Key Takeaways

Most of the world's 160 currencies trap savers in a losing game

The global money problem is staggering. In 2022, Türkiye hit 85% inflation; Argentina exceeded 100%. Egypt halved its currency twice in six years, wiping out savings overnight. Lebanon froze bank deposits so severely that citizens literally robbed banks to reclaim their own money. Even in wealthy nations, over $18 trillion in bonds offered negative yields at the peak — people paid for the privilege of lending to governments.

There are roughly 160 fiat currencies, each with a monopoly in its own jurisdiction and little acceptance outside it. The global financial order is practically a barter system. A handful of top currencies lose value slowly; most of the rest devalue sharply and often. The Federal Reserve's twelve-person committee sets monetary conditions for 330 million Americans and billions abroad.

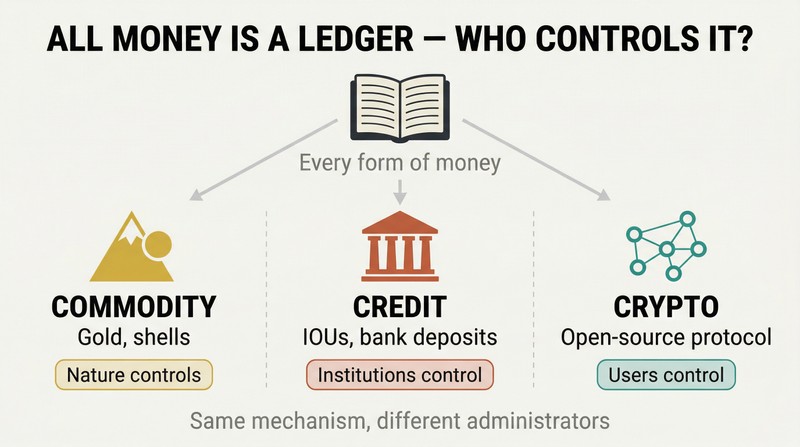

See every form of money as a ledger — then ask who controls it

Alden's unifying insight is simple. Both commodity money (gold, shells) and credit money (IOUs, bank deposits) are just different ways of maintaining a ledger. With commodity money, nature controls the ledger through the physical scarcity of the material — nobody can cheat. With credit money, human institutions control the ledger — and human institutions can and do debase it. With open-source cryptocurrency, users collectively control the ledger through code and cryptography.

This framework, which Alden calls the ledger theory of money, reconciles the long-running conflict between the commodity theory of money (Austrian school) and the credit theory (Chartalists, MMT). Both theories are partially right because both describe different methods of maintaining a ledger, with different administrators and different failure modes.

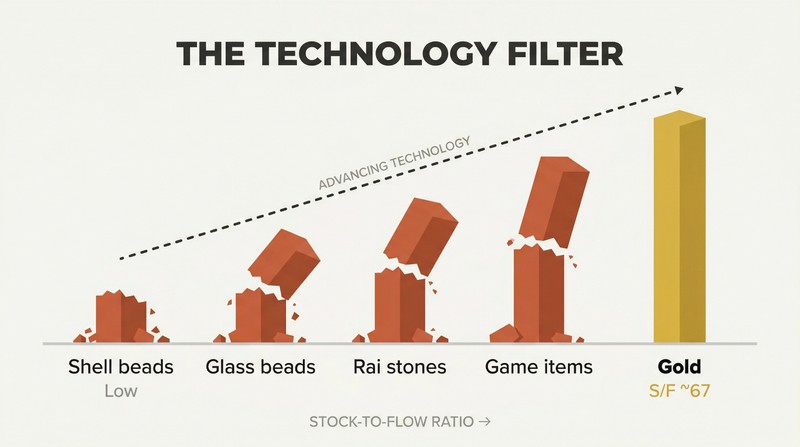

Only money that resists supply inflation survives technology's advance

Technology ruthlessly filters weak monies. The stock-to-flow ratio — existing supply divided by annual new production — determines whether a commodity can serve as money long-term. Gold's ratio is roughly 67, meaning it would take 67 years of mining to double existing supply. That's the highest of any commodity. Shell beads survived thousands of years until industrial drills made them easy to mass-produce. West African glass beads collapsed when Europeans flooded the market. On Yap island, an Irishman with modern ships broke the rai stone economy.

Even in the video game Diablo II, millions of players naturally selected Stone of Jordan rings as money — until duplication bugs destroyed their scarcity. Only gold and silver withstood millennia of technological progress.

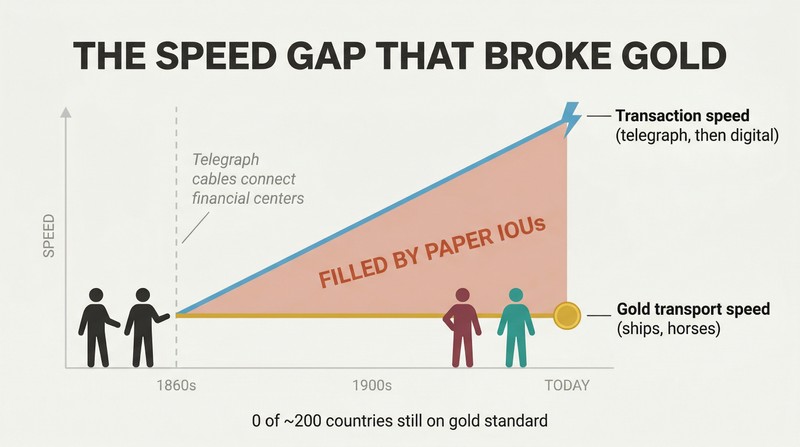

The telegraph — not politicians — broke sound money worldwide

Speed created an unbridgeable gap. When intercontinental telegraph cables connected financial centers in the 1860s, transactions began moving at the speed of light while gold still traveled at the speed of horses and ships. Banks filled that gap with IOUs, gaining a monopoly on fast long-distance payments. Claims for gold proliferated far beyond actual gold reserves. By the early 20th century, the UK banking system held just 4-7% reserves against deposits.

This wasn't a moral failing — it was technological inevitability. Out of nearly 200 countries, zero maintain a gold standard today. Switzerland was last, dropping it in 1999. If we reran this period of history a hundred times, Alden argues, we'd end up in the same place nearly every time. Once telecommunication systems existed, centralized ledgers dominated.

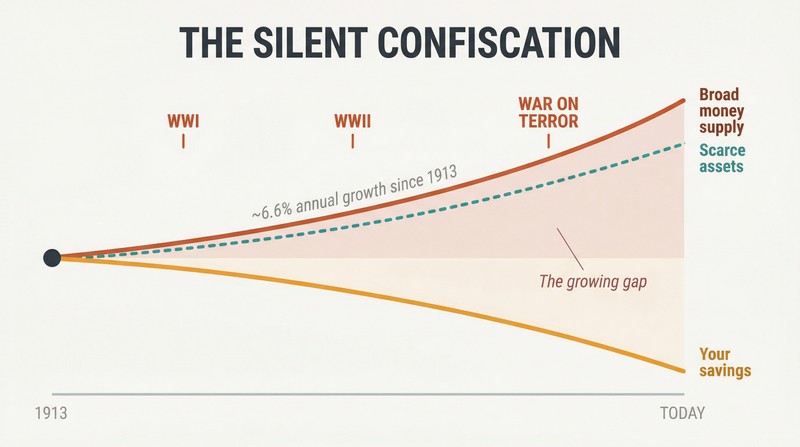

Governments fund wars and bailouts by silently debasing your savings

The UK's WWI financing was a cover-up. The 1914 War Loan was marketed as massively oversubscribed; a century later, Bank of England archives revealed it raised less than a third of its target. The Bank secretly created money to buy the rest, then lied. The Financial Times issued a correction 103 years late. Prices and the broad money supply more than doubled within five years, silently confiscating savers' purchasing power.

The pattern repeats. The US War on Terror cost an estimated $5.8 trillion by 2022, financed entirely through debt rather than transparent taxation — unprecedented in American history. Meanwhile, US broad money supply has grown at roughly 6.6% annually since 1913, while bank accounts rarely keep pace. Scarce assets like waterfront property track money supply growth almost exactly.

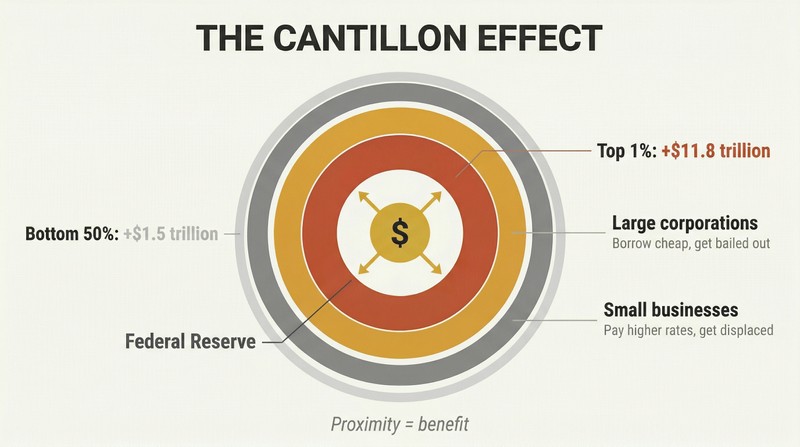

Inflation rewards those closest to the money printer

The Cantillon effect plays out dramatically. During 2020-2021, the top 1% collectively gained $11.8 trillion in net worth while the bottom 50% gained $1.5 trillion. A study found that three-quarters of the $800 billion Paycheck Protection Program went to the top 20% of households. Airlines that recklessly spent profits on buybacks received tens of billions in bailouts; prudent competitors were punished for their conservatism.

Access to cheap credit is the real divider. Large corporations borrow at low rates, expand with leverage, and get bailed out during crises. Small businesses pay higher rates and get displaced. Since 1972, US banks consolidated from 13,733 to 4,135, with the top ten holding 55% of all assets. The system inherently centralizes wealth toward those nearest the source of money creation.

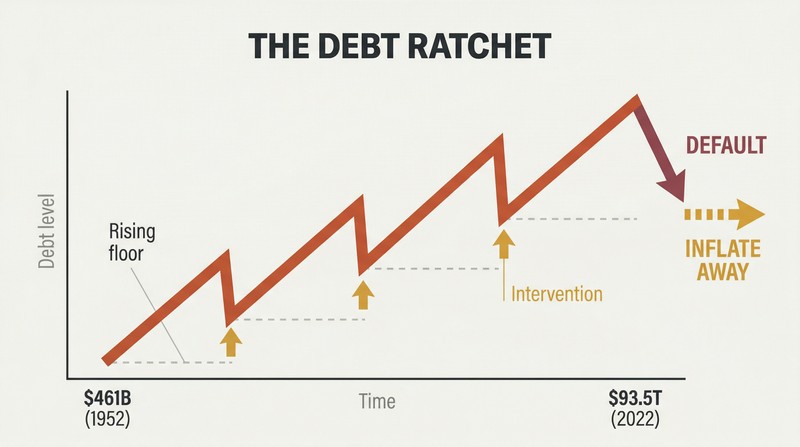

Debt compounds until society defaults or inflates it away

US total debt: $461 billion in 1952; $93.5 trillion in 2022. It was never allowed to decrease in that seven-decade span, except for a 1.3% blip during the 2008 crisis. By 2007, total debt was 63 times the monetary base — like musical chairs with 63 children per chair. When the music stopped, rather than let debt collapse, the Fed doubled the monetary base.

This is the long-term debt cycle. Short-term cycles build higher and higher debt through recurring policy interventions that prevent credit from ever clearing out. Eventually interest rates hit zero, debt levels become unworkable, and the resolution shifts from the private sector to the government, which inflates it away. The 2020s echo the 1940s: war-era deficits, financial repression, and purchasing power destruction for bondholders.

The world's reserve currency is hollowing America from within

Extra global demand for dollars is a curse. It makes US exports uncompetitive and workers expensive relative to peers. The US has run structural trade deficits since the 1970s, and its net international investment position has become deeply negative — foreigners own more American assets than Americans own abroad. Industrial production per capita has been declining since roughly 2000.

The system enriches two groups: American financiers and foreign exporters. It harms two others: American workers and developing-country consumers stuck saving in constantly devalued local currencies. The petrodollar arrangement likely helped win the Cold War, but since the 1990s it has been more curse than blessing. China now uses its trade surpluses to finance 150+ countries through the Belt and Road Initiative rather than buy US Treasuries.

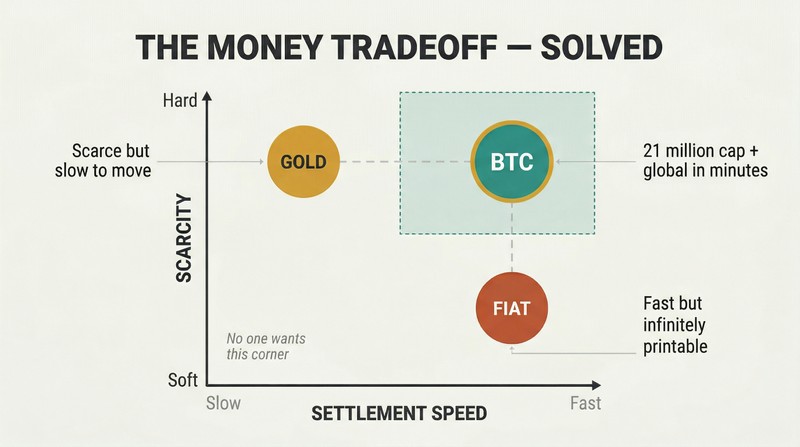

Bitcoin is the first scarce money that settles at the speed of light

Bitcoin closes the 150-year speed gap. For the first time, a finite digital asset (21 million coins, subdivided into 2.1 quadrillion units) can be self-custodied and transferred peer-to-peer globally within minutes — no bank required. The Blocksize War of 2015-2017 proved its decentralization: over 80% of miners and major exchanges tried to force a rule change and failed. Individual node operators maintained consensus.

The Lightning Network adds instant, near-free payments as a channel layer on top. Afghan refugee Laleh Farzan kept 2.5 bitcoin through her family's escape to Europe — thieves stole their jewelry and cash, but she hid her seed phrase on a scrap of paper. Navalny's Russian opposition used bitcoin after Putin's establishment froze their bank accounts. Nigerian protestors turned to it when their accounts were frozen by government.

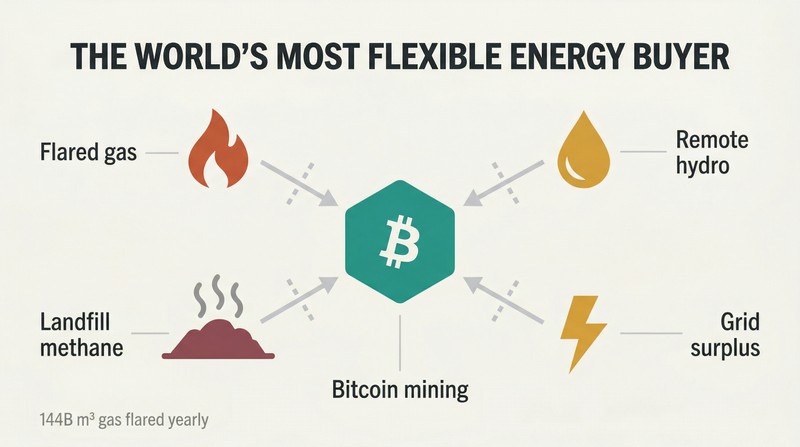

Bitcoin mining monetizes wasted energy no one else can use

Miners are unique energy buyers. They go to the energy source (rather than requiring energy to come to them), tolerate intermittent supply, and need rock-bottom prices — so they consume energy that would otherwise be wasted. The World Bank estimates 144 billion cubic meters of natural gas is vented or flared annually; that alone could power the Bitcoin network several times over.

Gridless in Kenya uses bitcoin mining to anchor rural hydropower microgrids, making small-river power development economically viable. Vespene Energy captures landfill methane. Texas miners curtail during peak demand, acting as a virtual grid battery. Bitcoin's energy usage is strictly limited by the utility it provides — and the declining block subsidy means energy consumption as a percentage of market capitalization has fallen every year.

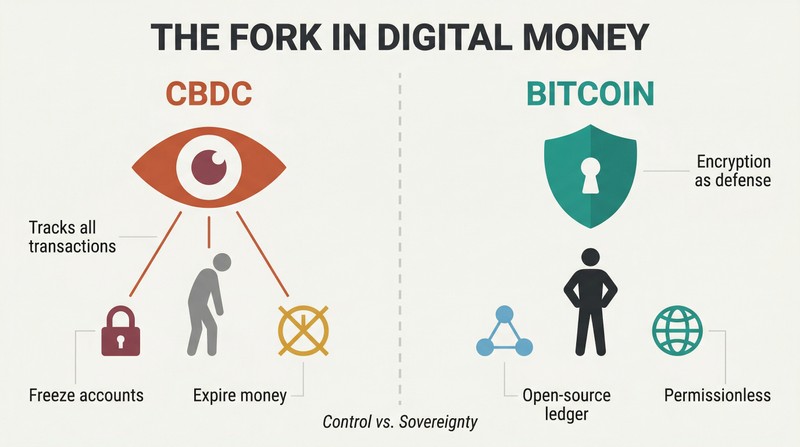

CBDCs turn money into a surveillance tool; Bitcoin pushes back

This is the fork in the road. China's digital yuan can track all transactions, set expiration dates on money, and auto-freeze accounts. The ECB's president suggested allowing zero anonymous transactions above €300-400 — citing a decade-old terrorist attack. Nigeria capped ATM withdrawals to $45/day to push citizens toward its eNaira, yet far more Nigerians adopted bitcoin and stablecoins instead.

Encryption provides asymmetric defense: cheap to deploy, impossible for supercomputers to break. Phil Zimmermann published his PGP encryption code as a book to invoke First Amendment protection when the US government classified it as munitions. Bitcoin extends this principle to value transfer. If the mere existence of an open-source ledger threatens the existing system, Alden argues, the problem lies with the existing system.

Analysis

Lyn Alden's central intellectual contribution is the speed gap thesis — the argument that the gold standard's global failure was a technological inevitability rather than a political choice. This reframing is more powerful than either the Austrian lament ('they shouldn't have abandoned gold') or the Keynesian dismissal ('gold is a barbarous relic'). By treating the financial system as an engineered system subject to technological constraints, Alden arrives at conclusions that challenge both camps: gold failed not because it was bad money, but because telecommunication-enhanced ledgers introduced speed as a competitive variable that physical bearer assets couldn't match.

The ledger theory of money is a genuine contribution to monetary economics. By recognizing that both commodity money and credit money are simply different methods of administering a ledger — with nature or human institutions as the respective administrators — Alden dissolves a debate that has persisted since at least Adam Smith and Mitchell-Innes. The framework also elegantly positions Bitcoin as a third category: a ledger governed by users through code, combining nature's resistance to debasement (via proof-of-work energy expenditure) with telecommunication-era speed.

The book's most vulnerable section is its Bitcoin analysis, which inevitably shifts from historical analysis to forward-looking speculation. Alden acknowledges this explicitly and devotes an entire chapter to risk analysis, which lends credibility. Her treatment of proof-of-work versus proof-of-stake — framing the distinction as volatile versus non-volatile memory — is one of the clearest explanations available. However, the book may underweight the political economy risk: governments have demonstrated willingness to suppress competing monetary technologies for centuries, and the combination of CBDC deployment with anti-privacy legislation could create a more hostile environment than the book anticipates.

What distinguishes this work from Ammous's Bitcoin Standard or Graeber's Debt is Alden's engineering discipline. She treats monetary systems as complex engineered systems with measurable parameters — stock-to-flow ratios, money multipliers, deposit-to-reserve ratios — rather than as purely ideological constructs. This makes her arguments falsifiable and her framework transferable to readers who may not share her conclusions about Bitcoin specifically.

Review Summary

Readers overwhelmingly praise "Broken Money" for its comprehensive and accessible explanation of monetary systems. Many appreciate Alden's balanced approach, combining historical context with modern financial analysis. The book's exploration of Bitcoin and cryptocurrencies receives mixed reactions, with some finding it insightful and others viewing it as overly enthusiastic. Overall, reviewers commend the book for its clarity in explaining complex financial concepts and its thought-provoking ideas about the future of money.

People Also Read

Glossary

Stock-to-flow ratio

Existing supply versus annual productionA measure of monetary scarcity calculated by dividing the total existing supply of a commodity (the stock) by the amount of new supply produced annually (the flow). Gold's ratio of roughly 67 is the highest of any commodity, meaning 67 years of mining would be needed to double existing supply. Higher ratios indicate greater resistance to supply dilution and thus better monetary properties.

Ledger theory of money

Money as a ledger systemAlden's proposed unification of the commodity theory and credit theory of money. It holds that all forms of money — from shell beads to gold coins to bank deposits to Bitcoin — are fundamentally methods of maintaining a ledger. The key differences between monetary systems are who or what administers the ledger: nature (commodity money), human institutions (credit/fiat money), or user-operated code (open-source cryptocurrency).

Speed gap

Transaction speed minus settlement speedAlden's term for the foundational mismatch created when the telegraph enabled transactions to move at the speed of light while physical bearer assets like gold could only settle at the speed of matter. This gap, which opened in the 1860s, gave banks and central banks a monopoly on fast long-distance payments and is identified as the root cause of the global gold standard's failure and the rise of fiat currency systems.

Monetary premium

Excess value from savings demandThe portion of an asset's market value that exceeds its pure utility value, arising because many people hold the asset as savings rather than for its end-use purpose. Gold's price, for example, far exceeds what industrial demand alone would justify. The premium creates a permanent incentive for people to produce more of the asset, which is why only commodities with very high stock-to-flow ratios can maintain a monetary premium long-term.

Cantillon effect

Uneven impact of new moneyAn 18th-century observation by Richard Cantillon describing how newly created money does not affect all prices simultaneously. Those closest to the source of money creation — banks, large corporations, government contractors — benefit first by spending new money at prevailing prices, while those furthest from the source experience only the resulting price inflation. Alden applies this to modern selective bailouts and quantitative easing.

Long-term debt cycle

Multi-decade debt accumulation patternA pattern spanning several decades in which successive short-term business cycles accumulate higher and higher levels of total debt relative to the economy, because policymakers intervene to prevent debt from ever fully clearing out. The cycle culminates when interest rates reach zero, sovereign debt levels become unsustainable, and the resolution involves significant inflation, financial repression, or debt restructuring — as occurred in the 1940s and appears to be recurring in the 2020s.

Financial repression

Inflating away government debt covertlyA set of government policies that keep interest rates below the prevailing inflation rate while restricting citizens' ability to flee to alternative assets. This forces bondholders and savers to accept negative real returns, effectively transferring wealth from creditors to the government debtor. During 1945-1980, real interest rates across advanced economies were negative roughly half the time, liquidating much of the WWII-era government debt.

Difficulty adjustment

Bitcoin's self-regulating mining calibrationAn automatic recalibration mechanism in the Bitcoin protocol that occurs every 2,016 blocks (approximately two weeks). If blocks are being produced faster than the ten-minute target — because more computational power has joined the network — the mining puzzle becomes harder. If blocks slow down because miners leave, it becomes easier. This ensures consistent block production regardless of total network mining power, and was a key innovation by Satoshi Nakamoto.

FAQ

What's Broken Money about?

- Historical Evolution: Broken Money by Lyn Alden explores the historical evolution of money, from ancient systems to modern financial structures. It examines how money emerged to solve the inefficiencies of barter.

- Critique of Fiat Systems: The book critiques current fiat monetary systems, highlighting their flaws and susceptibility to manipulation, which lead to economic imbalances and crises.

- Future of Money: Alden discusses the potential of cryptocurrencies and stablecoins as alternatives to traditional financial systems, aiming to empower readers to understand and consider these new forms of money.

Why should I read Broken Money?

- Comprehensive Understanding: The book provides a thorough understanding of how money works and its historical context, helping readers make informed financial decisions.

- Critical Analysis: It offers a critical analysis of the current financial system, encouraging readers to question the status quo and consider the implications of monetary policy.

- Technological Insights: Alden discusses the impact of technology on money, making it a timely read as digital currencies gain prominence.

What are the key takeaways of Broken Money?

- Nature of Money: Money is fundamentally a ledger, reflecting societal needs and technological advancements. Understanding its properties is crucial for recognizing its value.

- Flaws in Fiat Systems: Current fiat systems are prone to inflation and manipulation, leading to economic instability and exacerbating inequality, especially in developing countries.

- Emerging Alternatives: Cryptocurrencies and decentralized finance present new opportunities for financial control and solutions to traditional banking problems.

What are the best quotes from Broken Money and what do they mean?

- "Money is a ledger.": This quote encapsulates the idea that money serves as a record of transactions and ownership, emphasizing the importance of understanding its mechanisms.

- "The financial system as we know it isn’t working anymore.": Alden highlights the growing discontent with current systems, underscoring the need for reform and innovation.

- "Politics can affect things locally and temporarily, but technology can affect things globally and permanently.": This emphasizes the transformative power of technology in shaping the future of money.

How does Lyn Alden define money in Broken Money?

- Definition of Money: Alden defines money as a ledger that records transactions and ownership, evolving from physical commodities to digital forms.

- Historical Context: The book traces money's historical development, showing how societies have used various forms based on needs and technology.

- Social Credit: Alden discusses social credit, informal systems of trust and reputation that underpin transactions, illustrating money as a social construct.

What are the main criticisms of the current financial system in Broken Money?

- Inflation and Devaluation: Alden criticizes fiat currencies for losing value over time, disproportionately affecting savers and developing countries.

- Centralized Control: The book highlights the dangers of centralized banking systems, which can manipulate money supply and interest rates without accountability.

- Inequality: Alden argues that the current system exacerbates inequality, particularly in developing nations lacking access to stable money.

How does Broken Money address the rise of cryptocurrencies?

- Potential Solutions: Cryptocurrencies, particularly Bitcoin, offer a decentralized alternative to fiat currencies, providing more financial control and protection against inflation.

- Trade-offs and Risks: The book discusses the risks of cryptocurrencies, including volatility and regulatory challenges, emphasizing the need for understanding before investing.

- Future of Money: Alden posits that cryptocurrencies represent a significant shift in the monetary landscape, potentially reshaping global value storage and transfer.

What is the Cantillon Effect mentioned in Broken Money?

- Definition: The Cantillon Effect describes how monetary expansion benefits are unevenly distributed, favoring those closest to new money sources.

- Impact on Inequality: This effect exacerbates economic inequality, as early recipients of new money can spend it before inflation erodes its value.

- Policy Implications: Understanding the Cantillon Effect is crucial for reforming financial systems to ensure more equitable wealth distribution.

How does Lyn Alden view the future of banking in Broken Money?

- Decentralization Trends: Alden envisions decentralized finance and cryptocurrencies challenging traditional banking, offering greater financial control.

- Technological Integration: The book discusses technology's potential to enhance banking services, addressing current system shortcomings.

- Need for Reform: Alden emphasizes reforming banking practices to create a more equitable financial system, prioritizing transparency and accountability.

What role do central banks play in the financial system according to Broken Money?

- Monetary Policy Control: Central banks control money supply and interest rates, significantly impacting the economy, but Alden critiques their lack of oversight.

- Crisis Management: Central banks act as lenders of last resort during crises, but this can lead to moral hazard and risky bank behavior.

- Impact on Inflation: Alden highlights central banks' role in creating inflation, eroding purchasing power, especially in developing countries.

How does Broken Money relate to current global economic issues?

- Inflationary Pressures: Alden connects the book's themes to current inflationary pressures, discussing how monetary policy responses can exacerbate these issues.

- Geopolitical Tensions: The book addresses how global financial systems are influenced by geopolitical tensions, particularly regarding the U.S. dollar's status.

- Call for Alternatives: Alden advocates for exploring alternative monetary systems that prioritize stability and equity, addressing ongoing economic challenges.

What role do cryptocurrencies play in the future of money according to Alden?

- Alternative to Fiat: Cryptocurrencies, particularly Bitcoin, are seen as potential alternatives to fiat currencies, offering scarcity, portability, and censorship resistance.

- Decentralized Finance: The rise of decentralized finance could democratize access to financial services, reducing reliance on traditional banks.

- Challenges and Risks: While optimistic about cryptocurrencies, Alden acknowledges risks like regulatory scrutiny, technological vulnerabilities, and market volatility.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.