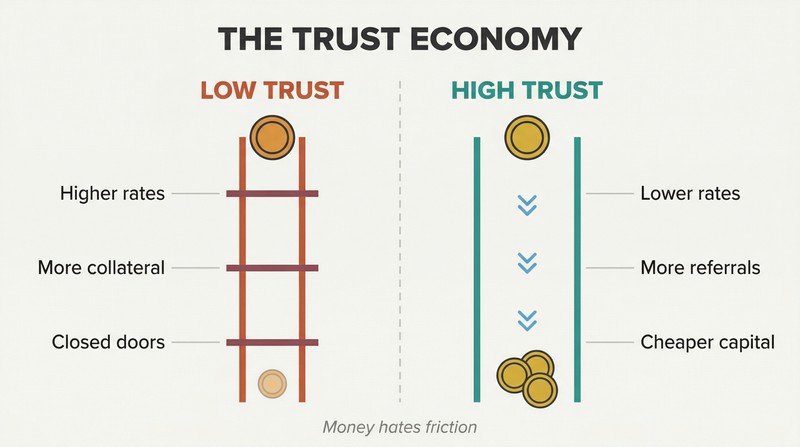

Your reputation is the cheapest and most powerful line of credit

The word "credit" comes from the Latin credere — to trust. Every loan, investment, and deal rests on it. Higher trust means lower interest rates, less collateral, more referrals, and cheaper capital. Lower trust means friction, fees, and closed doors. Moore calls this your personal "Trust economy" — and argues it's your single greatest financial asset.

Practical moves to build trust capital: Never miss a credit card payment — automate every one. Monitor your credit score. If you borrow, always repay, even if you negotiate longer terms. Defaulting isn't just a credit mark; it's a decade-long signal that you can't be trusted. Do what you say you will do, especially when no one is watching. Trust reduces friction, and money hates friction.

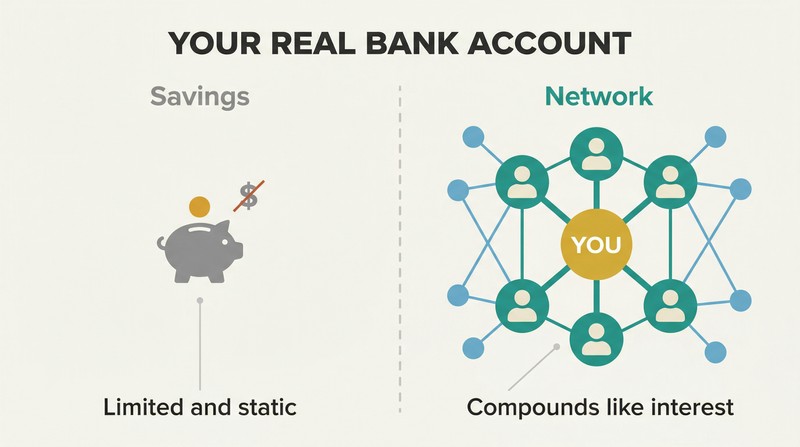

Treat your entire network as your real bank account, not your savings

Your extended bank account isn't cash — it's people. Social networks have shrunk six degrees of separation to 3.9. Every contact is a potential investor, partner, or referral. Bill Gates credits Warren Buffett as his mentor. Buffett credits professor Benjamin Graham. Zuckerberg credits Steve Jobs. The chain of mentors doesn't stop at the top — it's how they got there.

Moore recommends spending up to one-third of working time building relationships. Attend one networking event per week — 52 per year. Aim to be the least wealthy person in the room. When you connect high-net-worth individuals to each other, you become indispensable. The goodwill compounds like interest, with no credit limit and no fees — just trust accumulated over time. Go where money flows, and some flows your way.

Analysis

Moore's contribution to the personal finance genre is less about novel financial mechanics and more about emotional deprogramming. The book's central argument — that money is amoral energy, neither virtuous nor villainous — is philosophically basic but psychologically potent. Most readers picking up this book aren't struggling because they lack an investment strategy; they're struggling because they unconsciously associate wealth with moral corruption. Moore attacks this head-on with the Ferrari anecdote, positioning himself not as an enlightened guru but as a reformed money-hater who once projected his insecurities onto strangers' car choices.

The Formula for Wealth (W = (V + FE) × L) is the book's structural backbone and its most deployable tool. It crystallizes what many business books take 300 pages to articulate: create value, price it fairly, then scale. The formula's diagnostic power — identifying which of the three components is broken — gives it practical utility beyond motivational platitudes.

Where Moore is most original is in synthesizing Bancroft's 1896 Book of Wealth — a 6,700-year study of the wealthy distributed only to families like the Rockefellers and Carnegies — into three surprisingly consistent traits across millennia: service at massive scale, material opulence, and deep financial literacy. This historical lens elevates the book beyond typical 'visualize abundance' fare.

The book's weakness is its sprawl. At 112,000 words, core principles are restated dozens of times — Moore himself acknowledges this. The book would be sharper at a third of its length. Survivorship bias also runs throughout: the argument that wealthy people are generous philanthropists selectively samples billionaires who give publicly while ignoring those who don't. The 80-86% 'self-created' millionaire statistic depends heavily on how you define the starting line — a middle-class family with stability and connections is a significant head start that doesn't register as 'inheritance.' Still, for readers trapped in the cognitive prison Moore describes — believing wealth is inherently immoral — this book provides a systematic, if repetitive, counter-argument backed by economic principles and raw personal candor.

Review Summary

Money: Know More, Make More, Give More receives mixed reviews. Some praise its authentic insights and practical advice on wealth creation, while others criticize its repetitive content and perceived capitalist bias. Positive reviewers appreciate Moore's personal story and mindset-changing approach to finances. Critics argue the book lacks depth, is poorly structured, and promotes a materialistic worldview. Many readers find value in the book's ideas on financial planning and entrepreneurship, though some feel it's best suited for beginners or those interested in starting a business.

People Also Read

Glossary

VVKIK

Five-level priority hierarchyA top-down system for organizing life and business decisions: Vision (life purpose), Values (guiding principles), KRAs (Key Result Areas—the 3-7 highest-impact focus zones), IGTs (Income Generating Tasks—actions that directly produce revenue), and KPIs (Key Performance Indicators—metrics that track progress). Working from the top down ensures daily actions align with long-term wealth goals.

IGV (Income Generating Value)

Your hourly earning rateCalculated by dividing total weekly gross income by total hours worked. For example, £1,000 earned across 55 hours yields an IGV of £18.18/hour. Any task that costs less than your IGV to outsource should be delegated, freeing time for higher-value work. Moore argues this single metric should govern every decision about what to do yourself versus what to hand off.

BCDJ

Four wealth-repelling behaviorsAn acronym for Blame, Complain, Defend, and Justify—four habitual behaviors Moore identifies as the biggest drains on wealth and reputation. Each puts a person in a reactive, victimized position rather than a proactive, wealth-creating one. Moore recommends complete elimination of all four, including a 30-day no-complaining challenge to break the pattern.

Formula for Wealth

Core wealth-building equationW = (V + FE) × L, where W is Wealth, V is Value (service as perceived by others), FE is Fair Exchange (sustainable pricing that satisfies both buyer and seller), and L is Leverage (scale and speed of delivery). All three components are required in sequence: create value first, price it fairly, then scale. Missing any one creates a distinct failure mode.

PYF (Pay Yourself First)

Prioritize savings before expensesA money management principle where you set up automatic transfers to savings and investment accounts on payday, before paying any bills or expenses. The opposite—PYL (Pay Yourself Last)—guarantees nothing remains for savings. Even small amounts like £50 per month change the psychological direction of money flow from outward to inward.

SANT (Save And Never Touch)

Untouchable savings accountA dedicated savings account funded by automatic monthly transfers, intended to build a foundational capital base that is never withdrawn from. It serves as the first 'bucket' in Moore's money bucketing system, creating discipline and a psychological safety net that grows through compounding over time.

YGDP (Your Personal GDP)

Personal money throughput measureModeled on national GDP, this is the total monetary value of all money flowing through your personal economy—spending, investing, earning, and giving combined. Moore argues that wealth isn't just what you store but how much flow you create. Increasing YGDP means increasing transactions, velocity, and the total throughput of money moving to, through, and from you.

4S Model

Product development and scaling systemA four-step business framework: Survey (crowdsource what customers want), Solve (create a product or service addressing those needs), Serve (launch a minimum viable product and iterate based on feedback), Scale (expand once the product is proven). Moore calls it a 'licence to print money' because it eliminates guesswork by building what people have already told you they want.

Money Bucketing

Income-splitting savings systemA system of splitting income into seven purpose-driven 'buckets' via automatic transfers: SANT savings (5%), irregular shock fund (5%), bucket list goals (10%), self-education (10%), investments (10%), charitable giving (5%), and living expenses (55%). Percentages are adjustable based on current income level, with the key principle being that allocation happens automatically on payday before discretionary spending.

First-world poor

Poverty mindset in developed nationsMoore's term for people in developed countries who have access to free information, healthcare, security, and the Internet but maintain a scarcity mindset and unhealthy financial habits. Distinguished from 'third-world poor,' who face genuine structural barriers. Moore argues first-world poverty is primarily a knowledge and belief problem, not a resource problem, and therefore solvable through education and mindset shifts.

FAQ

What is Money: Know More, Make More, Give More by Rob Moore about?

- Comprehensive money philosophy: The book explores the psychology, history, and practical systems of money, aiming to dispel negativity and guilt around wealth.

- Balanced spiritual and material approach: Rob Moore combines spiritual and material perspectives, teaching readers to love money, use it for good, and serve both themselves and others.

- Practical strategies: It covers myths, money mastery, and actionable systems to help readers make, grow, and give more money ethically and sustainably.

- Personal growth and trust: The book emphasizes that trust in yourself attracts money, and personal development is key to building lasting wealth.

Why should I read Money: Know More, Make More, Give More by Rob Moore?

- Break limiting beliefs: The book helps readers reprogram common money myths and limiting beliefs that hold them back from wealth.

- Learn from real experience: Rob Moore shares his journey from debt to millionaire, offering relatable stories and practical advice.

- Holistic wealth approach: It combines mindset, personal development, practical strategies, and ethical giving for a balanced path to wealth.

- Empowerment and mindset: Readers are encouraged to take responsibility, embrace abundance, and develop a positive, strategic money mindset.

What are the key takeaways from Money: Know More, Make More, Give More by Rob Moore?

- Trust is foundational: Trust reduces friction in transactions and is the basis of personal and business reputation.

- Leverage and compounding: Using leverage (time, money, systems, people, ideas) and understanding compounding are essential for exponential wealth growth.

- Personal GDP (YGDP): Wealth is measured by the flow and velocity of money you generate, not just your net worth.

- Philanthropy and purpose: Giving back and having a clear purpose attract more wealth and create a lasting legacy.

What are the major money myths addressed in Money: Know More, Make More, Give More by Rob Moore?

- Money and happiness: The book debunks the myth that money doesn’t make you happy, arguing that it enables more of what brings joy.

- Rich get richer: Moore explains that money flows to those who value it most, emphasizing personal responsibility over victimhood.

- Making money is hard: He stresses that making money is a learnable system, especially with modern technology and opportunities.

- Greed and money: The book reframes greed as growth and highlights the importance of balancing self-interest with contribution.

How does Rob Moore define money and its purpose in Money: Know More, Make More, Give More?

- Money as exchange: Money is an efficient, fair, and universal medium of exchange that replaced barter and solved trade limitations.

- Four economic purposes: It serves as a medium of exchange, unit of account, store of value, and standard of deferred payment.

- Money is trust: The value of money depends on trust and belief; it must keep moving to function effectively.

- Spiritual and material balance: Money is seen as spirit converted into matter, enabling fair exchange and human progress.

What is the "formula for wealth" in Money: Know More, Make More, Give More by Rob Moore?

- Wealth formula: Wealth = (Value + Fair Exchange) × Leverage.

- Value creation: Wealth is built by providing valuable services or solutions that others desire.

- Fair exchange: Sustainable wealth comes from balanced transactions where both parties feel satisfied.

- Leverage: Scaling your value and fair exchange through leverage multiplies your wealth potential.

What is the concept of "You are money" in Money: Know More, Make More, Give More by Rob Moore?

- Trust attracts money: Your personal trustworthiness and reputation act as currency, drawing financial opportunities.

- Trust economy: Building your brand, creditworthiness, and reliability accelerates financial and personal success.

- Fair exchange and relationships: Both lending and borrowing should be fair; greed erodes trust and damages relationships.

- Reputation as leverage: Your reputation, built on proof and trust, influences referrals, costs, and profits in all areas of life.

How does Rob Moore define and suggest growing your personal GDP (YGDP) in Money: Know More, Make More, Give More?

- YGDP definition: Your personal GDP is the total flow and velocity of money you generate through spending, investing, and receiving.

- Growth through flow: Wealth increases by accelerating the movement of money, not just by saving or hoarding.

- Measure and target: Regularly monitor your cashflows—spending, investing, and income—to ensure growth in all areas.

- Balance giving and receiving: Acts of giving, charity, and reinvestment boost both your YGDP and overall wealth.

What are the "five vehicles of leverage" in Money: Know More, Make More, Give More by Rob Moore?

- Time (life): Multiply your time by focusing on high-value tasks and delegating or automating the rest.

- Money (assets): Invest in appreciating assets like businesses, property, and intellectual property for residual income.

- Systems (processes): Create repeatable, automated systems to increase efficiency and reduce reliance on yourself.

- People/skills: Build teams and networks to leverage others’ talents and time, treating relationships as partnerships.

- Ideas and information: Innovate and monetize ideas through information marketing and creative problem-solving.

What is the VVKIK system in Money: Know More, Make More, Give More by Rob Moore and how does it help with money mastery?

- VVKIK defined: Vision, Values, KRAs (Key Result Areas), IGTs (Income Generating Tasks), KPIs (Key Performance Indicators).

- Top-down clarity: Start with a clear vision and aligned values to guide your priorities and decisions.

- Focus on high-value tasks: Concentrate on KRAs and IGTs that directly generate income, delegating or dropping low-value work.

- Measure progress: Use KPIs to track results, optimize efforts, and avoid working hard on the wrong things.

How does Money: Know More, Make More, Give More by Rob Moore address emotions and beliefs around money?

- Emotions rule money: Extreme emotions like fear, guilt, or impatience can sabotage wealth creation; mastering emotions is crucial.

- Beliefs shape reality: Money beliefs are shaped by family, culture, and experience; changing limiting beliefs unlocks wealth potential.

- Strategies for mastery: Observe emotions without judgment, understand their roots, and link spending/investing to your values for balanced decisions.

- Feedback and growth: Seek feedback and continually adjust your beliefs and behaviors to align with your financial goals.

What money management and mastery advice does Rob Moore provide in Money: Know More, Make More, Give More?

- Take responsibility: You are ultimately responsible for your financial well-being; no one else will care as much as you do.

- Financial planning: Set clear short- and long-term goals, get out of debt, budget daily, and build savings and investments.

- Seven layers of money: Understand the full spectrum from spending and saving to borrowing, investing, speculating, insuring, and giving.

- Track net worth and cashflow: Regularly monitor your assets, liabilities, and cashflow to ensure solvency and sustainable growth.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.