Key Takeaways

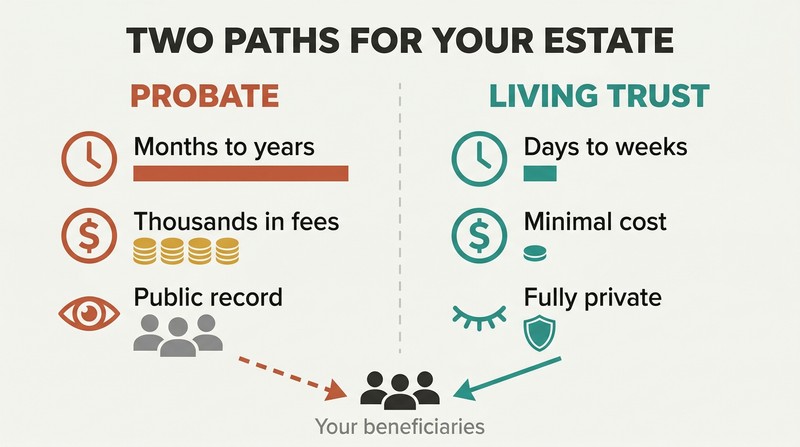

A living trust bypasses probate — saving months, thousands, and privacy

A living trust is a legal arrangement where you transfer ownership of your assets to a trust during your lifetime. You remain in control as trustee while alive, but upon your death or incapacity, a pre-designated successor trustee distributes assets directly to your beneficiaries — no court involvement needed.

Probate is the alternative, and it's brutal. It's the court-supervised process of validating a will and distributing an estate. It's public, so anyone can see your assets and beneficiaries. It's expensive, with legal fees consuming significant estate value. And it's slow — sometimes dragging on for years while your family waits. A living trust sidesteps all of this: direct transfer, no court delays, no public exposure, and streamlined handling even for property across multiple states.

Living trusts aren't just for the rich — DIY options start at $50

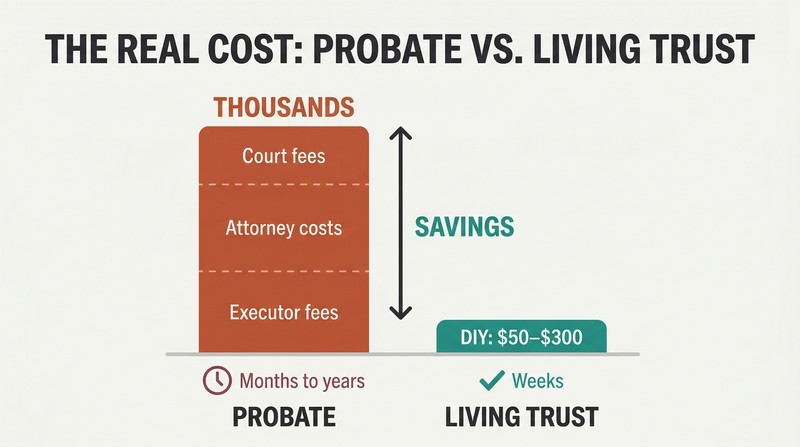

The biggest myth in estate planning is that living trusts are exclusively for the wealthy. In reality, even modest estates benefit enormously from avoiding probate's costs and delays. Attorney-drafted trusts range from a few hundred to a few thousand dollars depending on complexity, but online DIY services offer templates for $50 to $300.

The long-term math overwhelmingly favors trusts. By avoiding probate, a living trust can save thousands in court fees, attorney costs, and executor expenses. It also delivers assets to beneficiaries potentially months or years sooner. The book emphasizes that living trusts are "the unsung heroes for middle-income families" — the upfront investment, whether professional or DIY, typically pays for itself many times over compared to the probate gauntlet your heirs would otherwise face.

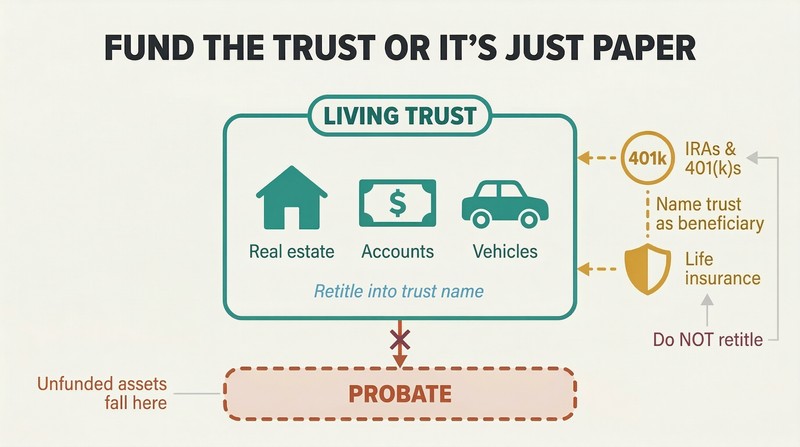

An unfunded trust is worthless — retitle every asset into it

Creating the trust document is only half the job. The trust controls nothing unless assets are formally titled in its name. Real estate requires new deeds. Bank and brokerage accounts must be retitled. Vehicles, art, and personal property need updated ownership documents. Skip this step, and those assets pass through probate anyway — defeating the entire purpose.

Critical exceptions exist. Retirement accounts like IRAs and 401(k)s generally should not be retitled into a trust because doing so can trigger immediate tax consequences. Instead, name the trust as the account's beneficiary. Life insurance works similarly — the trust can be the policy's beneficiary rather than its owner. Conduct a comprehensive asset inventory and consult an attorney to ensure nothing falls through the cracks.

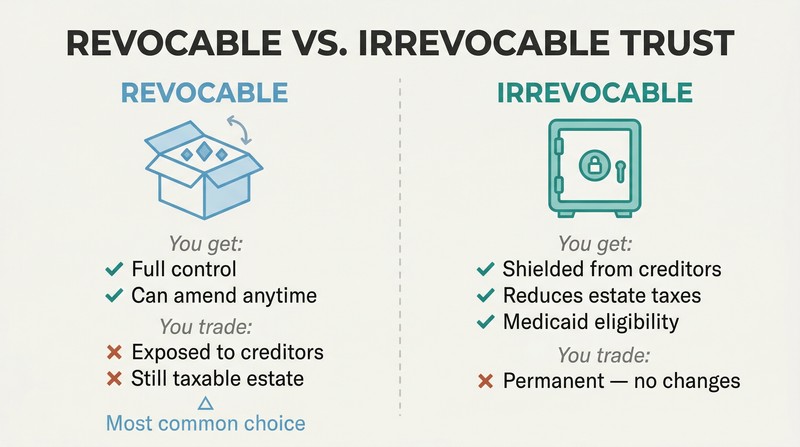

Pick revocable for flexibility, irrevocable for asset protection

This is the pivotal decision. A revocable living trust lets you modify, amend, or dissolve the trust anytime during your lifetime. You maintain full control. The trade-off: assets remain part of your taxable estate and are vulnerable to creditors and legal judgments.

An irrevocable trust flips that equation. Once established, it can't be changed — you permanently give up control. In exchange:

1. Assets are generally shielded from creditors and lawsuits

2. Assets are removed from your taxable estate, potentially reducing estate taxes

3. Beneficiaries may qualify for government benefits like Medicaid

Most people choose revocable trusts for everyday flexibility. Irrevocable trusts serve those with larger estates, asset protection needs, or specific tax-planning objectives.

Add a pour-over will to catch assets you forgot to transfer

A pour-over will is your trust's safety net. It's a legal document directing any assets not already in the trust at death to be transferred into it, ensuring everything gets distributed according to the trust's terms. Without one, overlooked or newly acquired assets could end up in probate — exactly the process you created the trust to avoid.

Important caveat: assets passing through a pour-over will still go through probate before landing in the trust. So it's a backstop, not a substitute for properly funding your trust. Think of it as the net beneath the tightrope. You should still retitle assets directly into the trust whenever possible, and rely on the pour-over will only for what slips through the cracks.

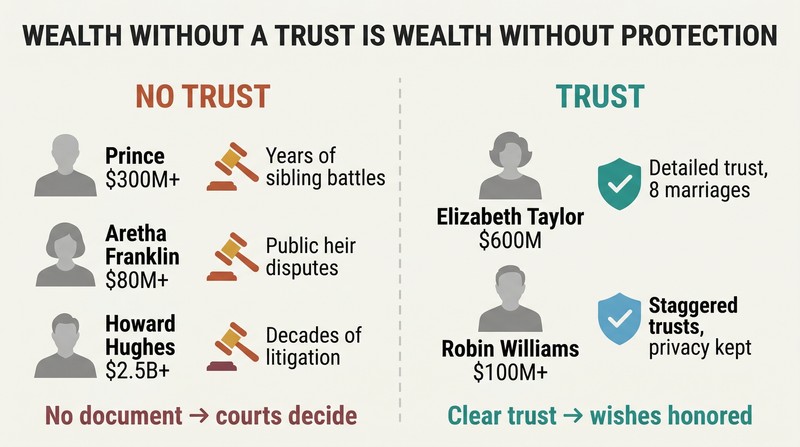

Without a formalized trust, even hundred-million-dollar estates implode

The celebrity graveyard of estate planning is instructive. Prince died in 2016 without a will or trust — his estate, worth hundreds of millions, triggered years of court battles among siblings. Aretha Franklin died without a clear, formal will, sparking a drawn-out public fight among her heirs. Howard Hughes, a billionaire, died in 1976 with no estate documents at all, generating years of litigation from multiple claimants.

Contrast this with those who planned. Elizabeth Taylor proactively managed her $600 million estate through a detailed trust adjusted across eight marriages. Robin Williams created trusts with staggered distributions for his children, preserving family privacy. The difference isn't wealth or fame — it's whether you put your wishes into a legally binding, unambiguous document before it's too late.

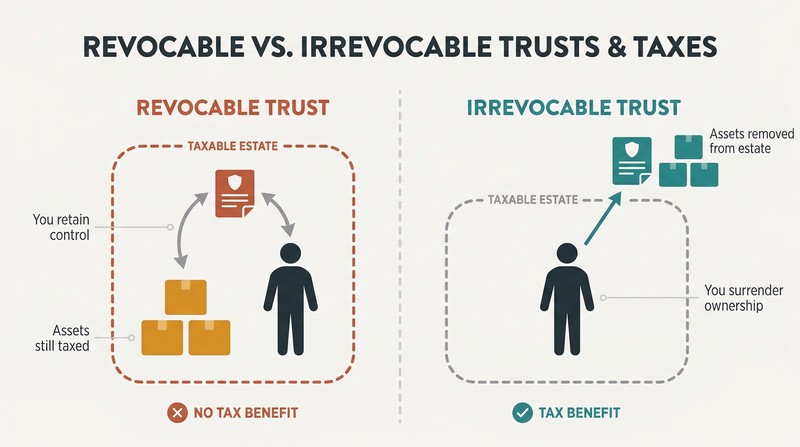

Revocable trusts don't cut estate taxes — that's a costly myth

Many people assume any trust reduces taxes. It doesn't. Assets in a revocable trust are still counted as part of your taxable estate because you retain control during your lifetime. Only irrevocable trusts — where you permanently surrender ownership — remove assets from your taxable estate.

The numbers matter. The 2025 federal estate tax exemption is $13.99 million per individual ($27.98 million for married couples), so most estates won't face federal taxes today. But this exemption is projected to drop to roughly $7 million per individual in 2026. Actor James Gandolfini's $70 million estate reportedly faced up to $30 million in taxes because trusts weren't used optimally. For larger estates, irrevocable life insurance trusts, charitable lead trusts, and generation-skipping trusts can dramatically reduce the tax burden.

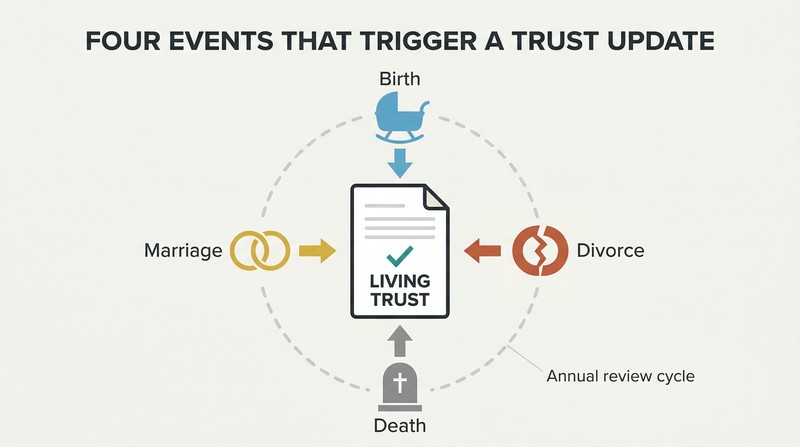

Update your trust after every birth, death, marriage, or divorce

A trust is not a set-and-forget document. Marriage may require adding a spouse as beneficiary or co-trustee. Divorce demands removing a former spouse. New children or grandchildren need to be added, potentially with age-based distribution conditions. Death of a named beneficiary or trustee requires reassignment.

Conduct an annual trust check-up covering:

1. Updated asset inventory compared against trust holdings

2. Beneficiary designations reflecting current relationships

3. Trustee and successor trustee suitability

4. Changes in tax laws or state regulations

5. Whether amendments suffice or a full restatement is needed

For minor changes, a formal amendment works. But when multiple amendments accumulate and risk confusion, a restatement — rewriting the entire trust while maintaining the original entity and date — is cleaner and more legally airtight.

Your crypto, social media, and domain names belong in your trust

Digital assets are real assets. Cryptocurrency holdings, domain names, online businesses, social media accounts, and digital photo libraries can carry significant financial or sentimental value. Yet most estate plans ignore them entirely, leaving these assets inaccessible or permanently lost when the owner dies.

To incorporate digital assets, catalog everything — usernames, passwords, private keys, seed phrases — and store this information securely but accessibly for your trustee. Consider appointing a digital executor with the technical knowledge to manage these assets. Platform terms of service may restrict account transfers after death, so legal guidance matters. Because digital holdings change faster than physical ones, review your digital asset inventory more frequently than your overall trust — the book recommends at least annually.

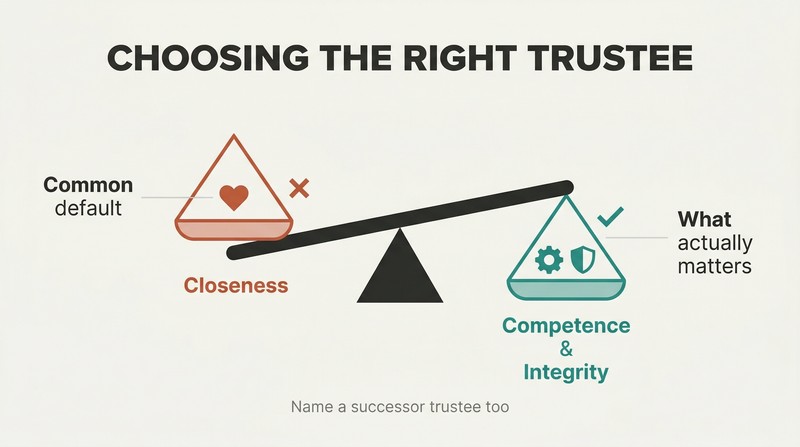

Pick your trustee for competence and integrity, not closeness

Your trustee manages every dollar in your trust — investments, distributions, tax filings, record-keeping, fiduciary duties. Choosing a family member purely out of loyalty, without considering their financial literacy, is one of the most common mistakes in trust planning. An individual trustee offers personal connection and lower cost but may lack expertise. A corporate trustee like a bank brings professional management and continuity but charges percentage-based fees and may feel impersonal.

Name at least one successor trustee in case the primary can't serve. The Brooke Astor estate scandal, where her son was accused of exploiting her diminishing mental capacity to amend estate documents, illustrates what happens without clear succession. Communicate your choices to everyone involved — trustee, successors, and beneficiaries — while you're still able to explain your reasoning.

Analysis

Monroe's book occupies a peculiar niche in personal finance literature — it's a popularized legal guide trying to make a fundamentally dry topic accessible to the median American household. The core insight is sound: for most families, a living trust represents the single most cost-effective estate planning tool available, yet cultural mythology continues to associate trusts with wealth far beyond the median net worth. The book succeeds in democratizing this tool through celebrity cautionary tales — Prince, Aretha Franklin, Howard Hughes — that make the abstract consequences of poor planning viscerally concrete.

Where the book reveals its limitations is in the tension between accessibility and precision. Writing under a team pseudonym, the authors occasionally oversimplify, particularly around creditor protection, where the vast behavioral difference between revocable and irrevocable structures deserves sharper treatment. The 2025-2026 estate tax cliff — with the individual exemption projected to halve from $13.99 million to roughly $7 million — is arguably the most time-sensitive insight in the book, yet receives only passing treatment when it could anchor an entire chapter of urgent action items. The digital assets chapter represents the book's most forward-looking contribution. Most estate planning guides published even five years ago barely mention cryptocurrency or social media, yet these assets constitute a growing share of net worth for younger Americans. The practical guidance on cataloging digital credentials and appointing a digital executor fills a genuine gap.

Notably absent is any substantive discussion of state-level variation. Trust law differs materially across jurisdictions — community property versus common law states, states with and without inheritance taxes — and the book treats these differences as an afterthought. This gap is perhaps the strongest argument for the professional counsel the authors repeatedly recommend. For readers wanting a conceptual map of living trusts before engaging an attorney, this book delivers. For those hoping to execute entirely solo, the jurisdictional omissions warrant caution.

People Also Read

Glossary

Pour-Over Will

Catches unfunded trust assets at deathA legal document that directs any assets not already placed in a living trust at the time of the trustmaker's death to be transferred into the trust. This acts as a safety net ensuring all assets are distributed according to the trust's terms. Assets passing through a pour-over will still go through probate before entering the trust.

Successor Trustee

Takes over when trustee can'tAn individual or institution designated in the trust document to assume management of the trust if the original trustee can no longer serve due to death, incapacity, or resignation. The successor trustee has the same fiduciary duties and powers as the original trustee, including managing assets, making distributions, and filing tax returns according to the trust's terms.

Crummey Powers

Enable gift tax annual exclusionA provision in an irrevocable trust that gives beneficiaries a limited window (typically 30 days) to withdraw contributions made to the trust. By granting beneficiaries this temporary right of withdrawal, the contribution qualifies as a 'present interest' gift, making it eligible for the annual gift tax exclusion rather than counting against the donor's lifetime exemption.

Trustmaker

Person who creates the trustThe individual who initiates and establishes a living trust, also known as the grantor or settlor. The trustmaker decides the trust's terms, selects beneficiaries, appoints trustees, and transfers assets into the trust. In a revocable trust, the trustmaker typically serves as their own initial trustee, retaining full control over the assets during their lifetime.

Grantor Retained Annuity Trust (GRAT)

Transfers asset growth tax-freeA type of irrevocable trust where the grantor transfers assets into the trust and receives an annuity payment back for a set term. Any asset growth exceeding the annuity payments passes to beneficiaries at the end of the term with minimal or no gift tax. GRATs are particularly effective for transferring appreciating assets out of a taxable estate.

Generation-Skipping Transfer (GST) Trust

Passes wealth to grandchildren directlyA trust that transfers assets directly to grandchildren or later generations, bypassing the children's generation. This avoids estate taxes that would apply if assets passed through each generation sequentially. GST trusts are subject to their own tax rules and exemptions, separate from estate and gift taxes, and are typically used by families with larger estates seeking multi-generational wealth preservation.

Dynasty Trust

Multi-generational estate tax minimizationA long-term trust designed to pass wealth across multiple generations while minimizing estate taxes at each generational transfer. Unlike standard trusts that terminate after one or two generations, dynasty trusts can last for the maximum period permitted by state law—in some jurisdictions, perpetually. They extend tax advantages beyond immediate heirs, potentially saving significant taxes over decades.

Digital Executor

Manages online assets after deathA person designated in a trust or estate plan to manage the trustmaker's digital assets after death or incapacity. Responsibilities include executing instructions for social media accounts, cryptocurrency holdings, email accounts, digital businesses, and online subscriptions. The digital executor should be technically competent and understand platform-specific policies governing posthumous account access and transfer.

FAQ

1. What’s "The Only Living Trusts Book You’ll Ever Need" by Garrett Monroe about?

- Comprehensive Living Trust Guide: The book is a step-by-step manual for understanding, creating, and managing living trusts, with a focus on avoiding probate, protecting heirs, and minimizing taxes.

- Accessible for All Readers: It breaks down complex estate planning concepts into clear, actionable advice suitable for people at any stage of wealth or life.

- Covers Modern Estate Issues: The book addresses not only traditional assets but also digital assets, business interests, and the impact of changing laws.

- Practical Tools Included: Readers get access to downloadable forms and checklists, making it easier to implement the strategies discussed.

2. Why should I read "The Only Living Trusts Book You’ll Ever Need" by Garrett Monroe?

- Avoid Probate Hassles: The book explains how living trusts can help you bypass the lengthy, costly, and public probate process, ensuring a smoother transfer of assets.

- Protect Your Heirs and Assets: It provides strategies to safeguard your family’s inheritance from legal disputes, creditors, and unnecessary taxes.

- Adaptable to Life Changes: The book teaches how to keep your trust current as your life, family, and finances evolve.

- Expert-Backed, Actionable Advice: Written by a team of estate planning professionals, it offers real-world examples and practical steps for readers to follow.

3. What are the key takeaways from "The Only Living Trusts Book You’ll Ever Need"?

- Living Trusts Are for Everyone: You don’t need to be wealthy to benefit from a living trust; they offer advantages for estates of all sizes.

- Probate Avoidance and Privacy: Living trusts help keep your estate matters private and speed up asset distribution.

- Flexibility and Control: Revocable trusts allow you to change your estate plan as your circumstances change, while irrevocable trusts offer asset protection and tax benefits.

- Ongoing Maintenance is Crucial: Regular reviews and updates ensure your trust remains effective and aligned with your wishes.

4. What are the most important concepts and definitions explained in "The Only Living Trusts Book You’ll Ever Need"?

- Living Trust: A legal document that places your assets under the management of a trustee for the benefit of your chosen beneficiaries, effective during your lifetime.

- Revocable vs. Irrevocable Trusts: Revocable trusts can be changed or revoked by the trustmaker, while irrevocable trusts cannot, offering different levels of control and protection.

- Trustee and Successor Trustee: The person or institution managing the trust, with successor trustees stepping in if the original trustee can’t serve.

- Pour-Over Will: A will that transfers any assets not already in the trust into it upon your death, acting as a safety net.

- Digital Assets: The book covers how to include online accounts, cryptocurrencies, and digital business assets in your estate plan.

5. How does Garrett Monroe’s book explain the process of creating a living trust?

- Step-by-Step Blueprint: The book guides you through choosing the right type of trust, selecting beneficiaries, and appointing trustees.

- Asset Inventory and Funding: It emphasizes the importance of listing all assets and properly transferring them into the trust to ensure effectiveness.

- Drafting and Legal Formalities: Advice is given on drafting the trust document, notarizing it, and ensuring it complies with state laws.

- Professional Guidance: While DIY options are discussed, the book recommends consulting an estate planning attorney for complex situations.

6. What are the main benefits of using a living trust, according to "The Only Living Trusts Book You’ll Ever Need"?

- Probate Avoidance: Assets in a living trust bypass the court-supervised probate process, saving time and money.

- Privacy Protection: Trusts keep your estate details out of the public record, unlike wills that go through probate.

- Incapacity Planning: If you become incapacitated, your successor trustee can manage your assets without court intervention.

- Customizable Asset Distribution: You can set specific terms for how and when beneficiaries receive their inheritance, including for minors or special needs individuals.

7. How does "The Only Living Trusts Book You’ll Ever Need" address common misconceptions about living trusts?

- Not Just for the Wealthy: The book debunks the myth that only rich people need living trusts, showing their value for all estate sizes.

- Cost-Effectiveness: It clarifies that while there are upfront costs, living trusts often save money in the long run by avoiding probate fees.

- Revocable vs. Irrevocable Confusion: The differences, pros, and cons of each type are clearly explained to help readers choose the right option.

- Limitations of Trusts: The book is honest about what trusts can and cannot do, such as not shielding all assets from creditors or taxes.

8. What tax strategies and implications are covered in "The Only Living Trusts Book You’ll Ever Need"?

- Estate and Gift Tax Planning: The book explains how to use trusts to minimize estate and gift taxes, including leveraging annual exclusions and lifetime exemptions.

- Income Tax Considerations: It details how trust income is taxed, the responsibilities of trustees, and strategies for minimizing tax burdens.

- Special Trust Structures: Advanced strategies like charitable trusts, generation-skipping trusts, and irrevocable life insurance trusts are discussed for tax efficiency.

- Staying Current with Laws: Readers are advised to monitor tax law changes and adjust their trusts accordingly.

9. How does Garrett Monroe’s book guide readers on updating and maintaining their living trust?

- Life Event Triggers: The book stresses updating your trust after major events like marriage, divorce, births, deaths, or significant changes in wealth.

- Annual Reviews: Regular check-ups are recommended to ensure all assets are included and trustee/beneficiary designations are current.

- Amendments vs. Restatements: It explains when to make simple amendments versus when to restate the entire trust for clarity.

- Professional Support: Consulting with estate planning professionals is encouraged for legal compliance and effective updates.

10. What risks, drawbacks, and limitations of living trusts are discussed in "The Only Living Trusts Book You’ll Ever Need"?

- Not a Cure-All: Trusts can’t protect against all creditors, taxes, or legal challenges, especially if not properly funded or managed.

- DIY Pitfalls: The book warns against creating trusts without professional help, as mistakes can lead to invalid documents or unintended consequences.

- Hidden Costs: Ongoing legal, tax, and management fees can add up, and the book provides strategies to manage these expenses.

- Family Dynamics: Trusts can cause or reveal family tensions, so clear communication and documentation are essential.

11. How does "The Only Living Trusts Book You’ll Ever Need" address the impact of living trusts on beneficiaries?

- Faster Inheritance: Beneficiaries often receive assets more quickly than through probate, but delays can still occur due to complex terms or disputes.

- Tax Implications: The book explains how distributions may be taxed as income or subject to inheritance tax, depending on the trust structure and state laws.

- Trustee Limitations: Trustees must act in beneficiaries’ best interests, but their powers are limited by the trust document and state law.

- Beneficiary Rights: Beneficiaries can challenge trustee decisions if there’s mismanagement or breach of fiduciary duty.

12. What does "The Only Living Trusts Book You’ll Ever Need" say about managing digital assets and modern estate planning challenges?

- Digital Asset Inclusion: The book provides guidance on cataloging and including digital assets—like social media, cryptocurrencies, and online businesses—in your trust.

- Legal and Privacy Issues: It discusses navigating data privacy laws and service agreements to ensure digital assets are accessible and transferable.

- Appointing Digital Executors: Readers are advised to designate someone to manage digital assets and provide clear instructions in the trust.

- Regular Updates Required: Because digital assets change frequently, the book recommends regular reviews to keep your estate plan current and comprehensive.

Bonus: What are the best quotes from "The Only Living Trusts Book You’ll Ever Need" and what do they mean?

- “By failing to prepare, you are preparing to fail.” — Benjamin Franklin: Emphasizes the importance of proactive estate planning to avoid future problems.

- “A man who does not plan long ahead will find trouble at his door.” — Confucius: Highlights the necessity of thinking ahead in managing your legacy.

- “Change is the law of life. And those who look only to the past or present are certain to miss the future.” — John F. Kennedy: Encourages readers to regularly update their estate plans to reflect life’s changes.

- “In this world, nothing is certain except death and taxes.” — Benjamin Franklin: Reminds readers that tax planning is an unavoidable part of estate management.

- “The greatest use of a life is to spend it on something that will outlast it.” — William James: Inspires readers to create a legacy that benefits future generations through thoughtful planning.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.