Key Takeaways

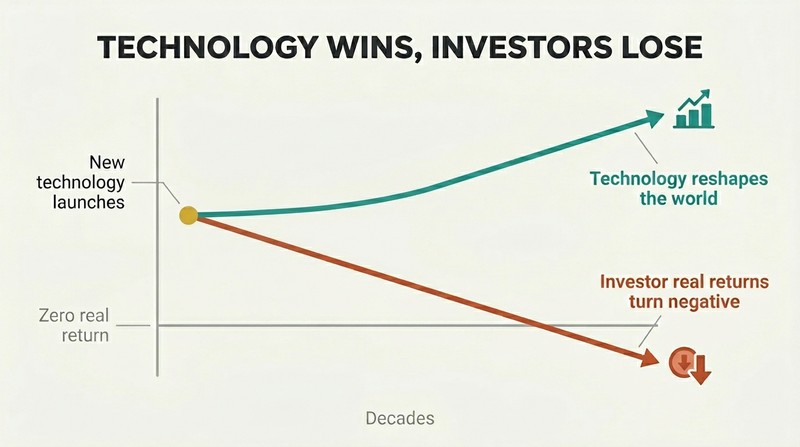

Technology always wins, but its investors usually lose

The central paradox of technology investing. Alasdair Nairn, a professional investor who ran global equity research at Templeton during the dot-com mania, studied ten transformative technologies from railways to the Internet. His verdict: a technology can reshape civilization while bankrupting nearly everyone who funded it. British railways genuinely revolutionized 19th-century transport, yet anyone who invested at the 1840s peak earned negative real returns over the next fifty years.

Why the gap exists. New technologies attract floods of capital, spawn hundreds of competitors, and get bid to valuations that discount all of tomorrow's profits today. The infrastructure gets built, consumers benefit, promoters cash out — but the average shareholder funds duplication, fraud, and ruinous price wars. Picking the winning technology is the easy part; profiting from it is the hard part.

This inverts the intuition most investors bring to innovation. The error is conflating economic importance with investment merit—a distinction echoed in Warren Buffett's observation that the airplane and the automobile transformed the world while wiping out most of their manufacturers' shareholders. Nairn's edge is empirical: he reconstructed actual share-price and earnings data from archives reaching the ceiling of a storage room. The framework also anticipates Carlota Perez's work on technological revolutions and financial bubbles, lending academic weight to what could otherwise read as mere contrarian skepticism.

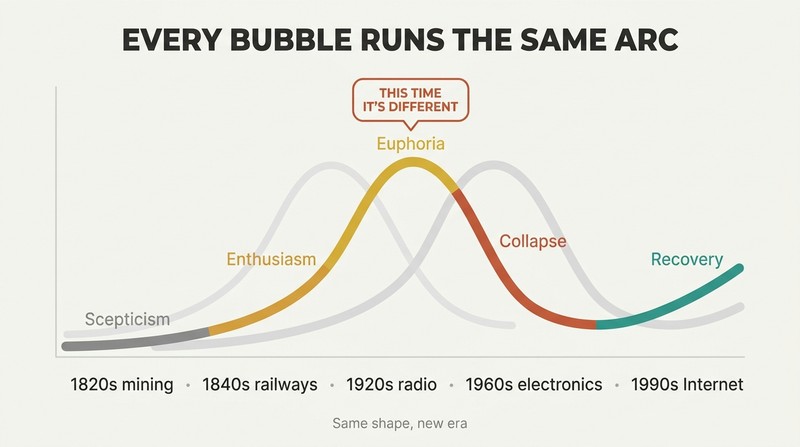

"This time it's different" are the four most expensive words in investing

History rhymes; bubbles repeat. Nairn borrows Sir John Templeton's warning as the book's spine. Every technology mania — the 1820s mining stocks, 1840s railways, 1920s radio, 1960s electronics, 1990s Internet — followed a near-identical emotional arc: scepticism, then enthusiasm, then euphoria, then collapse, then sober recovery. The specifics change; human nature does not.

The recurring ingredients. A bubble needs more than a shiny new technology. It requires:

1. A genuinely transformative invention enabling extravagant claims

2. Cheap money and easy credit

3. General consumer and investor optimism

4. A wave of promotional trade publications

5. An efficient machine for manufacturing new companies

6. Suspension of normal valuation criteria

When Nairn heard analysts in 1999 insist the "new economy" made old rules obsolete, he recognized the same refrain that preceded every prior crash.

The claim is strengthened by Nairn's structural insight that bubbles are timed by monetary conditions, not by the technology's maturity. This aligns with Hyman Minsky's financial-instability hypothesis: stability breeds risk-taking that breeds instability. One nuance worth flagging—the phrase can become a lazy thought-terminator. Sometimes things genuinely are different; the printing press, electricity, and the Internet did permanently raise productivity. The discipline Templeton urged was not blanket cynicism but insistence that prices eventually anchor to earnings, however delayed the reckoning.

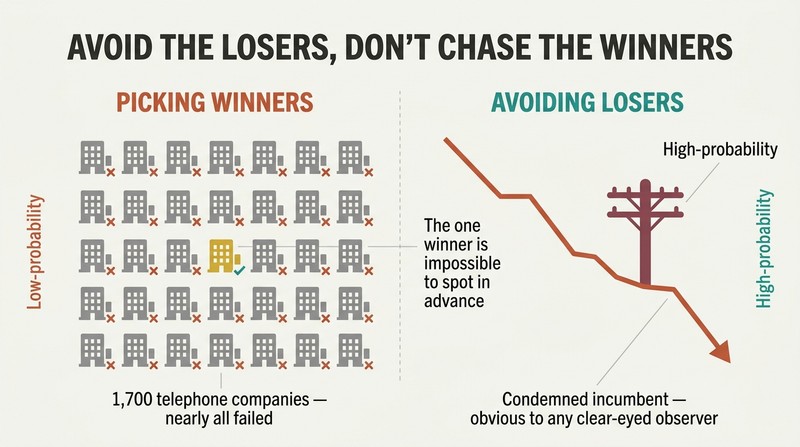

Spotting the losers is easier and safer than picking the winners

The book's most actionable lesson. Identifying which old technology is doomed is far simpler than guessing which new company triumphs. By the 1830s, any clear-eyed observer could see British canals could never match railways' cost and capacity — their share prices entered permanent decline. Western Union dismissed the telephone as an "electrical toy" and was rendered a niche player within twenty years.

Why this matters for portfolios. Trying to pick winners among hundreds of new entrants is a low-probability lottery; over 1,000 automobile makers and 1,700 telephone companies were launched, and almost all failed. But avoiding the condemned incumbents — canals, telegraphs, gas lighting, horse-drawn transport, newsprint — is high-probability. Kodak vanished once digital photography arrived. For professional investors, sidestepping structural losers reliably preserves wealth, even when the winners remain impossible to identify in advance.

This is the book's sharpest practical contribution, and it resonates with Charlie Munger's dictum to "invert, always invert." Psychologically, loss-avoidance is underrated because it lacks the glamour of finding the next Amazon. Yet the asymmetry is real: a doomed incumbent's decline is often visible years ahead, while winners emerge from chaotic selection. A caveat—incumbents occasionally adapt (Studebaker bridged carriages to cars; the best retailers absorbed e-commerce), so "loser" status requires confirming the incumbent cannot shift its cost curve, not merely that it faces a threat.

Without monopoly protection, competition strips all returns away

The single greatest determinant of profit. Nairn argues the only reliable way to earn sustained excess returns from a new technology is some barrier to entry: patent, copyright, legal prohibition, or a structurally superior cost curve. Where capital flows freely and no barrier exists, competition forces returns down across an entire sector — even when the technology succeeds spectacularly.

The contrast in cases. Standard Oil earned 10 – 20% returns on capital for decades because it controlled distribution. AT&T's profits stayed lavish only while Bell's patents held; once they expired and competitors flooded in, margins and earnings per share fell despite booming demand. Microsoft and Intel later captured nearly all PC-industry profit because they owned the branded "equalisers" — Windows and the microprocessor — while PC assembly itself became a brutal commodity business with wafer-thin margins.

This is essentially the economic theory of rents applied across two centuries, and it prefigures Buffett's "economic moat" concept and Michael Porter's five forces. The deeper insight is that durable moats are rare and perishable—AT&T's patent moat had a fixed expiry; Standard Oil's distribution moat was dismantled by antitrust. The modern parallel is acute: Google and Facebook now enjoy near-monopoly rents in search and social advertising, which by Nairn's logic makes regulatory backlash not a tail risk but a near-certainty, exactly as it was for Standard Oil.

Inventors rarely grasp what their own breakthroughs are really for

Visionaries are unreliable forecasters. The people who create new technologies frequently misjudge their ultimate use. Marconi, Fessenden, and de Forest all built wireless to replace point-to-point telegraphy; almost none foresaw broadcasting, which became radio's explosive market. AT&T treated radio broadcasting as a frivolous hobby. Western Union's committee concluded the telephone could never be more than a curiosity.

The compounding error. Even when inventors grasp the significance, financial pressure often forces them to sell rights cheaply. Bell offered his patents to Western Union for $100,000 and was lucky to be refused. The big computer firms — IBM, DEC — left the personal computer to hobbyists because they couldn't see the market. Ken Olsen of DEC declared in 1977 there was no reason for anyone to have a computer at home. The future is consistently misread by those closest to it.

This challenges the cult of the founder-visionary that dominates modern tech narratives. The pattern reflects what Clayton Christensen later formalized as the innovator's dilemma: incumbents and even inventors optimize for the known market and miss the disruptive adjacency. There's a sociological dimension too—expertise creates tunnel vision. The corrective for investors is to weight observed adoption patterns over expert pronouncements about use cases. Email, not commerce, became the Internet's first killer app; broadcasting, not telegraphy, made radio. Watch what users actually do, not what creators predict.

Every technology swings from capital famine to capital glut and back

Buy in the famine, not the feast. Nairn maps a recurring five-stage cycle: concept and feasibility, prototype development, funding and commercial viability, rationalisation and refinancing, then ultimate success or failure. The pioneers face repeated cash crunches; survival depends as much on retaining investor confidence as on the technology itself. Time is the enemy — when confidence wanes, raising cash becomes impossible.

The investor's window. The best moment to invest is after a capital drought has culled the field, survivors have been refinanced, and the losers have gone bankrupt — not when demand peaks and prices are absurd. General Motors had to be rescued from bankruptcy twice; Ford succeeded only on Henry Ford's third attempt. Amazon and Google survived precisely because they had raised enough capital to weather the post-2000 drought when rivals starved.

The cyclicality framing is valuable because it reframes recessions as filtration mechanisms rather than mere disasters. This dovetails with venture-capital vintage-year analysis, which shows funds launched in downturns often outperform—capital is cheap, competition thin, and only resilient businesses survive. The deeper point about confidence is almost reflexive: a technology firm's solvency is partly a function of perceived solvency, a self-fulfilling dynamic resembling a bank run. The actionable discipline—wait for the shake-out—runs directly against the herd impulse that creates bubbles in the first place.

When analysts climb the income statement, sell

Valuation drift signals a bubble's late stage. Nairn observed a telltale pattern: as prices detach from reality, analysts abandon dividends, then earnings, then move to revenue, then to non-financial metrics like website "eyeballs," visits, and "stickiness." During the dot-com peak, valuations were justified by discounting cash flows fifteen years out for companies with no profits. Yahoo commanded a $100bn-plus market cap on under $1bn of sales.

The cash-flow reckoning is unavoidable. Echoing journalist Frank Fayant's 1907 exposé of radio-stock scams, Nairn insists there is no escape from "the scissor blades of cash flow." A company that survives only by issuing new stock, never paying a dividend, enriches mainly its promoters. When share buybacks and equity-based pay let firms dodge the discipline of returning cash, investors should treat the absence of dividend-paying capacity as a red flag, not a footnote.

This is a precise, falsifiable bubble indicator, more useful than vague warnings about "froth." The migration up the income statement is a measurable behavioral tell, comparable to credit analysts loosening covenants near a cycle peak. Fayant's century-old radio exposé reading identically to 1999 dot-com prospectuses is the book's most chilling evidence for the permanence of human folly. One extension: stock-based compensation remains a live concern today, as it obscures true profitability and dilutes shareholders—the same mechanism Nairn flags, now industrial-scale across modern tech.

Hardware champions almost never survive the shift to software

Culture, not capability, kills incumbents. When an industry's value migrates from physical engineering to software and user interface, the dominant hardware firm typically collapses — not from lack of resources but from cultural and architectural handicaps. Nokia commanded roughly 40% of mobile handsets, staffed by brilliant engineers, yet when the user interface became decisive, Apple's iPhone ecosystem destroyed it; Nokia ended as a Microsoft footnote.

The pattern repeats across eras. IBM, dominant in mainframes, was caught flat-footed by the minicomputer and again by the PC. Kodak owned photography until digital arrived. The rule-bound, hardware-engineering mindset cannot easily encompass the anarchic, fast-iterating culture of software developers, and legacy systems become liabilities rather than assets. Even Intel and Microsoft, the PC era's twin monopolists, both lost mobile leadership to ARM and Google's Android.

This sharpens the disruption thesis by locating the failure mechanism in organizational culture and architecture rather than strategy alone—an insight aligned with Rebecca Henderson's research on architectural innovation, where incumbents fail because their structures mirror the old product. The investing implication is concrete: be wary of hardware leaders facing software-defined competition, regardless of balance-sheet strength. The current frontier test is whether today's software and platform giants can navigate the next architectural shift—AI-native interfaces—or whether they too will be handicapped by the very assets that made them dominant.

The losers from technology are easy targets for fraud and manipulation

Euphoria is a con artist's paradise. When investors suspend rational valuation, manipulators inevitably appear. Nairn catalogues the recurring schemes: George Hudson, Britain's 1840s "Railway King," paid dividends out of capital while charging revenue items against the balance sheet to inflate profits. Jay Gould and his cohorts "watered" Erie Railroad stock — issuing shares whose proceeds were siphoned off, leaving an empty shell. E. J. Pennington raised vast sums on automobile "patents" that were sometimes mere tracings of others' work.

The defense is cash-flow analysis. Profit can be misrepresented; cash balances and cash flows are far harder to fake. The York and North Midland Railway funded dividends entirely through new equity issuance for a decade until the arithmetic collapsed. The timeless rule Nairn extracts: when in doubt, check the cash position, because reported earnings during a mania are frequently fiction.

The continuity here is the book's quietly devastating argument—Enron, Wirecard, and assorted crypto collapses are lineal descendants of Hudson and Gould. The structural enabler is always the same: weak legal frameworks, dispersed and passive owners, and investor greed that suspends scrutiny. Nairn's emphasis on cash over earnings echoes forensic-accounting practice and the work of analysts like Howard Schilit. The sobering implication is that regulation reduces but never eliminates fraud, because each new technology creates a fresh information asymmetry that the unscrupulous exploit before rules catch up.

First-mover advantage is mostly a mirage without barriers to defend it

Being first rarely means staying first. Netscape built the dominant browser, IPO'd spectacularly in 1995, then squandered its lead by openly antagonizing Microsoft instead of entrenching its position — and was effectively destroyed within three years. The early British railways enjoyed first-mover advantage but lost it when freely available capital funded competing lines that forced returns down for everyone.

Last man standing beats first to arrive. When dot-com funding dried up after 2000, what mattered was not first-entrant status but who had raised enough capital to survive. MITS pioneered the personal computer with the Altair but vanished; Apple and IBM, arriving later, defined the market. Yahoo led search but, fixated elsewhere, was leapfrogged by Google, which obsessed single-mindedly over building the fastest, most accurate engine. The durable winner is usually the disciplined executor, not the pioneer.

This punctures one of Silicon Valley's most cherished myths. Academic work by Tellis and Golder found that market pioneers fail far more often than popular history suggests, with later "fast followers" frequently dominating—precisely Nairn's claim. The mechanism is that pioneers bear the cost of educating the market and proving the technology, while followers learn from their mistakes and arrive with better products and capital. The strategic lesson for founders and investors alike: a head start is an asset only if converted quickly into a defensible moat before well-funded rivals react.

Governments, not markets, often fund the riskiest foundational research

The Internet was a child of the Cold War. Unlike the telephone or electric light, the Internet's basic research and physical infrastructure were largely paid for by the US government — chiefly the Department of Defense through ARPA — over decades. Where Babbage and Marconi had to court the military for scraps, networking emerged because the government wanted nuclear-survivable, decentralized communications and economical timeshare access to scarce mainframes.

Why this changed the commercial dynamic. Because the costly, unprofitable groundwork was already complete, early Internet companies like Cisco, Netscape, and Yahoo could skip straight to commercialisation with relatively little capital. Vannevar Bush's 1945 vision of the "memex" — information stored by association rather than hierarchy, mirroring human thought — took fifty years and decentralized, publicly funded development to materialise as the World Wide Web. The private sector reaped what public money had sown.

This is an important corrective to techno-libertarian origin myths, echoing economist Mariana Mazzucato's argument in The Entrepreneurial State that the riskiest innovations—touchscreens, GPS, the Internet itself—were de-risked by public funding before private firms captured the upside. The tension Nairn surfaces is distributional: taxpayers bore the research risk while a handful of founders and early investors captured extraordinary returns. It also explains why the Internet, unlike railways, produced little speculative overcapacity in its core—though the adjacent telecoms sector, privately funded, repeated the classic overbuild-and-bust pattern with $243bn of capex in 2000 alone.

Watch finance next: money is the largest digital product of all

The coming disruption is in banking. Nairn argues that having transformed advertising, retail, and media, the Internet's most profound future impact lies in financial services — a vast, cost-heavy, trust-dependent sector burdened by legacy systems. Money is the economy's largest digital product, so the scope for efficiency gains is enormous. Payment firms, peer-to-peer lenders, and blockchain technology are early skirmishers in a longer campaign.

Why the moat is cracking. Banks' traditional barrier to entry — a physical branch network to gather deposits — has become a liability in a mobile world. The 2007 – 08 crisis also shattered the other great barrier: customer trust. Nairn predicts incumbents will be picked off service by service, with the highest-margin offerings (like the ~10% spread on tourist foreign exchange) attacked first. He notes bitcoin's rise reflects damaged faith in conventional banking, while cautioning it bears all the hallmarks of historic precious-metal manias.

Writing in 2018, Nairn's forecast has aged with mixed results—fintechs like Wrise, Revolut, and Stripe compressed FX spreads and payments margins as predicted, yet incumbent banks proved more resilient than the thesis implied, shielded by regulation and inertia. His framing of branch networks as liabilities-turned-assets is the same logic that doomed Kodak's film infrastructure. The bitcoin observation—dismissing the currency speculation while respecting the underlying distributed-ledger technology—displays exactly the discriminating skepticism the whole book advocates: separate the durable technological shift from the financial mania riding on top of it.

Analysis

Engines That Move Markets is a work of financial history disguised as an investment manual, and its method is its message. Alasdair Nairn — a Templeton-trained value investor who began the research while watching the dot-com bubble inflate around him in 1999 — did something most pundits never bother with: he reconstructed actual share prices, earnings, and returns from primary archives spanning two centuries. The result is empirical rather than anecdotal, which gives his contrarian conclusions unusual force.

The book's intellectual architecture rests on a single, uncomfortable separation: between technological significance and investment return. These two things, which intuition fuses, are in fact loosely coupled and often inversely related. Railways, telephones, automobiles, and the Internet all genuinely remade civilization; in aggregate they generated dismal or negative returns for the investors who funded them at peak enthusiasm. The value was real but captured elsewhere — by consumers via lower prices, by insiders via stock manipulation and timely exits, and by a handful of monopolists who built defensible moats.

Nairn's five-stage technology cycle and his bubble-ingredients checklist are useful scaffolding, but the book's most transferable insights are heuristic: avoid the doomed incumbents (easier than picking winners), demand monopoly protection before expecting durable profits, distrust valuation metrics that migrate up the income statement, and buy in the capital-famine after a shake-out rather than the capital-glut of a mania.

The work's limitation is survivorship and selection bias in reverse — by choosing ten canonical technologies, Nairn studies revolutions that succeeded, which may overstate how cleanly the cycle repeats. And his finance-disruption forecast has proven slower than predicted. Yet the core discipline — anchor valuations to eventual cash flow, treat "this time it's different" as a warning siren, and respect that human nature, unlike technology, never upgrades — remains as relevant in the age of AI and crypto as it was for canal shares in 1825. The engines change; the passengers behave identically.

Review Summary

Engines That Move Markets receives mixed reviews, with an average rating of 4.37/5. Readers appreciate its comprehensive historical analysis of technological innovations and market impacts. Some find it insightful for understanding investment cycles and technological disruptions. Critics note the book's verbosity and redundancy, suggesting it could be more concise. The detailed research and unique data on equity returns are praised, while the structure and academic tone are criticized. Overall, readers value its historical perspective on technology-driven markets, despite some finding it dry or overly detailed.

Glossary

This time it's different

The most dangerous investing phraseSir John Templeton's warning, adopted as the book's organizing principle, that the four most expensive words in investing are the belief that current conditions have escaped historical patterns. Every technology bubble is justified by claims that traditional valuation rules no longer apply; every time, prices eventually re-anchor to earnings and the believers suffer losses.

The technology cycle (five stages)

Recurring path of every new technologyNairn's framework describing how technologies progress: (1) concept and feasibility, (2) feasibility to prototype, (3) funding and commercial viability, (4) rationalisation and refinancing, and (5) ultimate success or failure. Each transition demands fresh capital, creating crisis points where survival depends on retaining investor confidence as much as on the technology working.

Spotting losers vs. winners

Avoiding doomed incumbents beats stock-pickingNairn's core practical doctrine that identifying which old technology will be superseded (canals by railways, telegraph by telephone, film by digital) is reliable and high-probability, whereas selecting which new company will triumph among hundreds of competitors is a low-probability lottery. Investors preserve wealth more dependably by avoiding structural losers than by chasing winners.

The scissor blades of cash flow

Profits cannot be faked indefinitelyA metaphor, drawn from journalist Frank Fayant's 1907 critique of radio-stock promotions, for the inescapable squeeze a company faces when it cannot generate genuine cash. Firms surviving only on repeated new share issuance, never paying dividends, enrich mainly their promoters. Cash flow, unlike reported profit, is hard to manipulate and reveals true financial health.

Memex

Vannevar Bush's associative information machineA hypothetical device described by Vannevar Bush in 1945 that would store information by association—mimicking how the human mind links thoughts—rather than by rigid hierarchical indexing. The concept anticipated hypertext and the World Wide Web by roughly half a century and inspired later pioneers like Doug Engelbart and Ted Nelson.

Watering down (stock watering)

Diluting shareholders by issuing stockA 19th-century manipulation, practiced notoriously by Jay Gould and Cornelius Vanderbilt, of issuing new shares whose proceeds were siphoned off to insiders rather than invested in the business, leaving existing shareholders diluted and the company an empty shell. A recurring mechanism of fraud during periods when investors suspended rational scrutiny.

FAQ

1. What is Engines That Move Markets by Alasdair Nairn about?

- Comprehensive technology history: The book traces the evolution of technology investing from the railroads to the Internet and beyond, highlighting how technological advances have shaped markets and industries over centuries.

- Case studies and analysis: It provides detailed case studies of key technologies and companies, examining their impact on financial markets, investor behavior, and economic development.

- Investment lessons: The book explores the interplay between technological innovation, market forces, and regulatory responses, offering insights into how investors can identify winners and avoid losers in technology cycles.

2. Why should I read Engines That Move Markets by Alasdair Nairn?

- Long-term perspective: The book offers a rare, historical view of technological revolutions and their impact on markets, helping readers recognize patterns that repeat across different eras.

- Practical investment insights: It provides detailed examples of both successes and failures, equipping readers with practical knowledge about the risks and rewards of technology investing.

- Preparation for future trends: By analyzing past and present technology cycles, the book helps readers anticipate and capitalize on future technological shifts.

3. What are the key takeaways from Engines That Move Markets by Alasdair Nairn?

- Recurring bubble patterns: New technologies often trigger cycles of skepticism, enthusiasm, speculative bubbles, and eventual crashes, with only a few strong survivors remaining.

- Investor psychology is constant: Despite changing technologies, human emotions like optimism, greed, and fear consistently drive market cycles.

- Technology success ≠ investor success: Even when a technology succeeds, investors can lose money due to overvaluation and speculative excess; identifying losers early is often more profitable than chasing winners.

4. What is Alasdair Nairn’s five-stage technology investment cycle in Engines That Move Markets?

- Concept and feasibility: The cycle begins with the demonstration of a new technology’s feasibility, often requiring limited capital but high technical risk.

- Prototype to commercial viability: Moving from prototype to commercial product demands increasing funding and investor confidence, with many companies failing at this stage.

- Rationalization and consolidation: As the market matures, industry consolidation occurs, with only a few companies surviving and thriving while others fail or are acquired.

- Ultimate success and failure: The final stage sees the emergence of dominant players and the exit of unsuccessful ventures, shaping the long-term industry landscape.

- Investment timing: Understanding these stages helps investors better time their entry and exit points in technology markets.

5. How does Engines That Move Markets by Alasdair Nairn explain the impact of major historical technologies like railroads, telegraph, and electric light on markets and investors?

- Railroad mania: The railway boom transformed transport and economic development but also led to speculative excess, overbuilding, and financial crashes, with many investors losing money.

- Telegraph and telephone: These industries were shaped by intense patent battles, monopolistic strategies, and regulatory challenges, illustrating the importance of legal protection and capital.

- Electric light industry: The transition from gas to electric lighting involved technological hurdles, speculative bubbles, and eventual consolidation, with Edison’s innovations leading to the formation of General Electric.

6. What investment lessons does Alasdair Nairn highlight from the rise and fall of early technology companies in Engines That Move Markets?

- Spotting losers is easier: Identifying companies and technologies likely to fail is often more straightforward than picking winners, helping investors avoid major losses.

- Monopoly protection is key: Sustainable profits come from strong barriers to entry, such as patents or dominant platforms; without these, competition quickly erodes returns.

- Beware of hype and bubbles: Investors should be cautious during periods of speculative excess and focus on fundamentals like cash flow and balance sheets.

7. How does Engines That Move Markets by Alasdair Nairn describe the evolution and lessons of the Internet era?

- Origins and commercialization: The Internet began as a government-funded project (ARPANET) and evolved through key innovations like TCP/IP, email, and the World Wide Web before being privatized and commercialized in the 1990s.

- The Internet bubble: The late 1990s saw speculative excess, with companies valued on hype rather than profits, leading to a dramatic market crash around 2000.

- Long-term survivors: Despite the crash, companies like Google, Amazon, and Facebook emerged as dominant players, demonstrating the Internet’s lasting impact and the importance of sustainable business models.

8. What role do patents, legal battles, and regulation play in technology investing according to Engines That Move Markets by Alasdair Nairn?

- Patents as barriers: Patent protection is critical for early market dominance, as seen with Bell in telephony and Edison in electric lighting.

- Legal battles shape markets: Intense litigation can consume resources and delay progress but also reinforce the position of leading companies.

- Regulation and government intervention: Government actions, such as antitrust cases and industry regulation, can reshape industry structures and influence which companies succeed or fail.

9. How does Alasdair Nairn explain the importance of market perception versus reality in technology investing in Engines That Move Markets?

- Investor enthusiasm precedes viability: Markets often become excited about new technologies before they are commercially viable, leading to bubbles and busts.

- Publicity and confidence: Maintaining investor confidence through effective publicity is vital for securing funding, but hype can also lead to overvaluation.

- Reality sets in: Ultimately, commercial success depends on fundamentals, and companies that cannot deliver sustainable profits are likely to fail.

10. What are the main factors behind the success of major technology companies like Google, Amazon, and Facebook according to Engines That Move Markets by Alasdair Nairn?

- Innovative business models: Google’s search and advertising, Amazon’s logistics and cloud services, and Facebook’s social networking and data monetization set them apart.

- Scale and platform dominance: These companies built platforms and ecosystems that created high barriers to entry and network effects, securing long-term market leadership.

- Adaptation and acquisition: Strategic acquisitions (e.g., Facebook’s purchase of Instagram and WhatsApp) and continuous innovation helped maintain their dominance in rapidly evolving markets.

11. What does Alasdair Nairn predict about the future of technology and investing in Engines That Move Markets?

- Financial sector disruption: Digital technologies, peer-to-peer lending, and blockchain are set to disrupt traditional banking and finance, creating opportunities for new entrants.

- Rise of platforms and ecosystems: Value is shifting from hardware to software and platforms, with success depending on building ecosystems that others rely on.

- Data and AI transformation: Big data and artificial intelligence will revolutionize industries like law, medicine, and finance, offering new investment opportunities and challenges.

12. What are the best quotes from Engines That Move Markets by Alasdair Nairn and what do they mean?

- Short-term vs. long-term impact: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” (Roy Amara) – Investors often expect immediate returns but miss the enduring impact of transformative technologies.

- Value of independent thinking: “In questions of science, the authority of a thousand is not worth the humble reasoning of a single individual.” (Galileo Galilei) – Independent analysis is crucial when evaluating new technologies.

- On underestimating the Internet: Paul Krugman’s 1998 quote about the Internet’s impact being no greater than the fax machine’s highlights how even experts can misjudge revolutionary changes.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.