Key Takeaways

A single card game reveals how Wall Street really thinks about risk

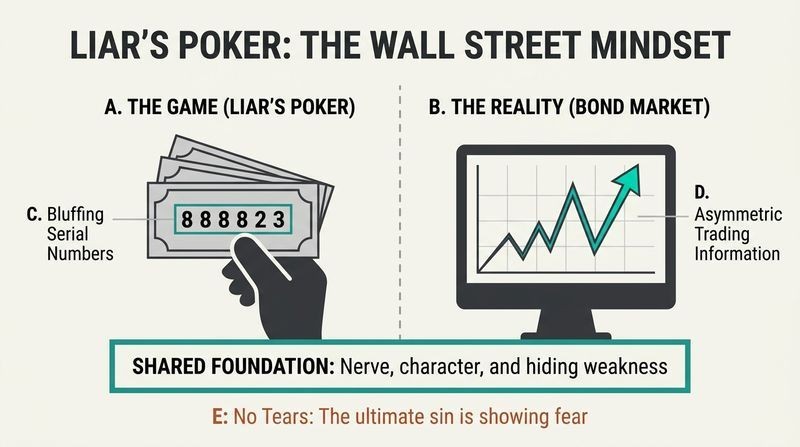

The game is the culture. Liar's Poker is played with dollar bills: traders bluff about the serial numbers, escalating bids until someone calls a challenge. It rewards probability, nerve, and reading faces. In 1986 Salomon's chairman John Gutfreund challenged his best trader, John Meriwether, to one hand for a million dollars, adding "no tears" (the loser must not complain). Meriwether coolly raised him to ten million, knowing his boss would fold. He was bluffing before the game even started.

Traders believed the game mirrored bond trading itself: a test of character where you exploit weakness and hide your own. The best players controlled the two emotions that destroy traders, fear and greed. Lewis uses this ritual to frame an entire era of quick killings.

What's striking is how a trivial game becomes a diagnostic for temperament. Behavioral economists would recognize Liar's Poker as an iterated game of asymmetric information, closer to poker than chess because reading opponents matters more than raw calculation. Meriwether's counteroffer is a classic signaling move: raising the stakes to make the challenger reveal his true resolve. The detail that matters most is "no tears," a norm that punishes emotional leakage. Modern research on professional poker players confirms the edge: the skill is less about the cards than about tolerating variance without tilting. Salomon simply institutionalized this temperament and paid millions for it.

Bond traders profit as toll takers, not gamblers

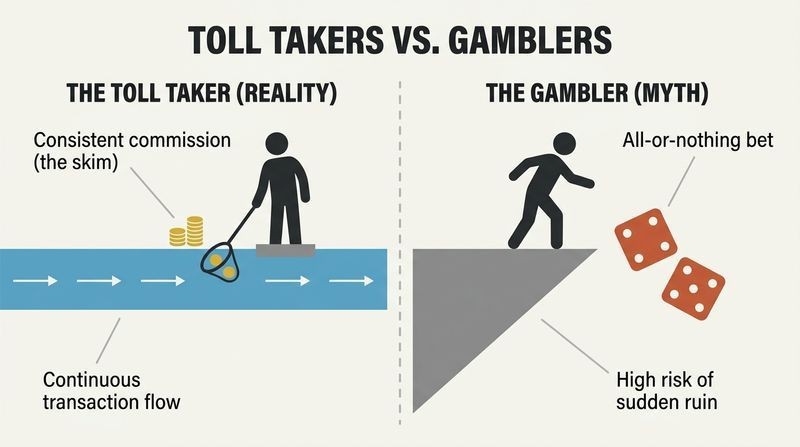

They tax the flow, they don't bet the ranch. The biggest myth is that traders make fortunes by taking huge risks. Most act as middlemen, skimming a tiny fraction from each transaction. Sell 50 million dollars of IBM bonds and the trader quietly pockets an eighth of a percentage point, about 62,500 dollars, and unlike stocks, bond commissions are hidden. He can then pressure a salesman to talk another client into buying the same bonds higher, generating a fresh slice.

Lewis borrows Kurt Vonnegut's image: there is a magic instant when a treasure passes from one hand to another, and the alert middleman makes that instant his own, keeping a little each time. The genius is not prediction. It is standing in the middle of an enormous river of money.

This reframing deserves emphasis because the public still imagines Wall Street wealth as heroic speculation. In reality much of it resembles a rent extracted from opacity. The hidden bond commission is the key mechanism: without transparent pricing, the intermediary captures information rents that would evaporate in a liquid, quoted market. This is precisely what later electronic bond platforms and regulations like TRACE began to erode, compressing spreads exactly as Lewis's own account predicts. The economic lesson generalizes far beyond finance: whenever a market lacks price transparency and buyers cannot easily comparison shop, the middleman, not the risk taker, captures the surplus.

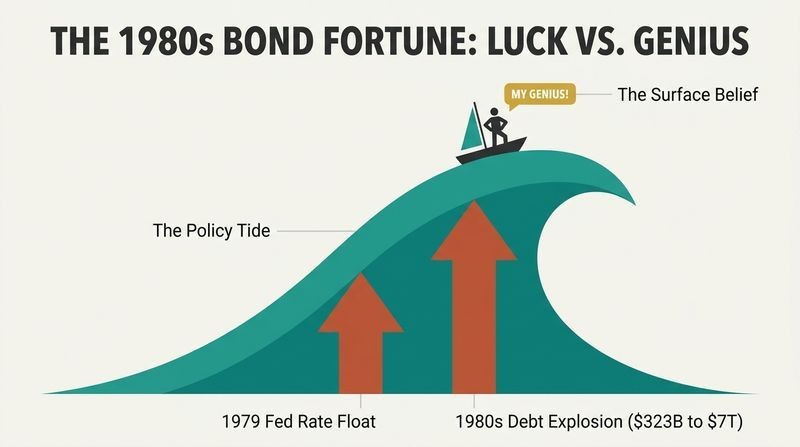

The 1980s bond fortune was policy luck dressed up as genius

Someone else stuffed the turkey. Lewis argues Salomon's traders were not suddenly more talented. Two acts of government handed them a windfall. First, in October 1979 Federal Reserve chairman Paul Volcker announced that interest rates would float freely. Because bond prices move inversely to rates, wildly swinging rates transformed bonds from sleepy savings vehicles into a casino. Turnover exploded.

Second, American governments, consumers, and corporations went on a historic borrowing binge. Combined debt rose from 323 billion dollars in 1977 to 7 trillion dollars by 1985, and far more of it took the form of tradable bonds. Salomon, already the dominant bond house, feasted first because it had the expertise in place. The men mistook a rare structural glitch for personal brilliance.

This is the book's quietly devastating thesis: enormous rewards flowed to people who happened to be sitting in the right seat when the rules changed. The insight anticipates Nassim Taleb's warning against confusing luck with skill, and Michael Mauboussin's work on separating the two. There is a sobering corollary for anyone evaluating their own success in a booming field. When an entire industry gets rich simultaneously, macro forces, not individual merit, are usually the cause. The danger is that windfall beneficiaries build identities and compensation expectations around a tailwind that can reverse without warning, as Salomon's later decline shows.

Wall Street's cardinal interview rule: never admit you want money

Lie about your motives or lose the job. Lewis's Lehman Brothers interview cratered when he honestly said he wanted to make money. The square young interviewer scolded him: they discourage people who are too interested in money. A friend later explained the taboo. When asked why you want to be an investment banker, you must invoke the challenge, the people, and the thrill of the deal, but never money.

The hypocrisy was total, since everyone knew money was the entire point. Lewis also skewers the era's ritual of studying economics not because anyone enjoyed it but because it functioned as a sifting device, a signal that you would subordinate your education to your career. Forty percent of Yale's 1986 class applied to a single investment bank.

The ritual denial of money illustrates what sociologists call institutional hypocrisy, where a group publicly professes values it privately violates to preserve legitimacy. The economics-major stampede is a textbook signaling equilibrium in the sense economist Michael Spence described: the degree conveyed conformity and willingness to sacrifice, not actual knowledge, which banks admitted was useless on the trading floor. What makes the observation sharp is Lewis's point that the credential worked precisely because it was a costly, joyless commitment device. The lesson endures: when everyone chases the same prize, the prize becomes overvalued, and the selection filters for compliance rather than talent.

In every trade someone is the fool, and the firm made you find them

Know the fool, or you are the fool. Lewis cites Warren Buffett's rule: any player unaware of the sucker in the market probably is the sucker. Salomon's edge was knowing who valued bonds wrongly. Lewis learned this brutally on his first sale, unloading Salomon's unwanted AT&T bonds onto a naive Austrian banker he calls Herman, who lost tens of thousands overnight and was eventually fired. Lewis felt not guilt but relief, discovering the middleman's protection: the customer suffers, not you.

When salesmen protested screwing clients, traders asked "Who do you work for?" President Tom Strauss offered the guiding creed: customers have short memories. Dumping a firm's loss into a client's portfolio even had a name, jamming, and it earned you praise, not punishment.

The zero-sum framing is the moral core of the book. Every dollar out of the client's pocket is a dollar in Salomon's, a fact salesmen learned to rationalize by telling themselves a bad idea for the firm was a good idea for the buyer. This is agency conflict in its rawest form, the same misalignment that decades later fueled the 2008 crisis, when banks sold securities they privately shorted. Strauss's line about short memories is empirically shaky: reputation effects in repeat markets usually punish exploitation, which is exactly why Lewis notes European clients, unlike Americans, refused to come back. Trust, once betrayed, is expensive to rebuild.

Lewie Ranieri turned home loans into bonds and built an empire the firm resented

Depersonalize the mortgage, and it becomes a tradable bond. A single home loan was too small and messy for Wall Street. Ranieri's department pooled thousands of mortgages so investors could trust statistics rather than inspect houses, then sold slices of the cash flow as bonds guaranteed by government agencies. Ranieri, a college dropout who started in the mailroom, hired from the back office, insisted "mortgages are about math," and lobbied Congress to change laws state by state.

The department nearly died until a September 1981 tax break forced thrifts to dump their loans, handing Salomon a monopoly on a trillion-dollar market. In 1982 the group made 150 million dollars. Yet Ranieri built it, in his words, in spite of the firm, which nearly shut him down.

Ranieri's story is a case study in how genuine innovation often incubates at an organization's despised margins. Securitization, transforming illiquid assets into liquid tradable instruments, was a real financial breakthrough that expanded credit for millions of homeowners. But the same mechanism that democratized mortgage funding also severed the lender's relationship to the borrower, a decoupling that would metastasize spectacularly in the subprime era two decades on. Lewis captures a recurring institutional pathology: incumbents starve their most creative units because those units threaten internal power balances. The mortgage desk survived only because one protector, Gutfreund, cast the deciding vote against its executioners.

Investors fear looking foolish alone more than they fear losing money

Contrarianism pays because conformity is a prison. Lewis's mentor Alexander taught that when everyone does the same thing, do the opposite. Investors rarely fear losing money as much as they fear the solitude of a bet others avoid, because a loss made alone has no excuse. When the U.S. Farm Credit system looked shaky, investors dumped its bonds, not because they were stupid but because they could not be seen holding them. Alexander bought, betting the government would never let it default. He was right.

His second method: after any shock, ignore the obvious target and hunt secondary effects. When Chernobyl exploded, he bought oil futures (less nuclear power means more oil demand), then potatoes (fallout would taint European crops, raising demand for American substitutes).

This is one of the most transferable ideas in the book. The observation that professionals fear career risk more than portfolio risk anticipates Keynes's famous remark that it is better for reputation to fail conventionally than to succeed unconventionally. The herd is not irrational; it is rationally protecting itself from blame, which creates exploitable mispricings for anyone insulated from that social pressure. The secondary-effects discipline resembles systems thinking: markets are webs, so a shock in one node ripples predictably to others. The caveat is survivorship bias. Lewis showcases Alexander's winning calls, but contrarian bets that arrive too early are indistinguishable from being simply wrong.

Institutions quietly reshape you into someone you once mocked

Salomonization was the hidden curriculum. The training program's real lessons were not the bond math but the war stories and the pecking order. Trainees split into a groveling front row and a paper-throwing back row. The prize everyone secretly craved was to become a "Big Swinging Dick," a trader who made millions pour out of the phones. New recruits, Lewis notes, sensed they had to shed whatever intellect and refinement they arrived with, buying the myth that a great trader is a great savage.

Lewis, who joined almost by accident after a dinner beside a managing director's wife, watched himself absorb the traits of whoever he last spoke to, mimicking his colleagues' phone posture and cursing until he stopped being a "geek" and became a normal, jaded salesman.

The account is a vivid ethnography of organizational socialization. Psychologists studying total institutions, from Erving Goffman onward, describe exactly this process: identity is stripped and rebuilt to fit the group. The back-row hooliganism is not immaturity but adaptive signaling, a performance of the aggression the culture rewarded. What gives the passage bite is Lewis's honesty that he was not corrupted against his will but drifted willingly, because status inside the tribe felt essential. The unsettling implication is that self-knowledge offers weak protection. People rarely notice their values shifting in real time. Environments, more than intentions, determine behavior, which is why choosing which institution to enter may matter more than resolving to resist it.

Milken's junk bonds exposed the efficient markets myth Salomon believed

Corporations were mispriced, and Salomon slept through it. Business schools taught that stock prices already reflect all information, so nobody can consistently win. Michael Milken at Drexel saw the flaw. He noticed that "fallen angels," the bonds of troubled companies, were shunned out of fear of seeming imprudent, not because they were genuinely bad bets. A portfolio of them consistently outperformed blue chips. He built a market that let shaky and small companies borrow directly from investors at higher rates.

Junk behaves like equity, soaring or sinking with the company's fortunes. By 1986 Drexel had passed Salomon as Wall Street's most profitable firm. Salomon dismissed junk as a fad and even sabotaged its own tiny junk desk, missing the era's biggest trade: the buying and selling of entire companies.

Milken's core insight is a direct empirical rebuttal to the strong form of the efficient market hypothesis. Markets efficiently digested earnings but grossly mispriced credit risk because rating agencies and money managers anchored to the past and hid behind a false prudence. This is the same behavioral gap Lewis identifies in bond investors generally, now applied to corporate credit. The darker legacy is well documented: junk-financed leveraged buyouts loaded firms with debt, Milken was later imprisoned for securities violations, and some deals collapsed. Salomon's failure to enter was not principled caution but managerial ignorance amid internal warfare, a reminder that firms often miss revolutions happening in the next cubicle.

Paying for loyalty after breaking the covenant never works

Short-term greed drove out long-term greed. When Salomon was a partnership, traders kept their wealth locked in the firm, so loyalty was automatic. After Gutfreund sold the firm in 1981 (personally clearing about 40 million dollars), that glue dissolved. Star mortgage traders like Howie Rubin bolted for guaranteed millions elsewhere, and each defector carried Salomon's client list and techniques, dismantling its monopoly. Management, judging producers by revenue rather than profit, rewarded reckless growth.

The covenant shattered publicly in October 1987, when the firm fired around a thousand people, dumping entire departments overnight, breaking the promise that performance would always be protected. Then, in its worst year, it broke its own pay ceilings to bribe survivors to stay. As one departing trader put it, if you want loyalty, hire a cocker spaniel.

The compensation saga is a clinic in incentive design gone wrong. Rewarding gross revenue rather than net profit encouraged empire-building and risk-taking whose costs were invisible until markets turned, an error that recurs across finance whenever bonuses track volume over value. Once the partnership's deferred-equity lock disappeared, Salomon faced a classic principal-agent problem with no retention mechanism except cash, which is the weakest possible bond because it can always be outbid. The deeper lesson, echoed in modern organizational research, is that loyalty is reciprocal. An institution that treats people as disposable trading positions cannot later purchase the devotion it discarded. Culture, once broken, is not repriced.

Analysis

Liar's Poker endures because it is simultaneously a coming-of-age memoir, an ethnography, and a piece of investigative economics. Written in 1989, it captured a hinge moment: the transformation of bonds from a somnolent backwater into the engine of Wall Street wealth, and with it the rise of a trading culture whose values, or absence of them, would define finance for a generation. Lewis's central and still radical claim is that the fortunes were largely undeserved, a byproduct of Volcker's monetary revolution and America's leveraging, not of superior intelligence. He indicts himself as thoroughly as his colleagues, which lends the moral critique credibility that outside muckraking lacks.

The book's analytical spine is the recognition that Wall Street profits often flow from opacity and information asymmetry rather than value creation. The hidden bond spread, the search for the fool, the practice of jamming losses into clients, all describe rent extraction. Yet Lewis is too honest to make finance purely parasitic. Ranieri's securitization and Milken's junk bonds were genuine innovations that expanded credit, even as both seeded future catastrophes. This tension, between finance as useful intermediary and finance as predatory casino, remains unresolved and is precisely what makes the book prophetic. The 2008 crisis reads like Liar's Poker's mortgage desk scaled to civilizational size.

What dates least well is nothing, and what dates most is the casual brutality toward women and the ethnic caricature, which Lewis reports rather than endorses but seldom interrogates. As business writing, its enduring gift is the demonstration that culture and incentives, not spreadsheets, explain institutional behavior. Salomon fell not to competitors but to its own severed covenant, its confusion of revenue with profit, and its leaders' mistaking of a policy windfall for personal greatness. The warning generalizes: beware any success you cannot fully explain.

Review Summary

Liar's Poker offers an insider's view of Wall Street's cutthroat culture in the 1980s. Lewis's witty and sarcastic narrative exposes the greed, ruthlessness, and absurdity of investment banking. While some readers found it entertaining and insightful, others felt it was dated or self-indulgent. The book provides a glimpse into the origins of mortgage-backed securities and the mindset that led to later financial crises. Despite its flaws, many consider it a must-read for understanding the financial world's inner workings.

People Also Read

FAQ

What's Liar's Poker about?

- Wall Street Insights: Liar's Poker by Michael Lewis is a memoir that offers an insider's perspective on the bond trading culture at Salomon Brothers during the 1980s. It delves into the aggressive trading environment and the immense profits that characterized the era.

- Personal Journey: The book chronicles Lewis's experiences as a bond salesman, highlighting his transition from a naive trainee to a successful trader. It reflects on the rapid wealth accumulation and moral ambiguities faced by traders.

- Cultural Commentary: Lewis critiques the broader financial system, emphasizing the disconnect between Wall Street's practices and the realities of the average American. The book serves as both a cautionary tale and a celebration of financial excesses.

Why should I read Liar's Poker?

- Engaging Narrative: Michael Lewis's storytelling is both entertaining and informative, making complex financial concepts accessible to readers. His vivid descriptions bring the trading floor to life.

- Historical Context: The book provides valuable insights into the financial practices of the 1980s, a pivotal time in Wall Street history. Understanding this context helps readers grasp the evolution of modern finance.

- Lessons on Ethics: It encourages reflection on ethical considerations in business, highlighting the consequences of unchecked ambition and the nature of risk-taking in finance.

What are the key takeaways of Liar's Poker?

- Culture of Excess: The book illustrates how the culture at Salomon Brothers fostered a sense of invincibility among traders, leading to reckless behavior and contributing to financial crises.

- Importance of Relationships: Personal connections in finance are crucial, where loyalty and trust often outweigh formal qualifications. Success often hinges on these relationships.

- Understanding Market Dynamics: Lewis explains how traders manipulate market perceptions and the importance of understanding human behavior in trading, essential for anyone interested in finance.

What are the best quotes from Liar's Poker and what do they mean?

- "One hand, one million dollars, no tears.": This quote encapsulates the high-stakes nature of trading at Salomon Brothers, where losses were expected but not lamented, reflecting the brutal reality of the trading floor.

- "Wall Street is a street with a river at one end and a graveyard at the other.": This metaphor highlights the duality of Wall Street, where immense wealth is created alongside significant risks and losses.

- "In the land of the blind, the one-eyed man is king.": This quote speaks to the advantage of having even a slight edge in knowledge or skill in a competitive environment, underscoring the importance of being informed.

How does Liar's Poker critique Wall Street culture?

- Moral Ambiguity: Lewis critiques the ethical lapses prevalent in the finance industry, where profit often takes precedence over integrity, highlighting the consequences of this mindset.

- Excess and Greed: The book exposes the culture of excess and greed that characterized Wall Street during the 1980s, illustrating how this environment led to reckless behavior.

- Disconnect from Reality: Lewis points out the disconnect between Wall Street's practices and the lives of ordinary Americans, emphasizing the need for accountability in the financial sector.

What is the significance of Liar's Poker in the book?

- Game as Metaphor: Liar's Poker serves as a metaphor for the bond trading environment, where bluffing and deception are key components, reflecting the psychological aspects of trading.

- Cultural Ritual: The game was a popular pastime among traders, fostering camaraderie and competition, illustrating the informal culture of Salomon Brothers.

- Risk Assessment: Playing Liar's Poker requires assessing risk and making calculated bets, paralleling the decision-making processes in trading, highlighting strategic thinking.

What role does money play in Liar's Poker?

- Driving Force: Money is portrayed as a primary motivator for traders, influencing their decisions and behaviors, driving the competitive atmosphere on the trading floor.

- Symbol of Success: Wealth accumulation is equated with success and status within the firm, reinforcing the idea that money defines worth.

- Consequences of Wealth: Lewis explores the pressures and ethical dilemmas that arise from wealth, serving as a cautionary tale about prioritizing money over values.

How does Liar's Poker reflect Michael Lewis's personal journey?

- Career Development: Lewis's transition from a bond salesman to a successful author mirrors the journey of many traders seeking to define their identities beyond financial success.

- Self-Reflection: The book serves as a form of self-reflection for Lewis, as he grapples with the moral implications of his work in finance.

- Cultural Critique: Through his personal narrative, Lewis critiques the broader culture of Wall Street, highlighting the need for change and understanding the complexities of the financial world.

What is the significance of the mortgage department in Liar's Poker?

- Profitability: The mortgage department at Salomon Brothers was highly profitable, contributing significantly to the firm's success, transforming the bond market with mortgage-backed securities.

- Cultural Impact: The department's culture, characterized by camaraderie, contrasts with the cutthroat environments of other divisions, central to understanding internal conflicts.

- Talent Drain: The exodus of top mortgage traders to competitors highlights Salomon Brothers' vulnerabilities, illustrating how the firm's compensation structure failed to retain talent.

How does Liar's Poker address the concept of corporate raiding?

- Emergence of Junk Bonds: Junk bonds became a tool for corporate raiders to finance takeovers, reshaping the corporate landscape with high levels of debt.

- Milken's Influence: Michael Milken's role in popularizing junk bonds is portrayed as revolutionary, changing how companies accessed capital.

- Consequences of Raiding: Lewis critiques the impact of corporate raiding on companies and employees, emphasizing the ethical implications of prioritizing short-term profits.

What role does luck play in Liar's Poker?

- Unpredictable Outcomes: Luck significantly influences success in finance, often overshadowing skill and preparation, highlighted through anecdotes of market movements.

- Personal Experiences: Lewis reflects on his career, acknowledging moments where luck played a crucial role, reminding that success is not solely a product of hard work.

- Market Dynamics: The unpredictable nature of financial markets means even knowledgeable traders face unexpected challenges, emphasizing adaptability.

What lessons can be learned from Liar's Poker?

- Navigating Corporate Culture: Insights into the complexities of corporate culture on Wall Street emphasize understanding power dynamics and relationships.

- Understanding Risk and Reward: Readers learn about risk management intricacies, assessing opportunities, and making informed decisions through Lewis's anecdotes.

- The Value of Adaptability: The need for adaptability in changing market conditions is underscored, illustrating how openness to new ideas can lead to success.

About the Author

Other books by Michael Lewis

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.