Key Takeaways

Buy a running business instead of gambling on a startup

Deibel's startup ViewPoint had everything: a former Microsoft director as CEO, Fortune 500 investors, a top-ten accelerator pedigree, and beta trials inside major corporations. It still died. Then Deibel acquired a print management company for a low six-figure down payment plus a bank loan — and doubled its marketable value within eleven months. The following year, he merged in a second acquired company, boosting revenue 20% and adding 500 customers, all funded by existing cash flow.

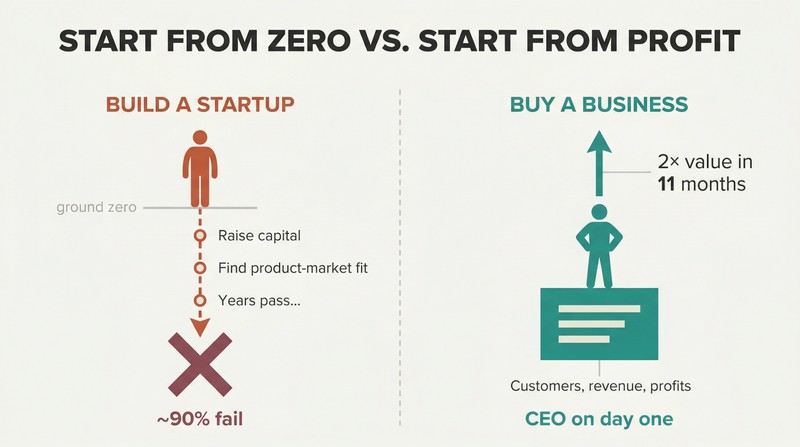

This is acquisition entrepreneurship: buying an existing business with customers, revenue, employees, and profits, then applying entrepreneurial drive to build value. Instead of spending years raising capital and chasing product-market fit, you become CEO on day one with profitable infrastructure already beneath you.

Acquired businesses succeed ~98% of the time; startups ~10%

The numbers are dramatic. SBA loan default rates hover around 2%, meaning acquired businesses carry an approximate 98% success rate. Meanwhile, startups fail roughly 90% of the time. Even VC-backed startups — averaging $41 million in funding with elite investment teams — fail 75% of the time, according to Harvard's Shikhar Ghosh.

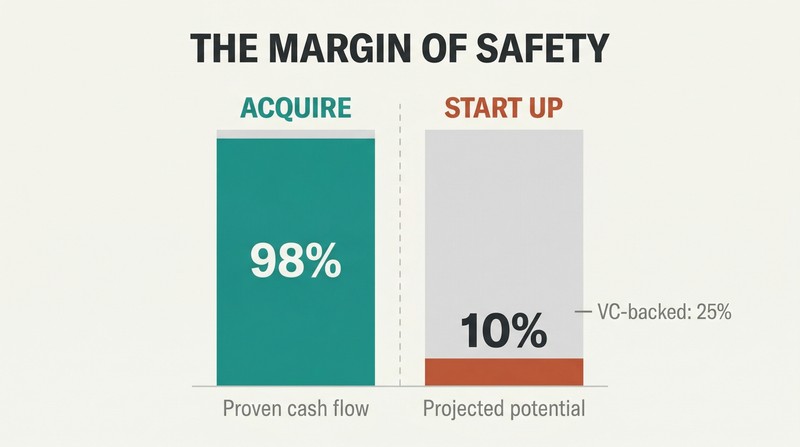

The mechanism is margin of safety, a concept from value investor Benjamin Graham. When you buy a company at 3 – 4x its proven annual cash flow, the valuation is anchored in real earnings, hard assets, and years of operating history. A startup valued on potential has no such anchor. The acquisition entrepreneur builds downside protection simply by starting with profitable revenue, just as Buffett buys securities trading below intrinsic value.

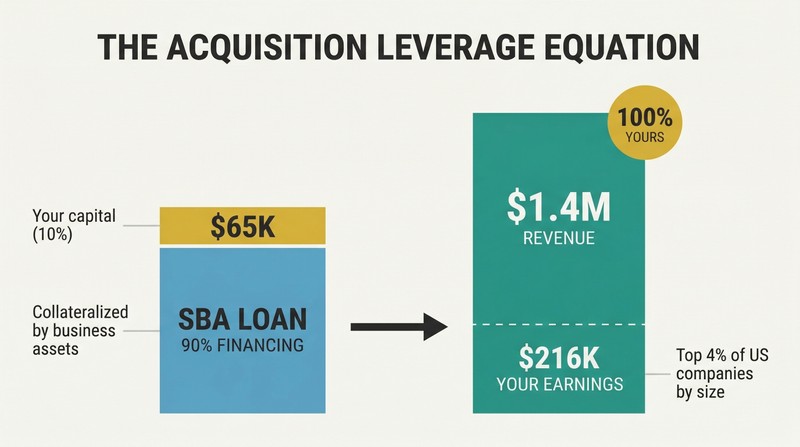

$65K can make you CEO of a million-dollar-revenue company

The math is surprisingly accessible. SBA-backed loans cover up to 90% of the purchase price, using the business's own assets as collateral. The average US startup launches with $65,000 in capital — roughly the same as an average home down payment. That same $65K, paired with a 90% SBA loan, buys a company at around $650,000. At a 3x earnings multiple, that yields about $216,000 in annual Seller Discretionary Earnings from a business generating over $1.4 million in revenue — placing you in the top 4% of US companies by size.

Unlike venture capital, bank financing doesn't require surrendering equity. You keep full ownership. The structure looks more like buying a house than launching a moonshot, with monthly debt payments covered by the company's existing cash flow.

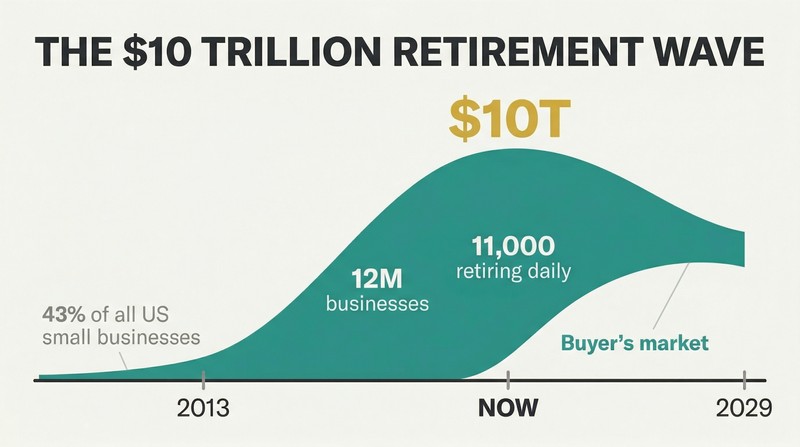

A $10 trillion wave of retiring boomer businesses is cresting now

The demographics are staggering. Baby boomers owned 12 million small businesses as of 2013 — 43% of all US small businesses. They began retiring at 9,000 per day, accelerating to 11,000 daily. By 2029, roughly 77 million people will have retired, and an estimated $10 trillion in existing business value must change hands.

This creates unprecedented opportunity. Established, profitable businesses with decades of operational history will flood the market at the most affordable levels ever experienced. Many operate on legacy systems, lack modern marketing, and have never optimized their operations — precisely the gaps an acquisition entrepreneur is equipped to fill. The infrastructure built by prior generations is available for purchase, often below what it would cost to replicate from scratch.

Align attitude, aptitude, and action before you look at any deal

Deibel's Law of Three As is a self-assessment framework that must precede any deal search:

1. Attitude — cultivate a growth mindset, the top predictor of entrepreneurial success per Carol Dweck's Stanford research

2. Aptitude — honestly inventory strengths and weaknesses (hire a professional assessor; research shows most people overrate themselves)

3. Action — define what you want your daily work to actually look like: sales calls, operations management, digital marketing?

Most buyers skip straight to browsing listings and never define what success looks like personally. They drift for months or years without clarity. The Three As ensure you know where you'll thrive — so when the right company appears, you recognize it instantly rather than endlessly tire-kicking.

Search by cash flow and growth opportunity, not by industry

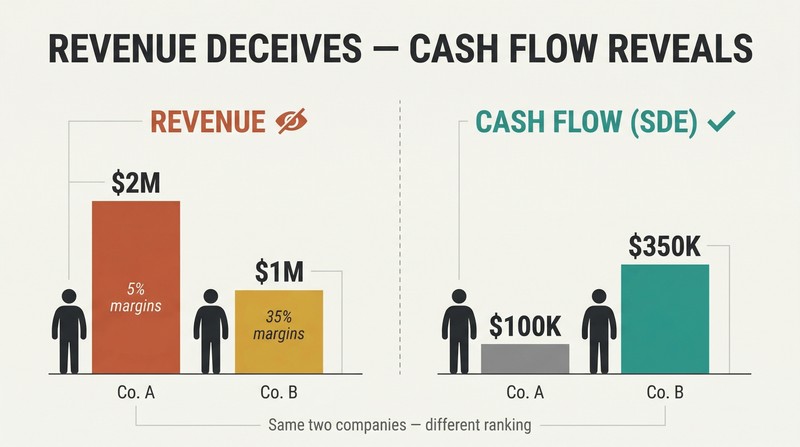

Revenue is a vanity metric when shopping for a business. A $2M company with 5% margins and a $1M company with 35% margins have wildly different values. Deibel insists on defining targets by Seller Discretionary Earnings — the total pretax cash flow the owner enjoys — because that's what you're actually buying.

Build a target statement combining four elements: industry type (product, distribution, or service), the specific growth opportunity your skills unlock, an SDE range you can afford, and any geographic limiters. Deibel identifies four Acquisition Opportunity Profiles — Eternally Profitable, Turnaround, High Growth, and Platform — with Platform being the most common: a solid business whose specific growth gap matches your specific skillset.

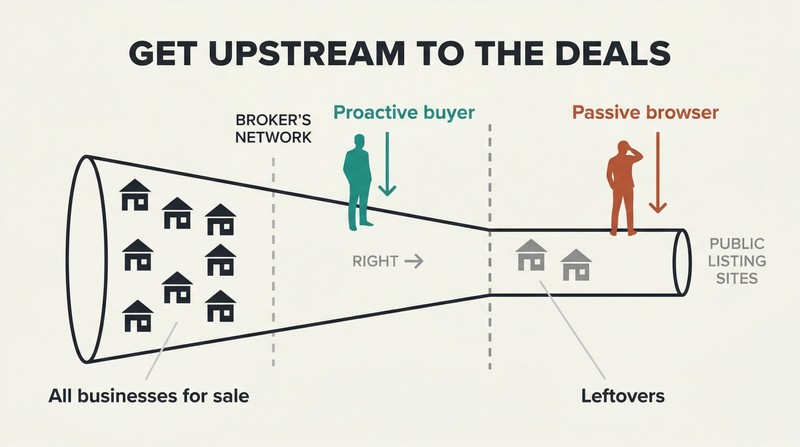

Get upstream to brokers — your deal isn't on BizBuySell

Online listing sites are downstream. Good businesses get shown first to vetted buyers in brokers' private networks. Only after nobody bites do listings hit sites like BizBuySell. Deibel's strategy: meet every intermediary in your area, present your target statement, demonstrate you have financing access, and commit to buying within six months. This conviction is rare, and brokers will prioritize you over less-prepared buyers.

Remember that every business is for sale. Deibel has proactively contacted companies he admired — from eCommerce firms to century-old factories — and reports every single prospect was willing to talk. Recruit a broker to approach targets on your behalf, or reach out directly and introduce a broker once interest develops. Treat your search like a networking campaign, not online window shopping.

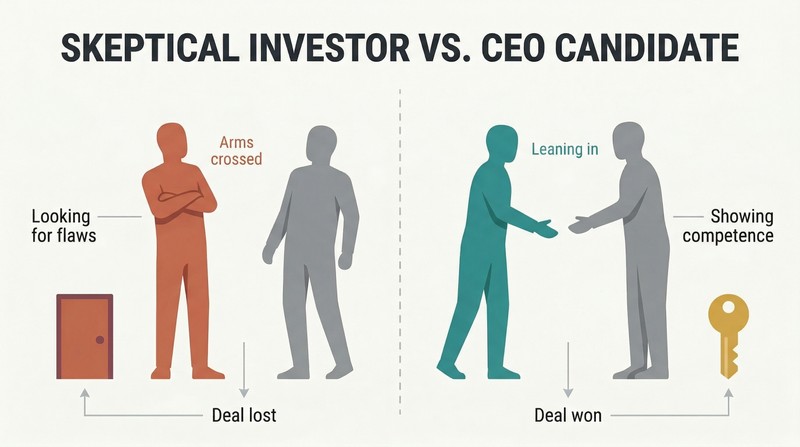

Interview for CEO of the seller's company, not as a skeptical investor

Most buyers get this backwards. They arrive suspicious, arms crossed, expecting a sales pitch — behaving like conservative investors looking for reasons to say no. Deibel treats the first seller meeting like a job interview where he's applying to be CEO of their company. He thanks the seller, compliments specific aspects of their business, shares his background and financing readiness, and demonstrates genuine passion for the opportunity.

This approach wins on three levels. The seller sees you can close, that you're competent to steward their life's work, and that you're a trustworthy partner. Negotiate everything except price before the formal offer — identify what matters to the seller beyond money (employee retention, closing speed, legacy), then give those easy wins freely. Save financial scrutiny for due diligence.

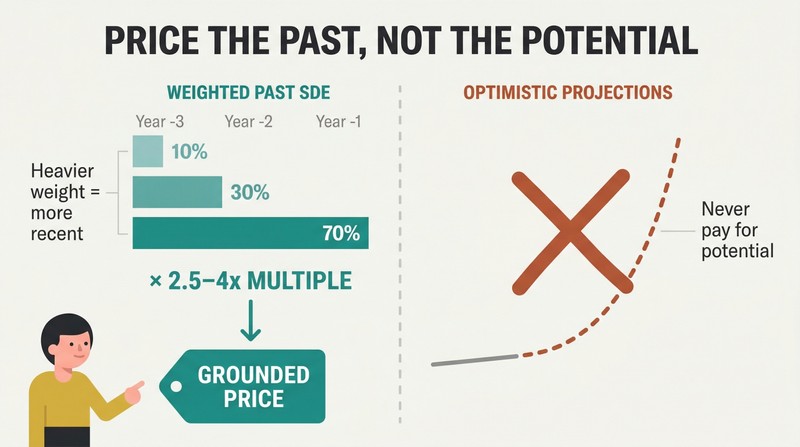

Price acquisitions on past cash flow, not optimistic projections

Ignore the asking price initially. Calculate your own valuation using a weighted average of the last three years' Seller Discretionary Earnings multiplied by a fair multiple — typically 2.5 – 4x for companies under $5M in transaction value. Weight recent performance more heavily: 70% for the most recent year, 30% prior, 10% third year back.

Then stress test the deal. Subtract annual loan payments from SDE, add your minimum salary, and calculate how much revenue must decline before you're in trouble. In Deibel's example, a $400K SDE company financed at 90% could survive a 37% revenue drop before debt became unserviceable. Your future growth is pure upside — never pay for potential you haven't yet created. A $94K initial investment at these terms can compound to over $5.7 million in total pretax returns over eleven years.

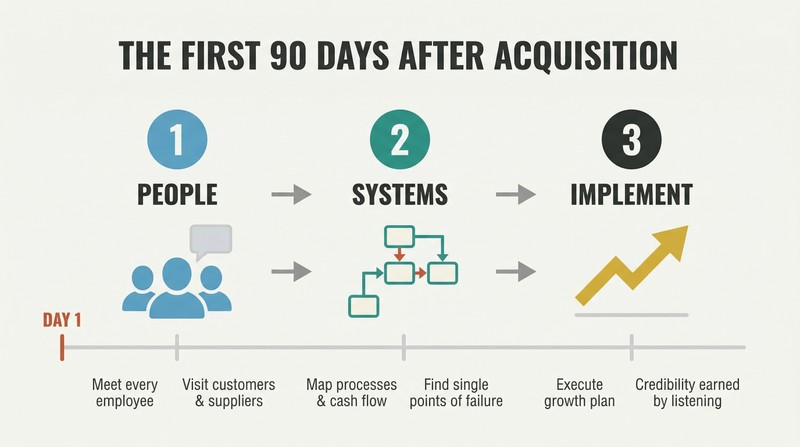

Month one people, month two systems, month three implement

Day one starts with an all-hands meeting where the seller introduces you and exits the stage — ideally for the last time in a leadership role. Immediately address employee fears: are there layoffs? Benefit changes? If the answer is no, say so plainly. Under-promise and over-deliver. Then spend month one in one-on-one meetings with every employee, riding along with salespeople, and visiting top customers and suppliers to build a feedback loop.

Month two, learn the machinery. Map how orders flow through the company, document undocumented processes, build a 13-week cash flow projection, and identify single points of failure. Get the seller out quickly — their emotional connection evaporates once money hits their account. Month three, begin implementing your growth plan with the credibility earned by listening first.

Analysis

Deibel's thesis is elegantly contrarian: the sexiest move in entrepreneurship is the unsexy one — buying what already works. The book functions as a corrective to Silicon Valley mythology, redirecting entrepreneurial energy from the minuscule probability of unicorn creation toward the near-certainty of acquiring profitable infrastructure. Intellectually, it borrows heavily from value investing (Graham, Buffett) and applies that framework to operating businesses rather than securities portfolios.

The strongest contribution is reframing the entrepreneur-investor hybrid identity. Traditional entrepreneurship literature cleanly separates 'founders' from 'investors.' Deibel collapses that distinction, arguing that the acquisition entrepreneur must think as an investor before acting as an operator — a sequence reversal that produces fundamentally different risk profiles. This is the book's deepest insight and one that challenges both the MBA startup track and the traditional private equity career path.

Where the argument is most vulnerable is in its treatment of execution risk post-acquisition. Substantial energy goes to search and deal mechanics, but the arguably harder challenge — actually running and transforming someone else's company — compresses into a single chapter. The cultural integration problem, acknowledged through an anecdote about a friend who clashed with inherited employees for years, deserves far deeper treatment. Private equity's mixed track record with operational transformation suggests this gap isn't trivial.

The timing argument around baby boomer retirements is compelling but warrants nuance. While $10 trillion in business value will change hands, many boomer-owned businesses are lifestyle companies with owner-dependent revenue, limited documentation, and deferred maintenance — precisely the characteristics that make acquisitions difficult regardless of price.

Still, Deibel's core proposition holds: for aspiring entrepreneurs with moderate capital and operational instincts, buying a profitable business and innovating from that base is a dramatically under-discussed path. The book's greatest service is making an invisible market visible and providing a structured process for navigating it. In an era of declining job security and accessible SBA financing, acquisition entrepreneurship deserves the mainstream attention this book argues it warrants.

Review Summary

Buy Then Build receives mostly positive reviews for its comprehensive guide on acquiring small businesses. Readers appreciate the practical advice, frameworks, and insights into the acquisition process. Many find it eye-opening and helpful for those considering entrepreneurship through acquisition. However, some criticize the book for overselling opportunities, lacking real-world examples, and containing typos. Critics also note that it's US-centric and doesn't deeply cover topics like valuation. Overall, reviewers consider it a valuable resource for understanding the potential of buying existing businesses.

People Also Read

Glossary

Acquisition Entrepreneurship

Buying businesses to build valueThe practice of buying an existing, profitable business instead of starting one from scratch, then applying entrepreneurial innovation and management to grow its value. Deibel positions this as a hybrid of private equity investing and traditional entrepreneurship, combining the margin of safety of proven cash flow with the upside potential of entrepreneurial drive.

Seller Discretionary Earnings (SDE)

Total pretax owner cash flowA measure of the total pretax cash flow benefit to the owner of a small business. Calculated by taking pretax earnings and adding back interest, depreciation, amortization, owner's salary, personal benefits, and any one-time expenses. SDE is the primary metric used to value privately held companies in the lower middle market. In larger deals, the equivalent term is Adjusted EBITDA.

Law of Three As

Self-assessment before acquisition searchDeibel's framework requiring aspiring acquisition entrepreneurs to align three personal attributes before searching for a company: Attitude (growth mindset and motivation), Aptitude (skills, strengths, and weaknesses), and Action (desired daily activities and preferred work style). All three must work in harmony for a successful acquisition and operation.

Acquisition Opportunity Profiles

Four types of target companiesDeibel's four-quadrant matrix categorizing acquisition targets by their growth and value characteristics: Eternally Profitable (stable, low-disruption cash cows), Turnaround (distressed businesses needing operational improvement), High Growth (fast-growing companies commanding premium multiples), and Platform (businesses whose specific growth gap matches the buyer's specific skillset). Each profile carries distinct risk-reward tradeoffs.

Target Statement

Compass for acquisition searchA concise description of the ideal acquisition target, structured as: 'I am looking for a [product/distribution/service] company with [specific growth opportunity], generating [SDE range], with [geographic or other limiters].' Used to communicate precisely with brokers, bankers, and contacts during the search process, replacing the typical vague industry-based approach.

Platform Company

Acquisition matched to buyer's skillsIn acquisition entrepreneurship, a company whose specific growth opportunity aligns with the buyer's personal strengths, goals, and desired daily activities. Unlike the private equity definition (which focuses on industry entry for bolt-on acquisitions), Deibel's platform concept emphasizes the match between the company's growth gap and the individual operator's skillset as the primary selection criterion.

Eternally Profitable

Disruption-resistant stable businessAn acquisition target serving a need unlikely to disappear, operating in a mature market with high barriers to entry and minimal technological disruption risk. Examples include snow removal, plumbing, and utility-adjacent services. Characterized by stable, predictable cash flow but limited growth potential. Concept drawn from Ruback and Yudkoff's HBR Guide to Buying a Small Business.

Eleventh Hour Freakout

Buyer panic near closingTerm used by Quiet Light Brokerage's Jason Yelowitz describing the common phenomenon of buyers developing heightened anxiety as closing approaches. As due diligence reveals operational realities, the initial allure may diminish and the weight of financial commitment intensifies. Deibel considers it normal and manageable, not a reason to walk away absent material adverse change in business performance.

Gazelles

Fast-growing job-creating companiesTerm coined by economist David Birch for the 2–3% of companies responsible for creating roughly 70% of new jobs annually. To qualify, a company must start with at least $1 million in revenue and grow at 20% annually for four consecutive years. Research by Birch and Zoltan Acs found gazelles average 25 years old and span all industries, contradicting the assumption that high growth belongs exclusively to startups or technology firms.

FAQ

What's Buy Then Build about?

- Acquisition Entrepreneurship Focus: Buy Then Build by Walker Deibel centers on acquisition entrepreneurship, where entrepreneurs purchase existing businesses instead of starting new ones. This strategy offers immediate cash flow and established customer bases.

- Framework for Success: The book provides a comprehensive framework for navigating the acquisition process, including identifying, evaluating, and executing business deals.

- Market Opportunity: Deibel highlights the wealth transfer as baby boomers retire, presenting a unique opportunity to acquire businesses at favorable prices.

Why should I read Buy Then Build?

- Practical Guidance: The book offers actionable advice for acquiring businesses, making it a valuable resource for both novice and experienced entrepreneurs.

- Real-World Examples: Deibel shares personal experiences and case studies, providing relatable insights into acquisition entrepreneurship.

- Emerging Trend: As acquisition entrepreneurship gains popularity, the book prepares readers to capitalize on current market opportunities.

What are the key takeaways of Buy Then Build?

- Acquisition Over Startup: Buying an existing business is often more advantageous than starting a new one, due to established infrastructure and customer bases.

- Financial Metrics Importance: Understanding metrics like Seller Discretionary Earnings (SDE) is crucial for evaluating business value and potential.

- Mindset Shift: The book encourages viewing entrepreneurship as acquiring and improving existing businesses, opening new avenues for success.

What is Acquisition Entrepreneurship as defined in Buy Then Build?

- Definition: Acquisition entrepreneurship involves buying an existing business and applying entrepreneurial skills to enhance its value.

- Benefits: This approach reduces risk, provides immediate cash flow, and leverages existing infrastructure for growth.

- Market Opportunity: The aging baby boomer population creates a favorable environment for acquiring businesses.

How does Buy Then Build suggest evaluating a business for acquisition?

- Financial Performance Review: Analyzing financial statements like income and balance sheets is crucial for assessing business health.

- Seller Discretionary Earnings (SDE): Understanding SDE helps determine business value and informs purchase price.

- Market Position and Growth Potential: Evaluating market position and growth potential is essential for identifying operational improvements.

What are the common pitfalls in acquisition entrepreneurship mentioned in Buy Then Build?

- Lack of Preparation: Failing to prepare adequately can hinder the acquisition process; having a clear target statement is crucial.

- Overlooking Due Diligence: Skipping thorough due diligence can lead to costly mistakes; verifying financial and operational health is vital.

- Ignoring Seller's Perspective: Not considering the seller's motivations can hinder negotiations; building rapport is essential.

What is the significance of Seller Discretionary Earnings (SDE) in Buy Then Build?

- Key Valuation Metric: SDE is critical for evaluating a business's financial performance and determining its value.

- Impact on Purchase Price: The purchase price is often based on a multiple of SDE, aiding in informed offers and negotiations.

- Comparison to Revenue: Focusing on SDE provides a clearer picture of profitability and cash-generating ability.

What strategies does Buy Then Build recommend for finding acquisition opportunities?

- Networking with Brokers: Building relationships with brokers helps tap into deal flow before public listings.

- Direct Outreach: Reaching out to business owners directly can uncover hidden opportunities.

- Utilizing Online Resources: Online listings are valuable for initial research, but should not be solely relied upon.

What are the financial considerations when acquiring a business as per Buy Then Build?

- Leverage and Financing: Using leverage can enhance return on investment, but associated risks must be managed.

- Understanding Cash Flow: Evaluating cash flow is crucial for determining debt serviceability and returns.

- Budgeting for Expenses: Accounting for all potential expenses, including closing costs, is essential for successful transactions.

What mindset shifts does Buy Then Build advocate for aspiring entrepreneurs?

- From Startup to Acquisition: Shifting focus from starting new businesses to acquiring existing ones opens new opportunities.

- Embracing a Growth Mindset: Viewing challenges as learning opportunities is crucial for navigating acquisition complexities.

- Commitment to Action: Proactive action and urgency in the acquisition process are necessary for seizing opportunities.

What is the role of due diligence in the acquisition process according to Buy Then Build?

- Verification of Information: Due diligence involves verifying financial, legal, and operational information for accuracy.

- Identifying Risks: It helps uncover potential risks or liabilities, crucial for informed decision-making.

- Comprehensive Understanding: Due diligence covers legal, financial, and operational aspects for a thorough business assessment.

What are the best quotes from Buy Then Build and what do they mean?

- “To hell with circumstances; I create opportunities.”: This quote by Bruce Lee emphasizes a proactive mindset in entrepreneurship, encouraging control over circumstances.

- “Results are gained by exploiting opportunities, not by solving problems.”: Focus on growth and potential rather than merely addressing issues for successful entrepreneurship.

- “The difference between ordinary and extraordinary is that little extra.”: Small, additional efforts can lead to significant outcomes in business and life.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.